Why India’s Strongest Businesses Sell the Simplest Products

SECTION I: Investment Thesis & Summary

This is India’s most trusted consumer franchise — the kind of company that sells you something before you brush your teeth in the morning and again before you sleep at night. But right now, the stock is priced for perfection in a business that’s delivering anything but. Revenue growth has been sluggish, margins are plateauing, and the price hasn’t come down enough to make this a screaming buy.

The HOLD is not a vote of no confidence in the business. It’s a valuation call. At roughly 49x trailing earnings, you’re paying a serious premium for single-digit revenue growth. The story gets better from here — rural recovery, premiumisation, and volume momentum are all building. But the stock needs to either correct further, or the earnings need to meaningfully accelerate, before this becomes a compelling entry.

Simply put: exceptional company, fair-to-slightly-expensive price. Wait for a better entry, or accumulate slowly on dips.

SECTION II: Business Model & Operations

The business is refreshingly simple to understand. It sells everyday products — detergents, shampoo, skincare, tea, coffee, soups, ice cream — across five segments: Home Care, Beauty & Wellbeing, Personal Care, Foods, and Others. Every product category it operates in, it leads. Market leadership in over 85% of its categories. That’s not luck — that’s distribution muscle built over nine decades.

The distribution network is the real moat here. Over a million retail outlets. Deep rural penetration. A supply chain that few Indian companies can replicate at this scale.

Here’s what’s been happening lately. The company confirmed in March 2026 that it has no plans to divest its Foods portfolio — that clarification itself tells you the market had been pricing in uncertainty. The Foods segment (tea, coffee, culinary products) contributes roughly 25% of topline and management wants it. A ₹2,000 crore investment plan in premium beauty, wellbeing, and home care over the next two years signals confidence in premiumisation as the next growth engine.

The strategic portfolio is split into three buckets — Core brands (scale and margin), Future Core (premiumisation plays), and Market Makers (new categories being seeded). This structure is deliberate: it funnels capital toward higher-margin products while keeping the cash-generative base brands intact.

Youtube Link:

SECTION III: Historical Financial Review

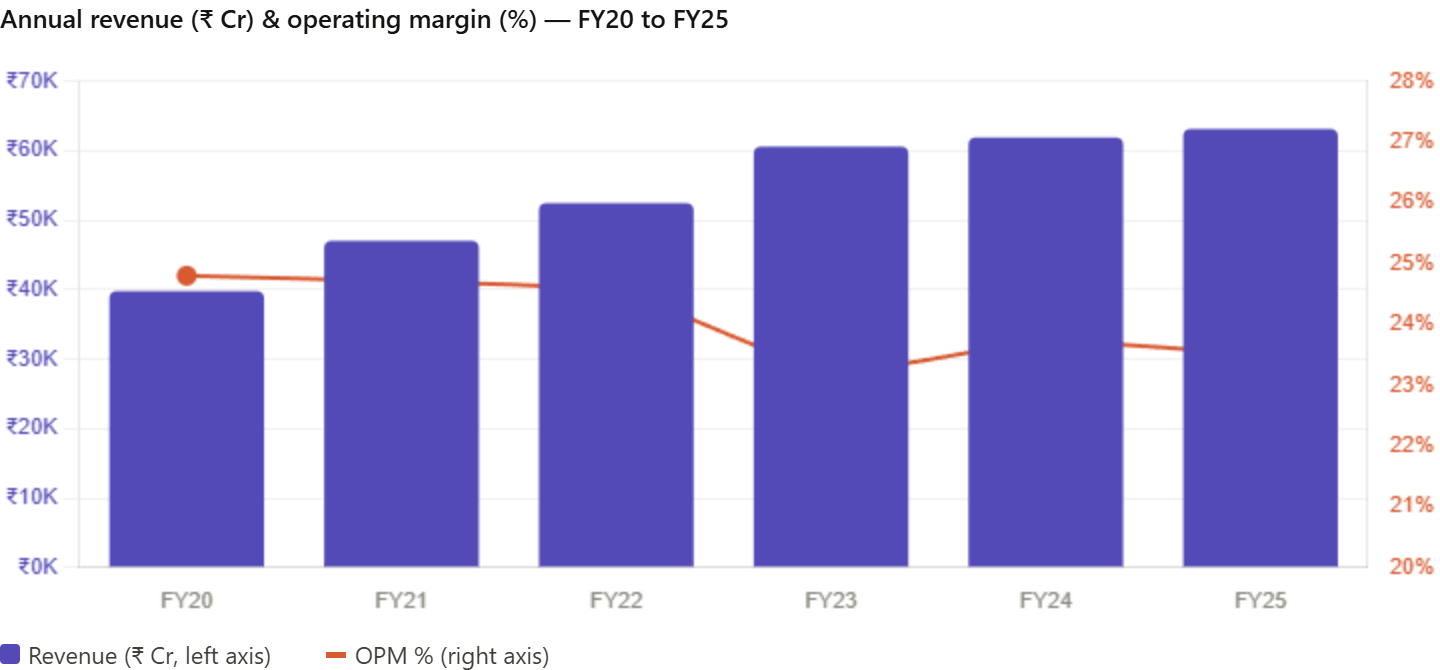

The numbers tell a mixed story. Revenue has grown from ₹52,446 crore in FY22 to ₹63,121 crore in FY25 — that’s a 3-year CAGR of roughly 6.4%. Sounds modest for a company of this stature, and it is. Five-year revenue CAGR is even softer at under 10%. This isn’t a high-growth FMCG story right now. It’s a high-quality, steady-compounding one.

FY25 annual revenue: ₹63,121 Cr | Operating profit: ₹14,843 Cr | OPM: ~23.5%

The operating margin has been remarkably stable — hovering between 23% and 24% quarter after quarter. That consistency is actually a hallmark of quality. Input cost pressures (palm oil, crude derivatives) hit and the company absorbs or passes through — margins barely flinch.

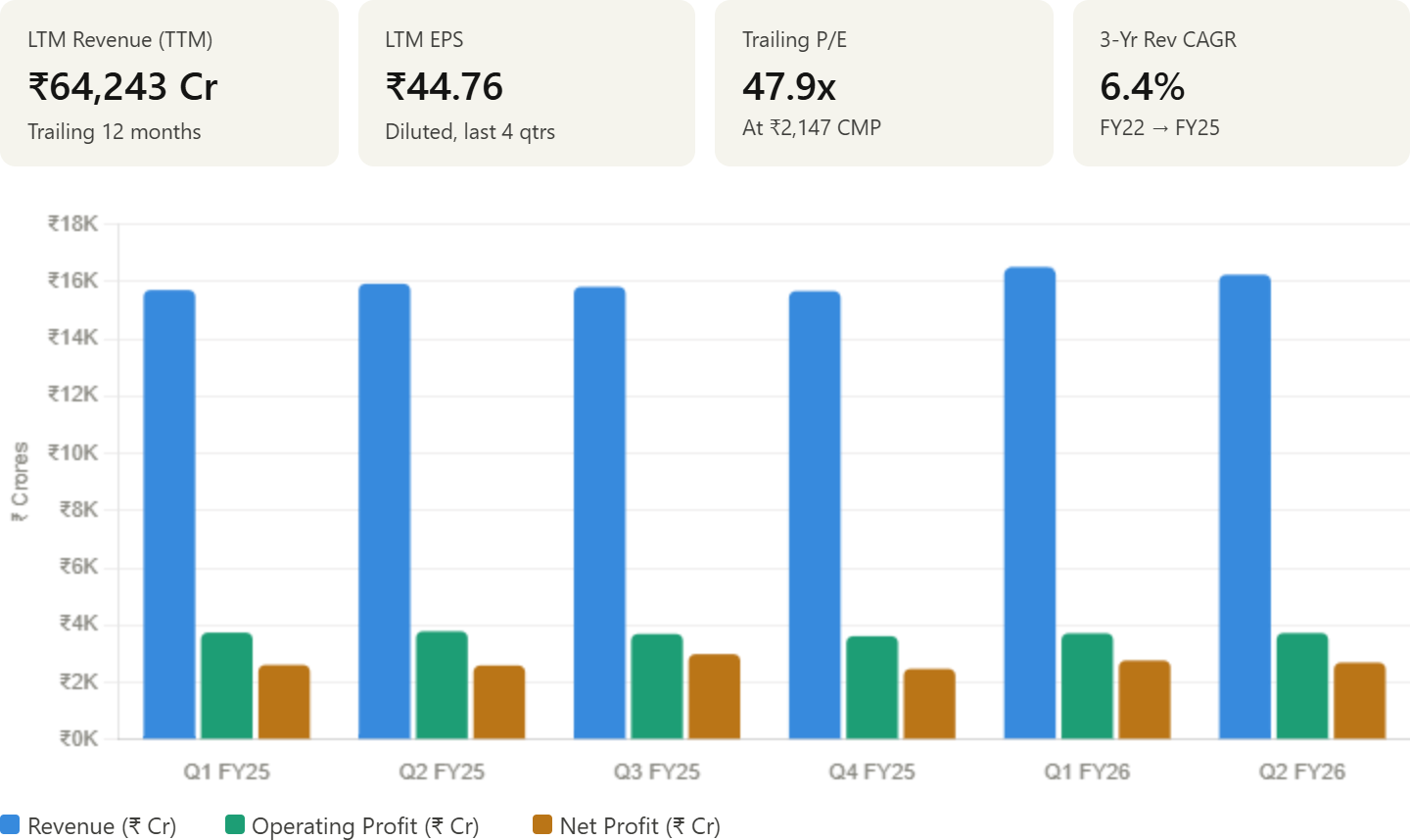

FY26 quarterly performance (available quarters):

Revenue for Q1 FY26 at ₹16,514 crore was the highest single-quarter topline in company history at the time — a 5.1% year-on-year jump. Q2 followed at ₹16,241 crore, marginally lower sequentially but still 2% higher year-on-year. Volume growth is back. That’s the important thing.

LTM (Last 12 Months) Diluted EPS: ~₹45.65

Sum up Q3 FY25 (₹10.49) + Q4 FY25 (₹11.11) + Q1 FY26 (₹11.73) + Q2 FY26 (₹11.43) and you get ~₹44.76. At the current price of ₹2,147, the trailing P/E sits around 47-49x. That’s a premium valuation — justifiable only if earnings accelerate meaningfully.

ROCE: 27.8% | ROE: 20.7% — Both are healthy. The company earns well above its cost of capital. That’s what a great business looks like over time.

Dividend yield: ~1.78% — With a 100%+ payout ratio, the dividend is essentially the entire net profit redistributed to shareholders. That’s comforting for income investors, but it also means almost zero reinvestment into the business from internal cash flows.

SECTION IV: Growth Drivers & Opportunities

Rural recovery is the single biggest growth catalyst. Rural India was squeezed by inflation and weak purchasing power through FY24-25. As food inflation cools and rural wages recover, the lowest-unit-price sachets and economy packs — this company’s heartland — see a volume revival. Early signs are visible in the recent quarterly trends.

Premiumisation is the margin story. The average Indian consumer is trading up. Liquid detergents over bars. Premium skincare over basic soap. Specialty coffee over mass tea. This company’s portfolio covers both ends of the market, but the capital allocation toward premium segments is where future margin expansion lives. The ₹2,000 crore commitment over two years in beauty and wellbeing is exactly the right bet.

Pricing power with discipline. The company hasn’t chased volume at the cost of margins. When input costs rose, it took calibrated price increases. When costs eased, it passed some benefit to consumers to drive volumes. This maturity in pricing decisions is rare.

Favourable demographics. India’s median age is 28. A young, aspirational population with rising disposable incomes in tier-2 and tier-3 cities is the long runway for branded FMCG. This company is already present in every one of those markets.

SECTION V: Risks to Monitor

Competitive intensity is rising — fast. D2C brands, regional challengers, and private labels are chipping at market share in premium categories. A digitally native skincare brand can build distribution and awareness in 18 months that used to take a decade. The company is responding, but this is a structural headwind.

Input cost volatility. Crude oil derivatives (packaging, surfactants), palm oil, and agri commodities are the key inputs. A surge in crude or an El Niño-driven spike in palm oil prices compresses margins. With OPMs already thin at 23-24%, any sharp move hits the bottom line directly.

Foods segment overhang. Market chatter around Foods divestiture rattled the stock earlier in 2026. Management has clarified their position — no sale. But the perception risk lingers. If Unilever globally pivots its strategy, the local entity has limited autonomy to resist.

Valuation leaves no room for disappointment. At ~49x trailing P/E, even a single quarter of revenue miss or margin compression can send the stock down 5-8% in a session. There’s no margin of safety at current prices.

Icecream demerger. The demerger of the ice cream business (into Kwality Wall’s India Ltd) is progressing. This will shrink the reported topline slightly and may create temporary valuation confusion. It’s not a negative long-term, but creates short-term noise.

SECTION VI: Valuation & Target Price

The target price of ₹2,610 is derived from a forward earnings basis. Assuming FY27 EPS of roughly ₹52-54 (factoring in modest 6-8% earnings growth as volume recovery and premiumisation play out), applying a 48-50x multiple — consistent with the stock’s historical premium band — gives a 12-month fair value of ₹2,500-2,700. The midpoint of ₹2,610 represents approximately 21-22% upside from current levels.

5-year return scenario (Base Case): Assuming 7-8% revenue CAGR, margin stability at 23-24%, and a slight P/E de-rating to 42-44x by FY31 as growth matures, the stock could compound at 10-12% annually — decent but not spectacular for a blue-chip holding.

Bull case: Rural recovery accelerates, premiumisation drives OPM expansion to 25%+, Foods segment rerated positively post-demerger clarity → stock re-rates toward ₹3,000+ in 18 months.

Bear case: Sustained competitive pressure, input cost shock, or macro slowdown compresses earnings → stock tests ₹1,900-2,000 support.

The risk/reward at ₹2,147 is roughly balanced. HOLD for existing investors. Accumulate below ₹1,950 for new positions.