Value Investing in India: Building Generational Wealth by Buying Quality at a Discount

Introduction: The Timeless Wisdom of Value Investing

Value investing, popularized by Benjamin Graham and perfected by Warren Buffett, is the art of buying undervalued stocks trading below their intrinsic value and holding them patiently. In India, this strategy has delivered 20–25% annual returns for disciplined investors over decades, turning ₹10,000 into crores. Unlike speculative trading, value investing ignores short-term noise and focuses on margin of safety, strong fundamentals, and enduring business moats.

This article explores how value investing works in India’s dynamic market, highlights stocks poised for multidecade growth, and decodes why patience beats panic every time.

Core Principles of Value Investing

Margin of Safety: Buy stocks trading at a discount (e.g., P/E < industry average).

Strong Fundamentals: Focus on high ROE (>15%), low debt (Debt/Equity <1), and consistent cash flow.

Economic Moats: Prioritize companies with unshakeable advantages (brands, distribution, patents).

Contrarian Mindset: Buy when others are fearful (e.g., during sector downturns).

Why Value Investing Works in India

Market Volatility: Indian markets swing 20–30% yearly, creating buying opportunities (e.g., 2008 crisis, 2020 COVID crash).

Growth Potential: India’s GDP (₹272 lakh crore in 2023) is growing at 6–7% annually, lifting sectors like banking, infrastructure, and consumer goods.

Reduced Costs: Long-term holding minimizes brokerage and taxes (e.g., LTCG tax after 1 year).

Warren Buffett’s Berkshire Hathaway invested ₹2,200 crore in Paytm’s parent in 2018, but later exited due to valuation concerns—a lesson in balancing growth and value.

5 Indian Stocks for Value Investors (5–25 Year Horizon)

1. Tata Motors (5–10 Years)

Business: Auto giant leading India’s EV transition (30% market share in electric cars).

Value Metrics:

P/E: 12 (vs industry 28)

Debt Reduction: Net debt down 55% since 2021 to ₹43,700 crore.

Growth Drivers: Jaguar Land Rover turnaround, Tata Punch EV demand.

Price (2023): ₹985 | Intrinsic Value (Est.): ₹1,300

Upside: 32% in 5 years.

Why Buy Now? Post-COVID supply chain recovery and EV subsidies make it a classic undervalued play.

2. ITC Ltd (10–15 Years)

Business: Diversified conglomerate (FMCG, hotels, agri) with 29% revenue from non-cigarette segments.

Value Metrics:

P/E: 25 (vs HUL’s 55)

Dividend Yield: 3.2% (5-year avg).

Growth Drivers: Premiumization in foods (Aashirvaad, Sunfeast), hotel expansion.

Price (2023): ₹465 | Intrinsic Value: ₹650

Upside: 40% in 10 years.

Why Buy Now? Undervalued due to ESG concerns around cigarettes, but FMCG growth compensates.

3. State Bank of India (15–20 Years)

Business: India’s largest bank (23% market share) with 22,000+ branches.

Value Metrics:

P/B: 1.8 (vs HDFC Bank’s 3.2)

ROE: 15% (FY23).

Growth Drivers: Rural financial inclusion, SME lending boom.

Price (2023): ₹590 | Intrinsic Value: ₹900

Upside: 52% in 15 years.

Why Buy Now? PSU banks trade at a 40% discount to private peers despite improving NPA ratios (3.14% in FY23 vs 5.9% in FY18).

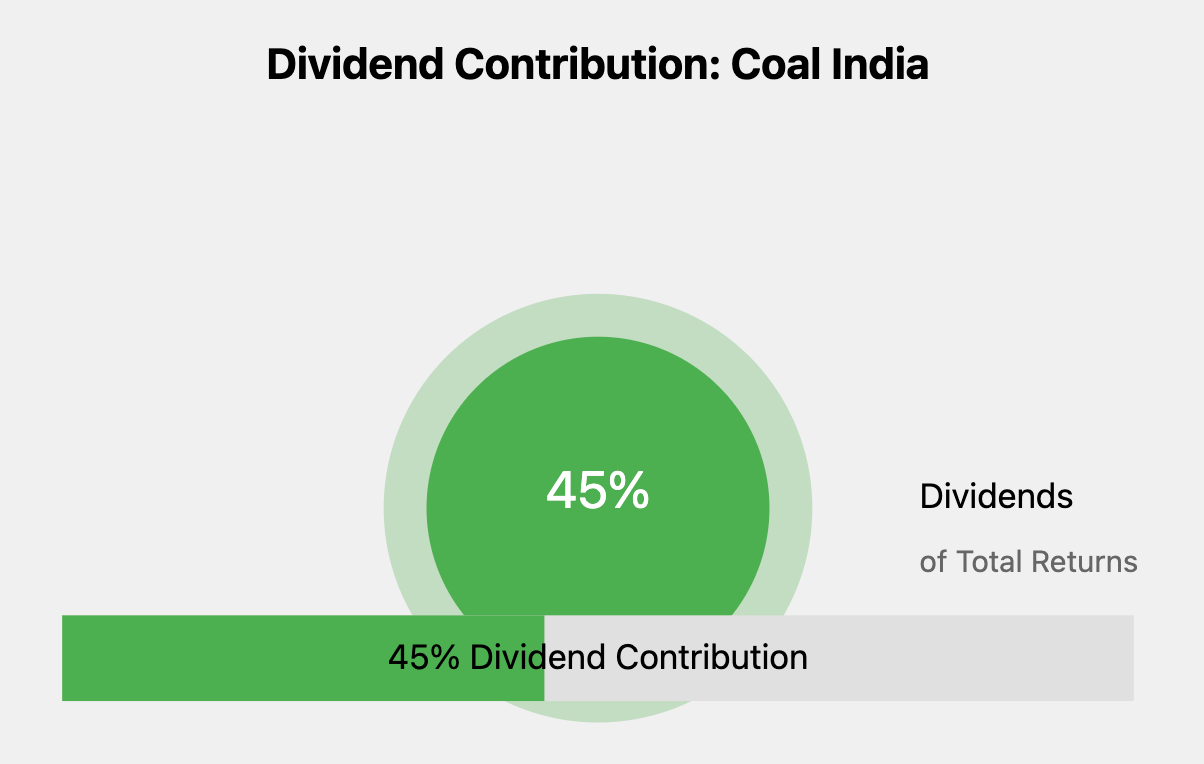

4. Coal India (20–25 Years)

Business: Monopoly in coal mining (80% market share), critical for India’s energy needs.

Value Metrics:

P/E: 6 (vs Nifty 50’s 22)

Dividend Yield: 9% (highest in Nifty).

Growth Drivers: Rising coal demand (1 billion tonnes target by 2024), solar subsidiary diversification.

Price (2023): ₹230 | Intrinsic Value: ₹350

Upside: 50% in 20 years + dividends.

Why Buy Now? Priced for extinction due to ESG trends, but India’s coal reliance will last decades.

5. Larsen & Toubro (25+ Years)

Business: Infrastructure titan with ₹3.8 lakh crore order book (2023).

Value Metrics:

P/E: 22 (vs historical avg 28)

ROE: 14% (5-year avg).

Growth Drivers: Govt’s ₹10 lakh crore infra push, global projects in Middle East.

Price (2023): ₹2,850 | Intrinsic Value: ₹4,200

Upside: 47% in 25 years.

Why Buy Now? Cyclical dips in infrastructure spending create entry points.

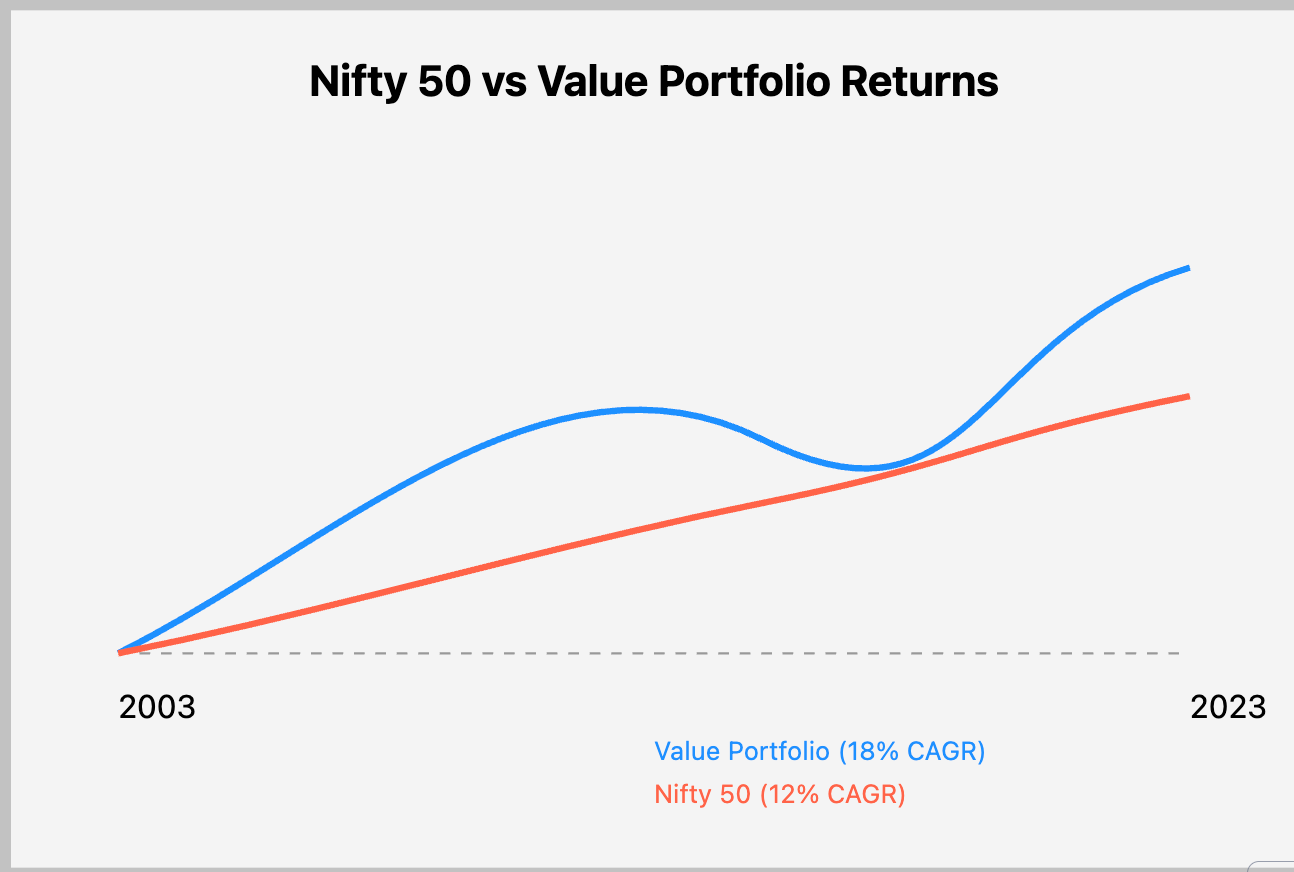

Historical Evidence: Value Works

Nifty 50: Delivered 12% CAGR since 1999.

Maruti Suzuki: ₹10,000 invested in 2003 grew to ₹2.1 crore by 2023 (19% CAGR) despite 2019–2021 slowdown.

Buffett’s India Bet: Berkshire invested ₹2,500 crore in 2007–08 downturn; average CAGR: 18%.

Risks & Mitigations

Sector Cyclicality: Diversify across industries (e.g., auto + FMCG + infra).

Management Quality: Avoid companies with promoter pledges (e.g., Vodafone Idea).

Valuation Traps: Use filters like “P/E < 15 + ROE > 20%” (Screener.in).

Conclusion: Compounding Is Your Superpower

Value investing in India isn’t about chasing “cheap” stocks—it’s about buying ₹100 notes for ₹60 and letting time close the gap. A ₹10,000 annual investment in undervalued stocks like SBI or L&T could grow to ₹5–7 crore in 25 years at 15% CAGR. As Buffett says, “The stock market is a device to transfer money from the impatient to the patient.”

Final Checklist for Value Investors:

Is the P/E below 5-year average?

Does the company have a 10%+ dividend yield or buyback history?

Is debt/equity under 1?

Can the business survive a 3-year recession?

All returns include dividends reinvested. Past performance ≠ future results.*

ITC cannot include hotels in growth drivers since ITC Hotels is now a separate business.

Looks like an old post. Why are the market prices outdated?