Unlocking Value: CPCL’s Q3 FY2025 Performance & Growth Outlook

Greetings Investors,

Welcome to this exclusive premium edition of our financial newsletter, where we dissect the latest Q3 FY2025 results of Chennai Petroleum Corporation Limited (CPCL) and project its long-term investment potential. If you’re looking for data-backed insights, compelling valuation estimates, and a clear roadmap for wealth creation, this is a must-read.

So, is CPCL a hidden gem in India’s energy sector? Let’s find out. 🧐

📊 CPCL Q3 FY2025: Numbers That Matter

📢 Financial Highlights (YoY Performance)

🔹 Revenue: ₹59,827 Cr (-10.3%)

🔹 Operating Profit Margin (OPM): 2.13%

🔹 Profit After Tax (PAT): ₹372 Cr (-88.1%)

🔹 ROE: 35.9% | ROCE: 35.1%

🔹 Dividend Yield: 12.2%

🔹 Debt: ₹6,114 Cr | Reserves: ₹7,569 Cr

🔹 Stock P/E: 18.1 | Book Value: ₹518

🔹 Market Cap: ₹6,725 Cr

🔹 Stock Price: ₹452 (52-Week High/Low: ₹1,275 / ₹450)

🔹 Promoter Holding: 67.3%

📉 Despite a dip in profits, CPCL remains a strong dividend play and a cash-generating powerhouse in the refining sector. The market correction presents a golden opportunity for long-term investors.

🏗️ CPCL’s Future Roadmap: What Lies Ahead?

🛢️ Expansion & Capex Plans

✅ Cauvery Basin Refinery Expansion – Increased refining capacity & better product diversification.

✅ Entry into Petrochemicals – Higher-margin products to drive profitability.

✅ Massive Capex Plans – Focused investments in automation & infrastructure modernization.

✅ Green Energy Transition – Exploring alternative fuel refining for long-term sustainability.

🔍 Strategic Rationale: CPCL is aligning itself with India’s growing energy demand while transitioning into a high-value petrochemical player, which could improve margins & reduce earnings volatility.

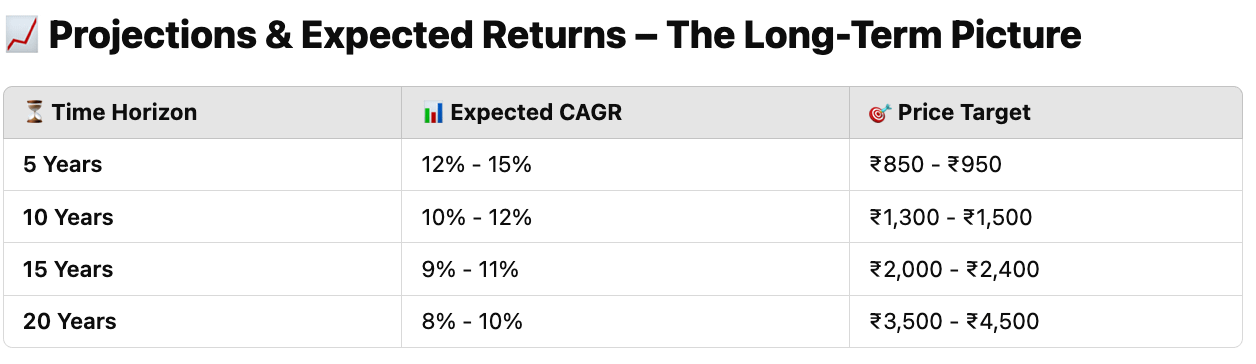

📈 Projections & Expected Returns – The Long-Term Picture

🚀 Key Growth Drivers:

Rising crude oil processing capacity

Expansion into high-margin petrochemicals

Strategic government support for energy players

Strong dividend yields, making it an income+growth stock

💡 Investor Takeaway: CPCL offers multifold wealth creation potential over the next two decades, making it a compelling BUY for long-term investors.

🔬 Competitive Landscape & Challenges

💪 Strengths:

✅ Backed by Indian Oil Corporation (IOC) – Ensuring long-term stability. ✅ Strategic location – Near ports & demand centers, minimizing logistics costs. ✅ Massive capex pipeline – Ensuring future scalability.

⚠️ Risks & Challenges:

❌ Crude Oil Price Volatility – A key determinant of refining margins. ❌ Regulatory Uncertainty – Compliance with environmental norms could add costs. ❌ Debt Levels – ₹6,114 Cr debt might pressure cash flows in weaker quarters. ❌ Refining Margins – Lower GRMs can impact short-term profitability.

🔍 Risk Mitigation: CPCL’s entry into petrochemicals & refinery expansion will buffer profitability against crude price swings.

💰 Valuation & Investment Thesis: The Case for CPCL

🎯 CPCL’s Fair Value Estimate:

📌 12-Month Target: ₹600 - ₹700 (30-50% upside potential).

📌 Long-Term Target: ₹3,500+ (by 2045, assuming a 9-10% CAGR).

📌 Why CPCL?

✅ Strong Financials & ROE (35.9%) – Solid fundamentals. ✅ Aggressive Expansion Plans – Capex-driven growth story. ✅ Attractive Valuation (P/B below 1x) – Stock trading at a discount. ✅ Generous Dividend Yield (12.2%) – Regular passive income.

📢 Final Verdict: CPCL remains an undervalued long-term play with strong earnings potential, making it a high-conviction pick for value investors.

📜 Disclaimer

This premium newsletter is for educational & informational purposes only and should not be considered as financial advice. Always consult with a certified financial advisor before making investment decisions.