Unconventional Strategies for Generational Wealth Creation

Building Generational Wealth: A Vision for Your Family’s Future

Paradigm-Shifting Insight Introduction:

The common narrative of generational wealth often fixates on the accumulation of assets. We are told to save more, invest wisely, and avoid profligacy. While undeniably important, this focus misses the true fulcrum of multi-generational affluence: the transmutation of capital into adaptive systems. Most investors treat wealth as a static quantity, a sum to be passed down. True generational wealth, however, is a dynamic ecosystem, designed not just to survive, but to evolve across economic epochs. The traditional approach, often glorified in financial media, views a large inheritance as the goal. My experience managing multi-billion dollar portfolios has repeatedly shown that an undifferentiated lump sum, without an embedded adaptive framework, is often a curse rather than a blessing, frequently dissipating within two generations. The truly wealthy build resilient, self-optimizing financial architectures, not just large bank accounts.

Watch the full video breakdown here

Youtube link:

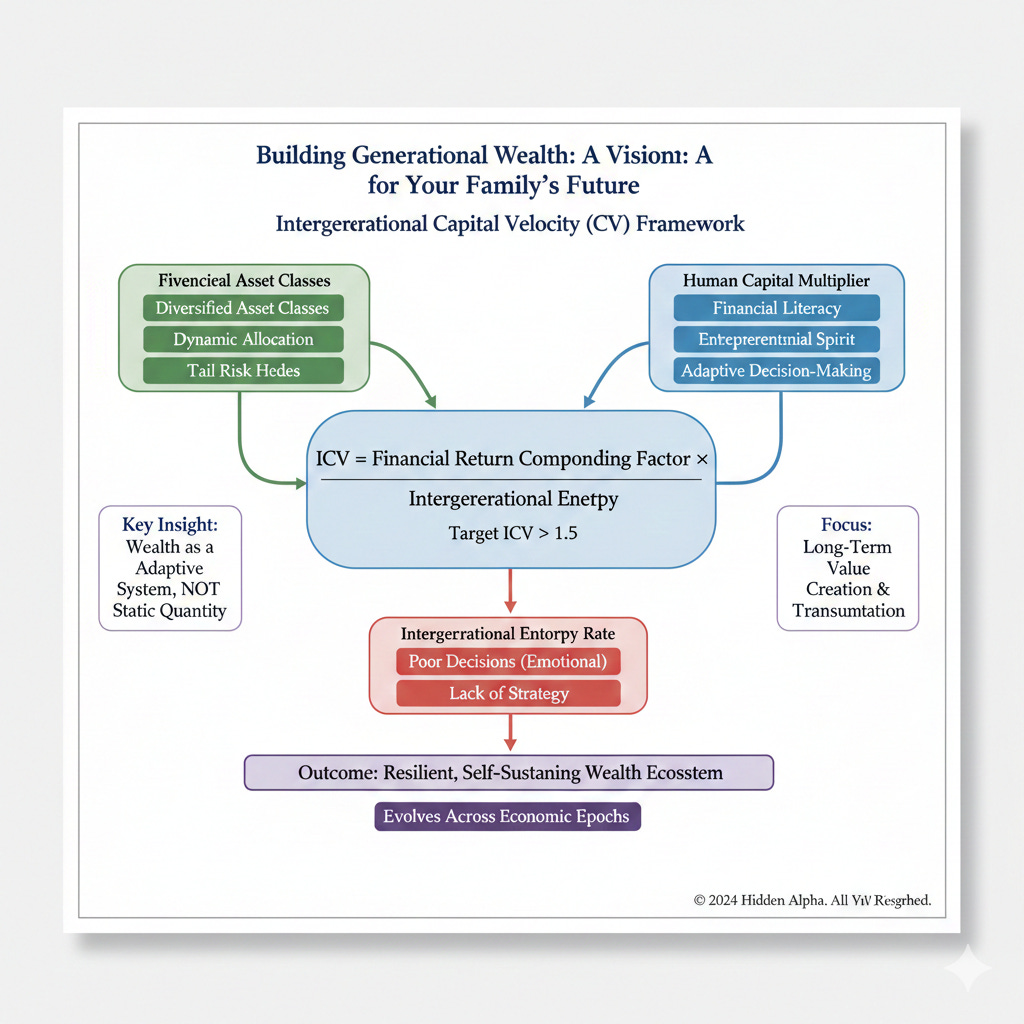

Advanced Analytical Framework: The Intergenerational Capital Velocity (ICV) Index

Standard wealth planning often relies on simple return targets and estate tax mitigation. My proprietary framework, the Intergenerational Capital Velocity (ICV) Index, assesses the efficiency with which capital adapts and compounds across generations, factoring in both explicit financial returns and implicit human capital development.

The ICV Index is calculated as:

ICV = (Financial Return Compounding Factor × Human Capital Multiplier) / Intergenerational Entropy Rate

Financial Return Compounding Factor: This isn’t just CAGR. It’s a measure of return diversification quality – how well different asset classes are integrated to perform across varying macro-regimes. We use a proprietary covariance matrix that prioritizes assets with genuinely uncorrelated returns during systemic shocks, not just periods of benign growth. This involves active management of tail risk hedges and dynamic asset allocation.

Human Capital Multiplier: This is the most overlooked component. It quantifies the investment in the next generation’s financial literacy, entrepreneurial spirit, and adaptive decision-making skills. It includes structured mentorship, early exposure to investment principles, and the cultivation of critical thinking, rather than merely bestowing wealth. A high multiplier indicates that successive generations are equipped to grow the wealth, not merely consume it.

Intergenerational Entropy Rate: This measures the rate at which wealth erodes due to consumption, poor investment decisions, taxes, and a lack of adaptive strategy. A key insight here is that emotional decisions and lack of financial education contribute more to entropy than market corrections.

A high ICV signifies a robust, self-sustaining wealth ecosystem, built to withstand economic shifts and familial challenges. We aim for an ICV above 1.5, which indicates that the wealth system is not just maintaining its value, but actively growing its adaptive capacity.

Visual Knowledge Synthesis: Here’s a visualization of the ICV framework, illustrating how these components interact:

Elite-Level Application Examples:

Consider two families, both starting with $100 million.

The “Static Accumulation” Family (Low ICV): This family focused on maximizing immediate investment returns through a concentrated portfolio of growth stocks. They left a sizable inheritance to their children without significant financial education, relying on trust funds. After a decade, the initial $100M grew to $250M, but the next generation, unfamiliar with wealth management and lacking a strong entrepreneurial drive, made several poor lifestyle choices and speculative investments. When a major market downturn hit, their highly concentrated portfolio was devastated. Within two generations, the $250M was reduced to $30M, largely due to a high Intergenerational Entropy Rate from poor decisions and a low Human Capital Multiplier.

The “Adaptive System” Family (High ICV): This family also started with $100M but immediately diversified into a “Barbell Strategy” – a core portfolio of robust, dividend-paying companies providing stability, coupled with a smaller, actively managed venture capital fund focused on emerging technologies. Critically, they established a family office dedicated to educating the next generation in financial analysis, risk management, and philanthropic strategy. Children were required to intern in various family enterprises and present investment proposals. The initial $100M grew to $200M over a decade, a seemingly lower financial return. However, due to a high Human Capital Multiplier, the subsequent generation not only preserved this wealth but actively expanded it through successful new ventures and shrewd portfolio rebalancing during crises. Despite a market downturn, their diversified portfolio provided stability, and their educated heirs identified and capitalized on distressed opportunities. After two generations, the family wealth grew to $400M, demonstrating the power of an adaptive system.

Implementation Strategy:

Shift from “Asset Accumulation” to “System Design”: Recognize that your goal is not merely to amass assets, but to build a self-repairing, self-optimizing financial ecosystem.

Implement Dynamic Diversification: Beyond basic asset allocation, truly diversify. This means actively managing correlations and incorporating “black swan” hedges (e.g., long-term out-of-the-money put options on broad market indices) that pay off when other assets falter. Regularly review and rebalance based on evolving macro-economic regimes, not just fixed percentages.

Invest in Human Capital as a Core Asset: This is paramount. Establish a structured financial education program for your heirs. This is not about lectures; it’s about practical involvement. Create mock investment committees, assign stewardship roles in family foundations, and encourage entrepreneurial ventures with seed capital (with clear performance metrics). Teach them about delayed gratification and the true cost of capital.

Calculate Your ICV (or a proxy): Even without complex models, estimate your own Intergenerational Capital Velocity. Are your children equipped to grow the wealth, or merely spend it? Is your portfolio truly resilient to unforeseen economic shocks? A low ICV score demands immediate action.

Establish a Generational Governance Framework: This goes beyond a simple will. Create a family constitution or set of guiding principles for wealth management, succession planning, and decision-making. This institutionalizes the “adaptive system” mindset and minimizes intergenerational conflict, which is a major source of entropy.

The ultimate measure of your success in building generational wealth is not the size of the initial inheritance, but the resilience and growth trajectory of that wealth across time, guided by a sophisticated framework that integrates financial acumen with human development.

This is the true “hidden alpha” for generational prosperity.