UltraTech Cement Share Price Outlook 2026: Growth Drivers, Expansion Plans & Investment Thesis

Investment Thesis & Summary

Here’s why: The company just posted solid quarterly numbers with 15% volume growth while everyone’s obsessing over price cuts. The stock’s trading below its 5-year average valuation even though they’re sitting on India’s largest cement capacity and executing a massive expansion that’ll add another 22.8 million tonnes. The market’s missing the forest for the trees.

Youtube Link:

Business Model & Operations

They make and sell cement - it’s that straightforward. With 194 million tonnes of capacity globally (188.66 mtpa in India), they’re the biggest player domestically with a 28% market share. Think of them as the default cement choice for most builders and contractors across the country.

The money comes from grey cement (the bulk of sales), white cement, ready-mix concrete, and building products. They’ve got plants spread across India, plus some operations in UAE, Bahrain, and Sri Lanka. Distribution network is massive - reaching tier-2 and tier-3 cities where India’s real construction boom is happening.

Recent moves include acquiring India Cements and integrating Kesoram Industries, which became effective this quarter. They’re not just buying companies; they’re systematically consolidating a fragmented industry. In the December quarter, they sold 38.87 million tonnes of cement - up 15% from last year. That’s real demand, not financial engineering.

Historical Financial Review

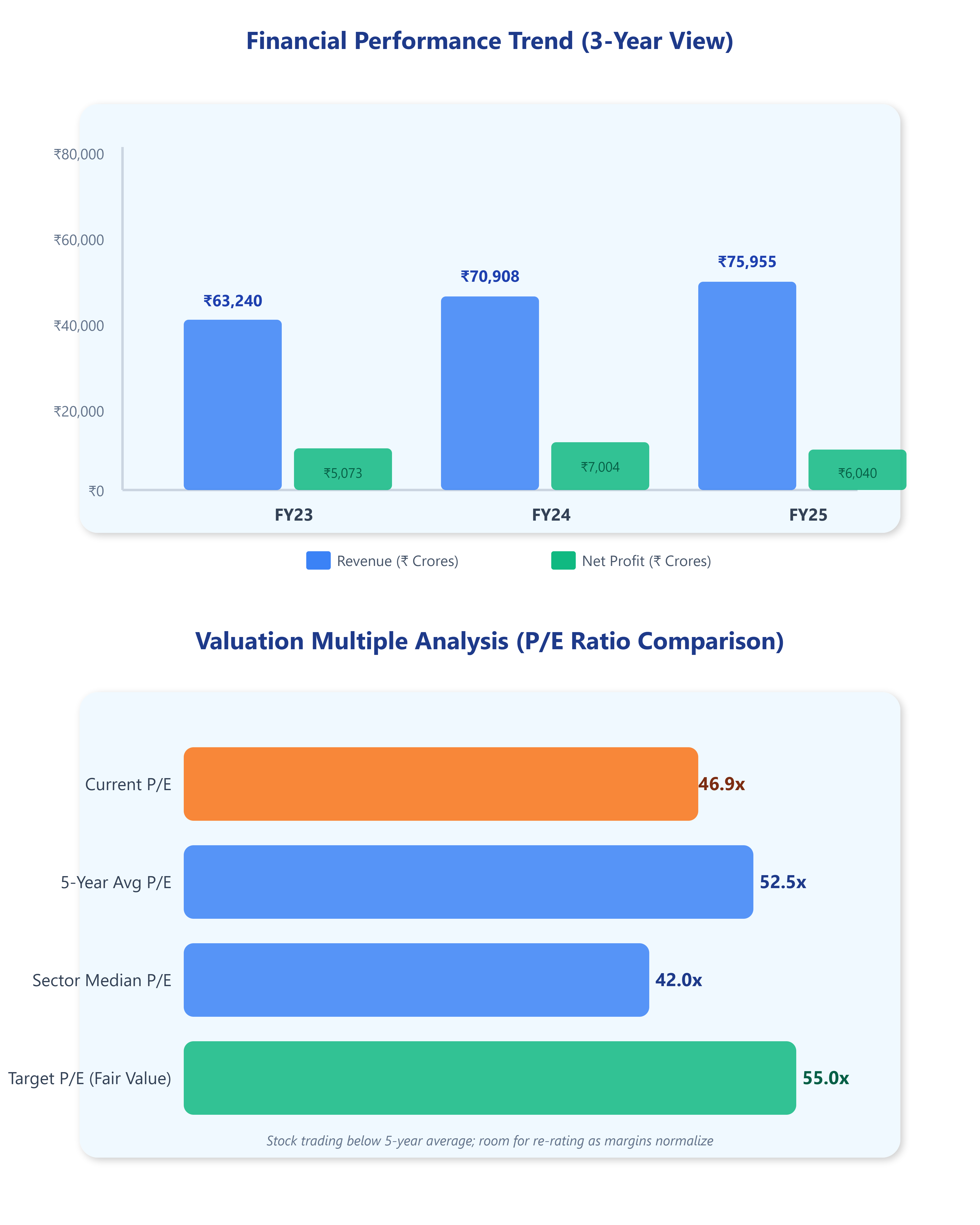

Over the last three years (FY23 to FY25), revenue grew at a 13% CAGR - from ₹63,240 crores to ₹75,955 crores. For the trailing twelve months ending December 2025, revenue hit ₹85,775 crores, showing the business is accelerating.

Last twelve months diluted EPS stands at ₹260.11. Operating cash flow has been strong at ₹10,673 crores for FY25, translating to roughly ₹362 per share. That’s healthy cash generation - the business converts sales into actual money, not just accounting profits.

But here’s the catch: FY25 saw net profit drop 14% to ₹6,040 crores from ₹7,004 crores in FY24. The culprit? Higher interest costs (debt from acquisitions), increased depreciation from new capacity, and margin pressure from cement price weakness. Management’s been clear about this - they took short-term pain to build long-term dominance. The December quarter showed this turning around with 27% profit growth year-on-year.

Debt levels have increased - net debt at ₹17,929 crores as of December 2025. But debt-to-EBITDA is at 1.08x, which is manageable. They’re using debt strategically to fund expansion, not to paper over operational issues.

Fundamental Valuation Metrics & Investment Call

Let’s talk numbers:

P/E Ratio: 46.9x based on FY25 earnings. Sounds expensive, right? Here’s context: the 5-year average P/E is around 50-55x, and at peak valuations it touched 65-70x. We’re actually trading below the historical mean. Given cement’s cyclical nature, buying when P/E compresses makes sense if you believe in the upcycle.

P/B Ratio: 5.06x. You’re paying ₹5 for every rupee of book value. This is justified for a market leader with pricing power and network effects. Smaller peers like Shree Cement and Ambuja trade at similar or higher multiples.

ROE: 9.29% for FY25, below the 3-year average of 10.4%. This is temporarily depressed due to acquisition integration costs and margin pressure. Pre-acquisition, ROE was healthier at 12-14%. As volumes improve and economies of scale kick in, ROE should normalize above 12%.

ROCE: 10.9% for FY25. Again, impacted by recent capex and integration. Historical ROCE has been in the 12-15% range.

EPS Growth: Last year was flat (actually negative). But the trailing twelve months show a recovery with TTM EPS at ₹260 versus FY25 EPS of ₹205. The December quarter delivered ₹58.55 EPS, up significantly from ₹47 in the previous quarter. Momentum is building.

Dividend Yield: 0.63%. They paid ₹77.50 per share for FY25, which is a 38% payout ratio. Dividends aren’t the story here - capital appreciation is.

The stock’s cheap here because the market got spooked by two things: cement prices falling post-GST reduction (which took rates from 28% to 12% on cement in September 2025), and near-term margin compression. But prices have already stabilized and are improving according to management’s latest commentary. Volume growth at 15% is strong - that’s demand catching up with India’s infrastructure push.

Sector median P/E is around 40-45x. We’re trading slightly above that, but for the market leader with the strongest balance sheet and biggest expansion pipeline, a 10-15% premium is justified.

Long-Term Outlook & Risk Assessment

5-15 Year Return Estimate: 12-15% annualized returns

Here’s the math: India’s cement consumption is around 420 kg per capita versus 1,500+ kg in developed markets. As GDP grows at 6-7% and urbanization accelerates, cement demand should compound at 7-8% for the next decade. They’re adding 22.8 mtpa capacity through brownfield and greenfield projects - that’s growing capacity faster than the market to grab share.

Management’s focused on three things: capacity expansion, cost optimization through scale, and premiumization of products. They’re spending ₹2,357 crores quarterly on capex. Most of this goes into backward integration (clinker capacity) and debottlenecking existing plants.

Promoters (Aditya Birla Group via Grasim) hold 59.28% - stable ownership with no signs of dilution. DIIs have been increasing stakes (17.45% now versus 14% two years ago), while FIIs have trimmed slightly. Smart money is accumulating.

What Could Go Wrong:

Raw material inflation - coal and petroleum coke prices spiking would hurt margins. They’ve got some captive mines but aren’t fully insulated.

Regulatory headwinds - cement’s been in the government’s crosshairs on pricing. CCI investigations or price controls could cap profitability.

Execution risk - integrating India Cements and Kesoram while simultaneously building new capacity is operationally complex. Any delay or cost overrun impacts returns.

Demand slowdown - if government infrastructure spending slows or real estate cools, volumes could disappoint. Cement moves with GDP growth; a recession kills the thesis.

What’s Going Right:

Infrastructure push is real - government’s betting big on roads, metros, airports. Housing for All programs are driving rural demand. That’s structural tailwinds for a decade.

Consolidation creates pricing discipline - top 5 players now control 60%+ of the market. Less fragmentation means better pricing power during upcycles.

They’re the lowest-cost producer at scale in many regions. Operating leverage kicks in as new capacity reaches 75-80% utilization.

Energy costs are falling - solar power adoption in plants is reducing electricity costs by 15%. Fuel efficiency improvements are ongoing.

The cement industry in India is entering a sweet spot: demand is strong, supply is consolidating, and input costs are moderating. For a market leader executing on expansion, the next 3-5 years look promising. Just don’t expect a smooth ride - cement’s cyclical, and there will be quarters where sentiment swings wildly on pricing data.

Company Name: UltraTech Cement Limited