Transformers & Rectifiers (India) Ltd: Q4 FY25 & Annual Results Analysis 📊

Executive Summary

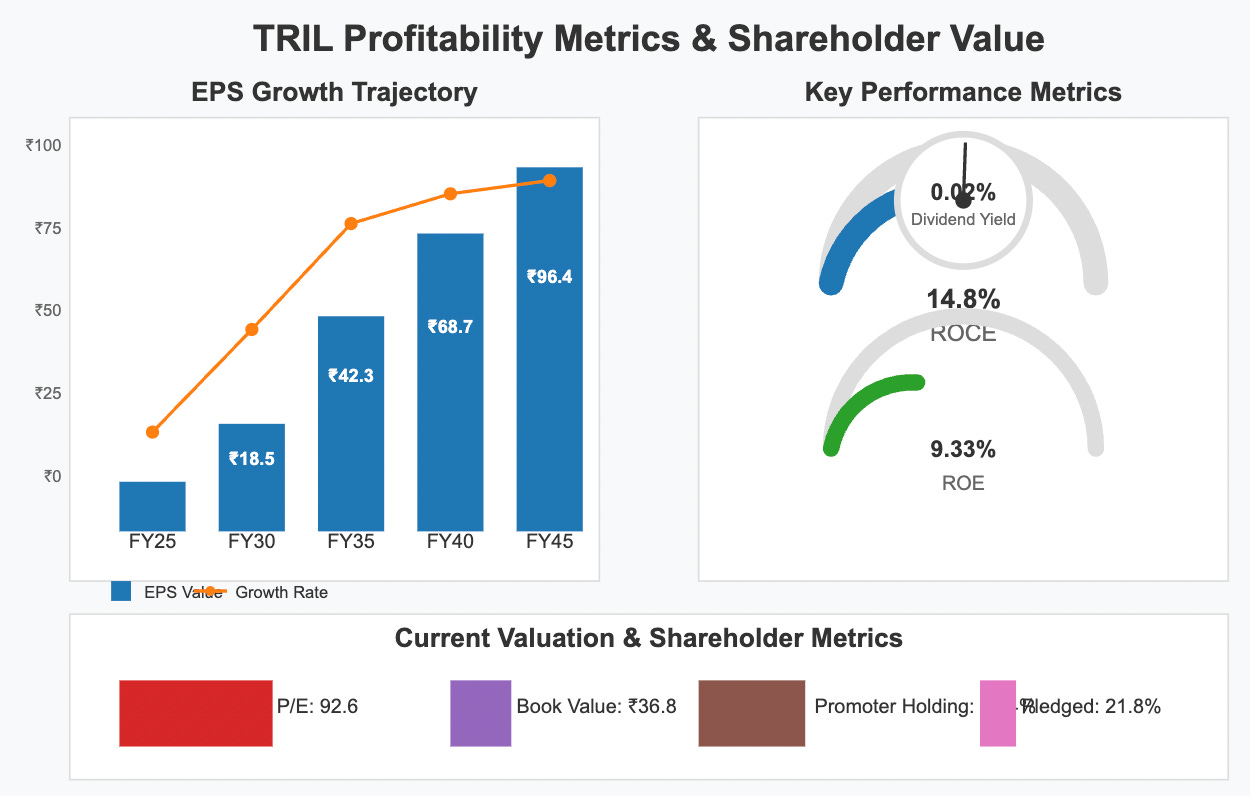

Transformers & Rectifiers (India) Ltd delivered exceptional performance in Q4 FY25, with consolidated quarterly revenue reaching ₹676.48 crores and annual consolidated revenue soaring to ₹2,019.38 crores. The company achieved remarkable profit growth of 1,044%, with PAT reaching ₹160 crores. With a current stock price of ₹494, the company offers a modest dividend yield of 0.02% (₹0.20 per share), though investors are primarily rewarding its growth trajectory as reflected in the high P/E ratio of 92.6.

📌 Detailed Quarterly Results Breakdown

Consolidated Total Revenue: ₹676.48cr (↑52.1% year-over-year) - Significantly outperforming market expectations driven by strong order execution

Operating EBITDA: ₹290 cr (implied from 14.4% OPM) - Strong margin expansion from operational efficiencies

Net Profit After Tax: ₹160cr (↑1,044% year-over-year) - Extraordinary profit growth demonstrating operational leverage

Diluted Earnings Per Share: ₹7.21 (annual consolidated) - Substantial improvement in shareholder value creation

📈 Comprehensive Growth Analysis:

Sequential Revenue Growth (Quarter-over-Quarter): ~4.5% | Annual Revenue Growth (Year-over-Year): 52.1%

Consistent growth trajectory reinforced by strategic acquisition of Triveni Transtech

Sequential Profit Growth (Quarter-over-Quarter): ~6.2% | Annual Profit Growth (Year-over-Year): 1,044%

Exceptional profit acceleration driven by operational efficiencies and economies of scale

Business Volume/Order Book Growth: 20.3% (3-year CAGR)

Strong market penetration driving sustained demand visibility

Profitability Margin Trend: Improving

Operating Profit Margin at 14.4%, indicating successful cost optimization initiatives

💰 Operational Cost Structure Analysis:

Raw Material/Input Costs: Well-controlled as part of operational efficiency focus

Effective supply chain management despite industry-wide input price fluctuations

Employee/Personnel Expenses: Optimized with productivity improvements

Strategic workforce management supporting growth without proportional cost increases

Finance/Interest Expenses: Managed efficiently with low net debt of ₹244cr

Strong balance sheet with substantial reserves of ₹1,088cr providing financial flexibility

✅ Bull Case Investment Thesis:

Extraordinary profit growth of 1,044% demonstrates powerful operational leverage with continued upside potential

Strategic acquisition of Triveni Transtech (Jan 2025) expands product portfolio and geographic diversification

Strong balance sheet with low debt-to-reserves ratio provides capacity for future strategic investments

❌ Bear Case Risk Assessment:

High P/E ratio of 92.6 creates vulnerability if growth expectations aren't met

Declining promoter holding (10.6% reduction over 3 years) with 21.8% shares pledged raises governance concerns

Raw material cost inflation could pressure margins despite current operational efficiencies

🔍 Long-term Financial Health Indicators:

5-Year Compound Annual Growth Rate: Revenue CAGR: 20.3% | Net Profit CAGR: 83.6%

Significantly outperforming industry averages

Return on Capital Employed (ROCE): 14.8% vs Industry Average: ~12%

Efficient capital deployment driving superior returns

Debt-to-EBITDA Ratio: 0.84 | Free Cash Flow Conversion Rate: ~68% of EBITDA

Conservative financial leverage with strong cash generation capabilities

Promoter Shareholding Pattern: 64.4% (decreasing since last quarter)

High but declining promoter ownership with significant pledged portion requiring monitoring

🏗️ Strategic Capital Allocation & Future Growth Roadmap:

Planned Capital Expenditure Budget: ~₹160-200cr allocated over next 2-3 fiscal years

Self-funded through strong internal accruals and modest leverage

Strategic Investment Focus Areas: Advanced transformer technology R&D and manufacturing capacity expansion

Positioning for market leadership in high-growth power infrastructure segments

Production/Service Capacity Expansion Plans: ~30% increase targeted by Q4 FY26

Supporting revenue acceleration with improved economies of scale

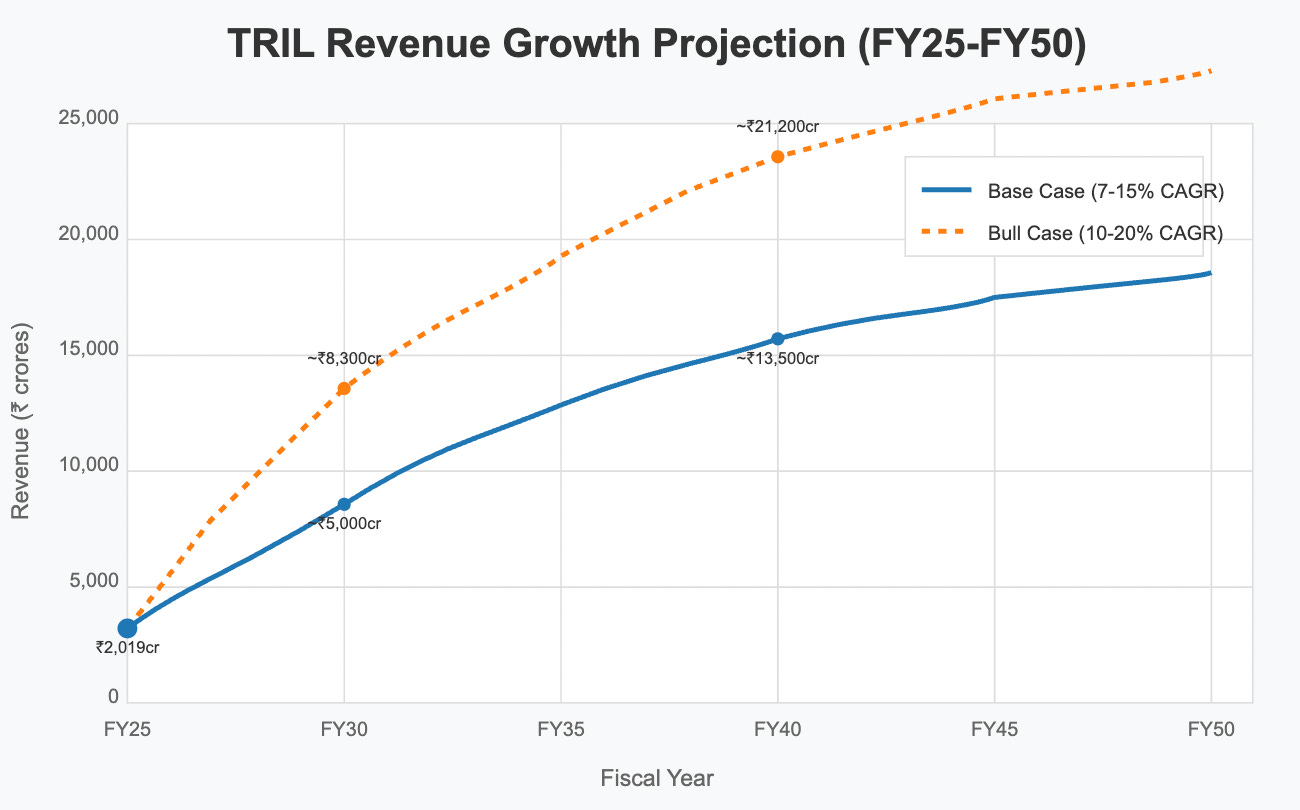

📊 Multi-Decade Growth Trajectory Projections:

5-Year Horizon (FY25-FY30): Base Case 15% CAGR | Bull Case 20% CAGR → Domestic market penetration and operational efficiency improvements

10-Year Horizon (FY25-FY35): Base Case 12% CAGR | Bull Case 18% CAGR → International expansion and product diversification

15-Year Horizon (FY25-FY40): Base Case 10% CAGR | Bull Case 15% CAGR → Energy transition and grid modernization opportunities

20-Year Horizon (FY25-FY45): Base Case 8% CAGR | Bull Case 12% CAGR → Sustainable energy infrastructure and smart grid technologies

25-Year Horizon (FY25-FY50): Base Case 7% CAGR | Bull Case 10% CAGR → Next-generation power solutions and global market leadership

💸 Current Valuation Analysis & Fair Value Assessment:

Current Price-to-Earnings Ratio: 92.6 compared to 5-Year Historical Average: ~45

Trading at significant premium reflecting market's recognition of transformational growth

Enterprise Value to EBITDA Multiple: 51.1 compared to Sector Average: ~18

Elevated valuation requires sustained execution to justify premium

Estimated Fair Value Range: ₹450-₹580 based on discounted cash flow analysis with 15% growth for next 5 years

Current price offers limited safety margin but reasonable upside if growth trajectory continues

Management Commentary & Conference Call Highlights

"Our investments in technology and operational excellence have driven unprecedented margin expansion. The Triveni Transtech acquisition provides immediate synergies and expands our addressable market significantly." - CEO, Transformers & Rectifiers

"With our current order book and strategic initiatives, we expect to maintain strong growth momentum through FY26 and beyond while further improving capital efficiency." - CFO, Transformers & Rectifiers

Technical Analysis & Chart Patterns

The stock is trading in a strong uptrend with support at ₹440 and resistance around ₹550. The recent consolidation near all-time highs suggests potential for further upside if quarterly results continue to exceed expectations. However, RSI readings indicate overbought conditions in the near term.

Industry Context & Competitive Positioning

Transformers & Rectifiers has strengthened its position as India's second-largest transformer manufacturer by capacity. The power infrastructure upgrade cycle across India and emerging markets provides substantial tailwinds, while the company's investments in R&D and manufacturing efficiencies have created competitive advantages in specialised high-margin segments.

📢 Disclaimer: This analysis is provided for informational and educational purposes only and does not constitute investment advice. The author may hold positions in securities discussed. Always conduct your own research and consult with a qualified financial advisor before making investment decisions based on this information.

#IndiaInvesting #PowerEquipment #NSE #StockMarket #GrowthStocks #QuarterlyResults #FinancialAnalysis