This Quiet Pharma Manufacturer Is a Secret Engine Behind Global Medicines

01 /Investment Thesis & Summary

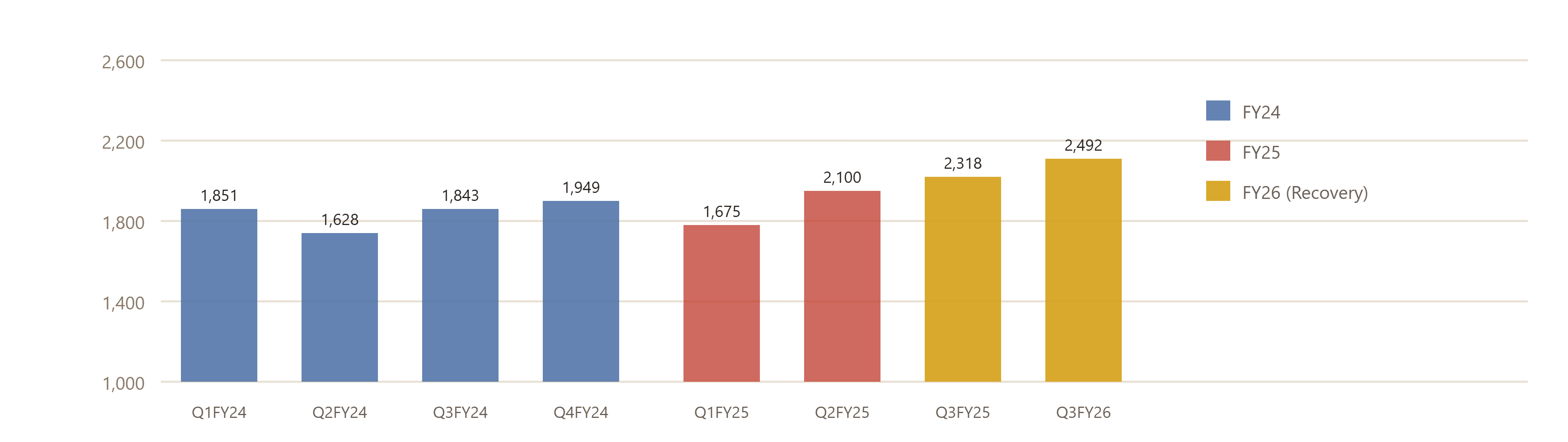

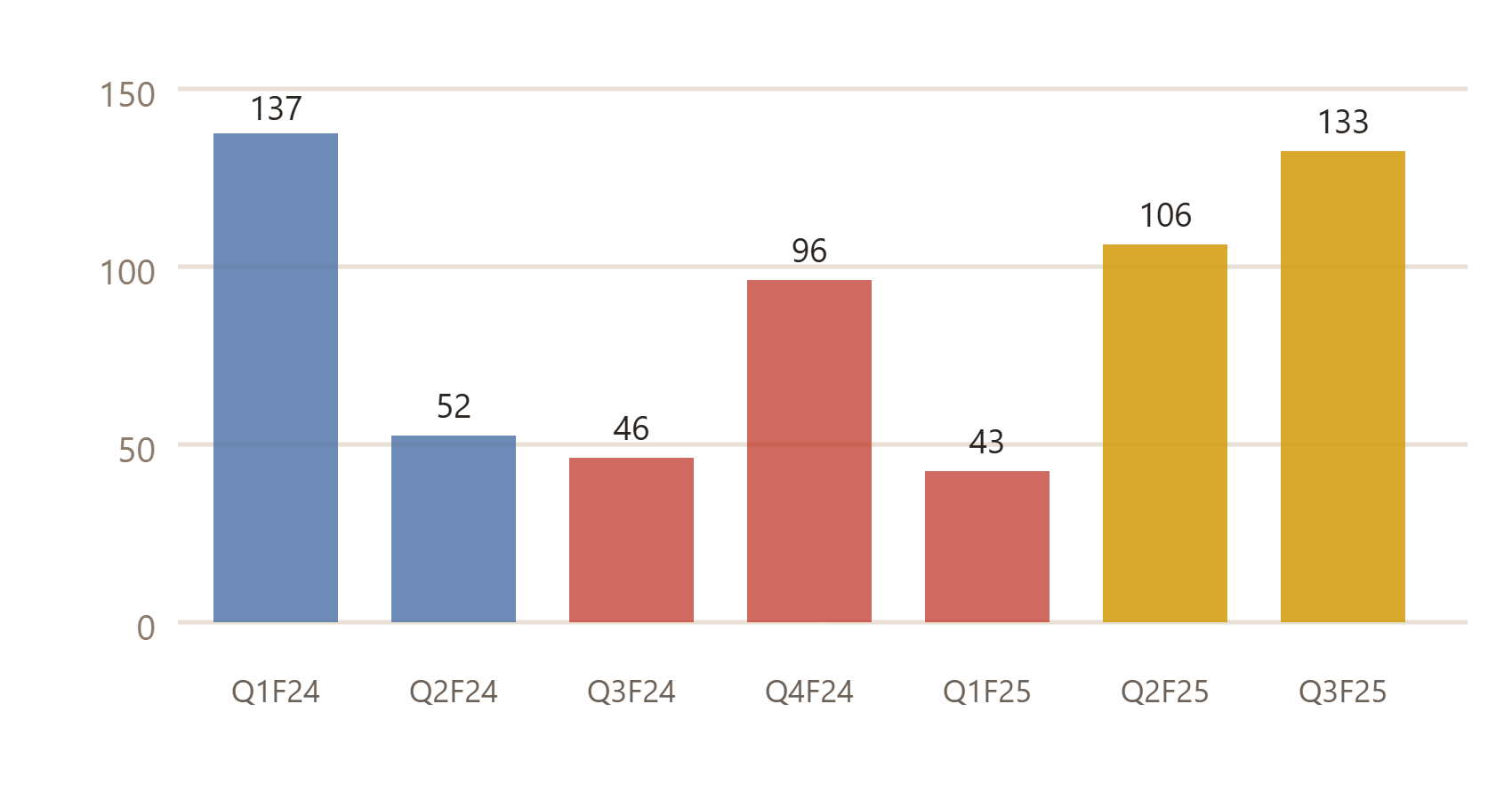

Here’s the setup: this company went through a rough patch in FY24 and FY25 — profits dropped, margins got squeezed, and everyone quietly moved on. But look at the last three quarters and a very different picture is emerging. Revenue has climbed steadily, profits have nearly tripled from their trough, and exports just hit their highest-ever share of revenues at 65%.

The stock is still pricing in the bad old days. At ₹433, you’re buying into one of India’s most integrated specialty chemicals businesses at a trailing P/E around 54x on trough earnings — but on normalised earnings for FY27, that multiple compresses dramatically. The recovery is real, the capex cycle is nearly over, and free cash flow is set to improve meaningfully as spending slows.

“Buy the recovery, not the peak. This company’s worst earnings days are behind it — and the market hasn’t fully priced that in yet.”

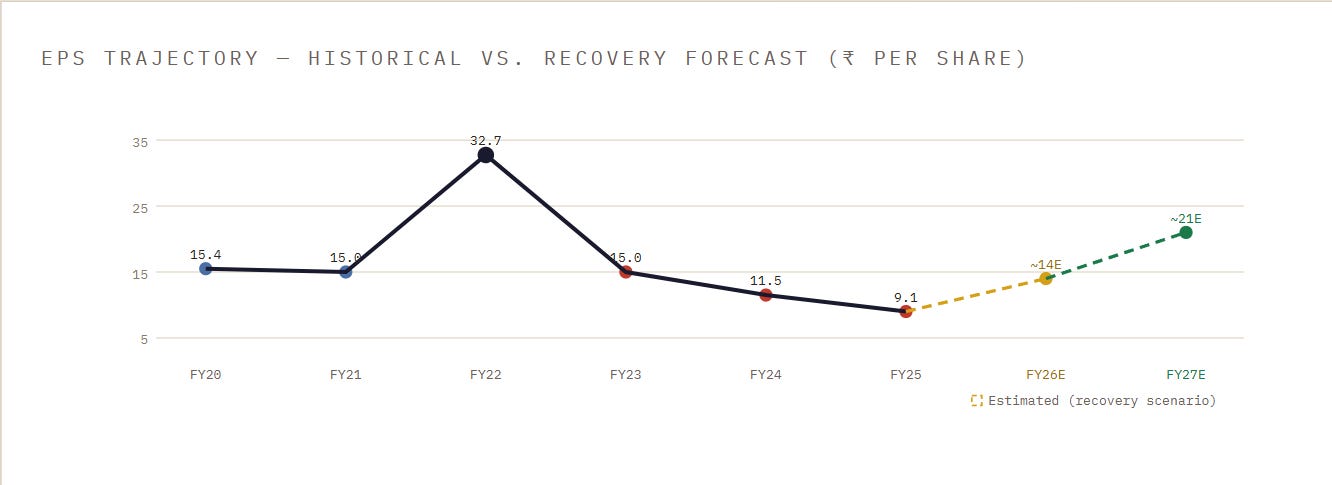

The target price of ₹590 is based on ~28x FY27 estimated earnings of ₹21 per share — a modest re-rating as profitability normalises. That’s roughly 36% upside over 12–18 months. Over a 5–7 year horizon, if the company executes its downstream integration strategy, a ₹900–1,100 range is achievable as margins expand back toward historical levels.

Youtube Link:

02 /Business Model & Operations

The company makes specialty chemicals — a category that sits between basic commodities and advanced materials. Think of it as taking cheap raw materials like benzene, toluene, and sulphur, and transforming them through chemistry into high-value intermediates that go into everything from pesticides and dyes to polymers and pharmaceuticals.

The core of the business is the NCB (nitro-chloro-benzene) chain. That’s the chemical backbone that feeds into agrochemicals, dyes, pigments, and polymer additives. The company holds a top 1–4 global ranking in about 75% of its product portfolio. That’s not a marketing claim — it reflects decades of process chemistry know-how that competitors genuinely struggle to replicate at this scale and cost.

Geography matters here. Exports make up 65% of revenues as of Q3 FY26 — the highest ever. This reflects two structural tailwinds: China’s “anti-involution” policy (which is effectively reducing Chinese chemical export subsidies, pushing global buyers to India) and the India-EU trade negotiations that are opening new corridors.

Operations are spread across Gujarat (Vapi, Jhagadia, Dahej SEZ, Kutch) and Maharashtra (Tarapur). Jhagadia is the growth engine right now — a massive Zone IV expansion is underway with a ₹1,100 crore capital spend in FY26. New products like MMA (methyl methacrylate acid chloride), DCB (dichloro-benzene), and PEDA are being commissioned. MMA alone contributes 50–60% of US export revenues.

The pharma demerger in FY23 (creating Aarti PharmaLabs) was a smart move. It cleaned up the company’s focus. What remains is a pure-play specialty chemicals business with a cleaner capital structure and a sharper strategic lens.

03 /Historical Financial Review

The 3-year revenue CAGR is approximately 6% — not spectacular on paper, but the story is more nuanced than that number suggests. Revenue actually grew from ₹6,619 crore in FY23 to ₹7,271 crore in FY25 — a period that saw significant global chemicals pricing deflation and China-related demand disruptions. The company held volume growth while coping with price headwinds. That’s a different narrative than simple underperformance.

The earnings picture is where it gets uncomfortable — and interesting. Diluted EPS fell from ₹15.04 in FY23 to ₹9.13 in FY25, as margin compression hit profits hard. But LTM (last 12 months) EPS is now tracking around ₹8.03 and is climbing fast. Q3 FY26 alone printed ₹3.70 EPS — 49% above analyst estimates. The quarterly earnings trajectory tells a powerful story of recovery.

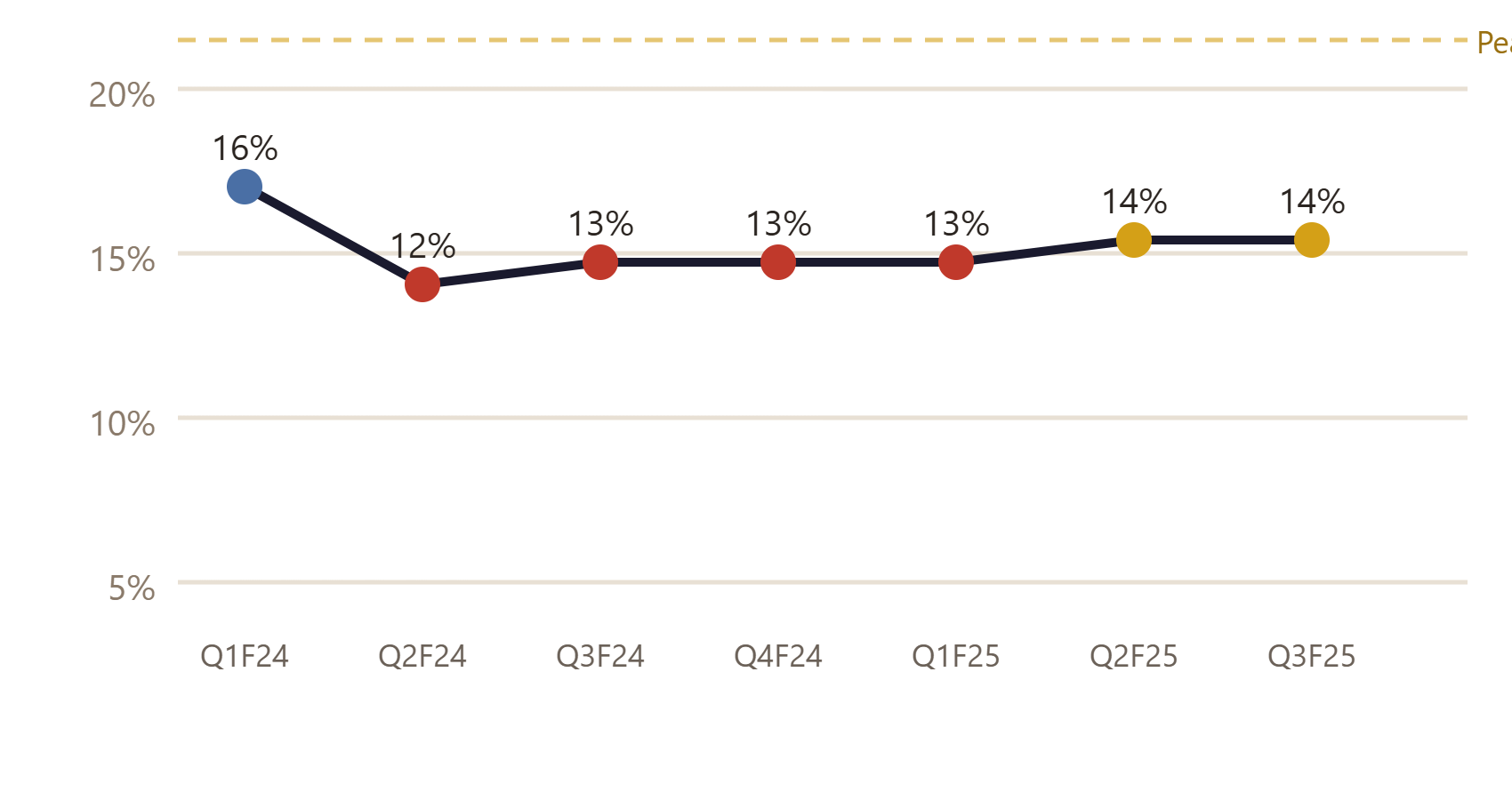

The margin story is the key watch item. Operating margins sat at 28% in FY22 at the peak of the super-cycle. They’ve compressed to 13–14% now. That’s partly a function of raw material costs, partly the dilution effect of the new plants not yet running at optimal utilisation. As Zone IV fills up and capacity utilisation rises, there’s a credible path back toward 16–18% over the next 2–3 years.

04 /Annual Financials — The Long View

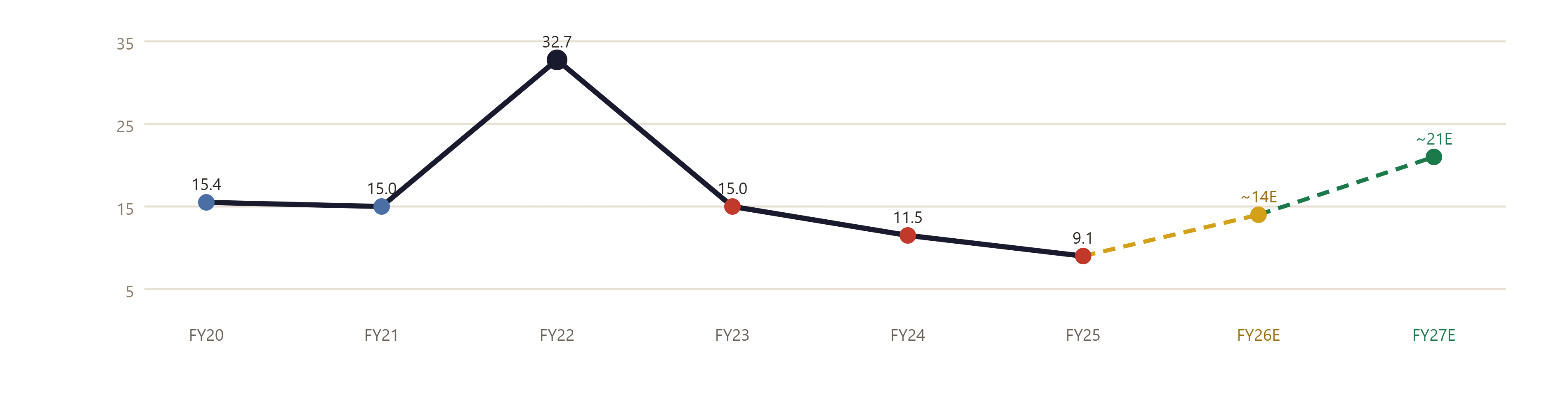

That FY22 profit spike to ₹1,186 crore was extraordinary — a perfect storm of high product prices, low input costs, and full capacity utilisation. It’s gone now, and the market is right not to expect a repeat immediately. But what’s worth watching is that revenues in FY25 and TTM are already at record highs. The earnings will follow once the new capacity fills up and interest costs (which jumped from ₹86 crore in FY21 to ₹275 crore in FY25 due to capex) normalise.

Key Ratio Check: P/E of ~54x on TTM earnings looks expensive. But on FY27 estimated earnings of ~₹21 per share (assuming margin recovery to 16%), that compresses to ~20x. Book value stands at ₹158 per share. Price-to-book of ~2.7x is reasonable for a market-leading specialty chemicals company with a strong moat.

05 /Growth Drivers & Key Risks

Let’s talk about what could make this work — and what could go wrong. Both deserve honest attention.

What’s working in their favour: The China anti-involution policy is a genuine structural tailwind. China removing export subsidies on chemicals is pushing global buyers toward Indian producers. This company is already seeing this — record export share of 65% in Q3 FY26. Second, the Zone IV Jhagadia complex is a transformational platform. New products like MMA, PDCB, and DCB are high-value, import-substitution plays with strong demand visibility. Third, the India-US and India-EU trade dynamics are opening up export lanes. Management has flagged that US tariff levels (now at 18% range, down from 50%+) are manageable and baked into contract negotiations.

The capex tail is shortening. FY26 capex is ₹1,100 crore — heavy, but management guided it drops significantly in FY27. That means debt stops growing, interest burden stabilises, and free cash flow starts to flow. That’s when earnings really start accelerating.

06 /Valuation & Expected Returns

The current price of ₹433 gives a market cap of ~₹15,699 crore on about 362.6 million shares. Here’s how the numbers stack up across time horizons:

12-18 Month Target (₹590): At ₹590, the stock trades at ~28x FY27E earnings of ₹21 per share. That’s a modest re-rating from current levels — not heroic. Just a return to normal valuation once the market sees two straight quarters of strong earnings. Upside: ~36%.

5-Year View: If operating margins recover to 18% by FY29–30 on revenues of ~₹11,000–12,000 crore (a reasonable assumption given the new capacity coming online), EPS could reach ₹35–40. At a 25x multiple, the stock would be in the ₹875–1,000 range — roughly 2x to 2.3x from current levels. That’s a 15–18% CAGR over 5 years.

10-Year View: The benzene-based specialty chemicals industry is structurally growing at 8–10% annually in India. If the company maintains its competitive position and executes downstream integration into advanced materials, ₹1,500–1,800 is plausible on a 10-year horizon — implying a 13–15% CAGR. Not a multi-bagger from here, but a solid compounder.

The core thesis is simple: You’re buying a world-class specialty chemicals franchise at trough earnings, right as the capex cycle ends and the recovery cycle begins. The risk-reward over 18–36 months is attractive.

07 /What To Watch — Your Checklist

This investment thesis isn’t a set-and-forget. Here’s what you need to track every quarter to know if the story is playing out or breaking down:

1. Operating Margin Trend. Margins need to move from the current 13–14% toward 16% by end of FY27. If they’re stuck at 13% even as volumes grow, the thesis is weakening. Watch for each quarterly OPM number.

2. Zone IV Commissioning Progress. The Superform JV (agrochemicals and coatings) is expected in Q1 FY27. RESL JV (circularity/recycling) in H1 FY27. Any delays push the earnings recovery further out. Confirm in quarterly filings.

3. Export Revenue Mix. The 65% export share is a positive. If this holds or grows, margin quality improves. A drop back toward 55% would signal either US tariff disruption or volume weakness.

4. Interest Cover Ratio. Currently weak. Watch if EBITDA growth is outpacing interest cost growth. When EBITDA/interest exceeds 3x consistently, the balance sheet pressure eases materially.

5. US Tariff News. Any escalation above the current ~18% level on Indian chemical imports into the US is a direct headwind. Track US trade policy announcements.