Everyone Drinks It. Almost No One Owns the Business Behind It.

Everyone drinks it. Almost no one owns it.

Revenue is up 18% this quarter. Profit is up 19%. Africa is barely even started.

This company delivers fizz across 14 countries — and still has half of India left to reach.

If you’re not watching this, you’re already late.

Section 1

Section 2

What the market is missing

The market sees this as a “soft drink company.” That framing is limiting and lazy.

What it actually is: a logistics and distribution empire that happens to fill bottles. The real moat isn’t the brand. It’s the cold chain. The fleet. The relationships with 3 million+ retail touchpoints across India and 13 other countries.

The market is also ignoring Africa. The continent is early-stage, fast-growing, and operationally maturing. South Africa alone, through recent acquisitions, represents a new growth engine that hasn’t been priced in.

And then there’s the energy drink category. Sting — the energy brand — is growing at breakneck speed among younger urban consumers. It’s not an add-on. It’s a category expansion play hiding inside an existing distribution network.

The FII holding is at a five-quarter low. Retail investors have barely started to notice. That’s not a warning sign — that’s a setup.

Youtube Link:

Section 3

The business, simplified

Think of the world’s most recognized beverage brand. They make the recipe. Someone else makes the drink, fills the bottle, builds the warehouse, drives the truck, and ensures the bottle reaches a shop in rural Bihar or downtown Morocco at the right temperature.

That “someone else” is this company.

They hold exclusive franchisee rights from one of the world’s top two beverage giants — across a massive and growing geography. They produce, bottle, and distribute: Pepsi, Mountain Dew, Mirinda, 7Up, Slice, Sting, Gatorade, Tropicana, Aquafina, and more.

Who pays them? Ultimately, the end consumer. But the relationship is sticky because it’s built on licensed territory, exclusive rights, and capital-intensive infrastructure that cannot be replicated overnight.

They don’t rely on a single product. They’re a platform. And platforms compound.

Section 4

Financial momentum

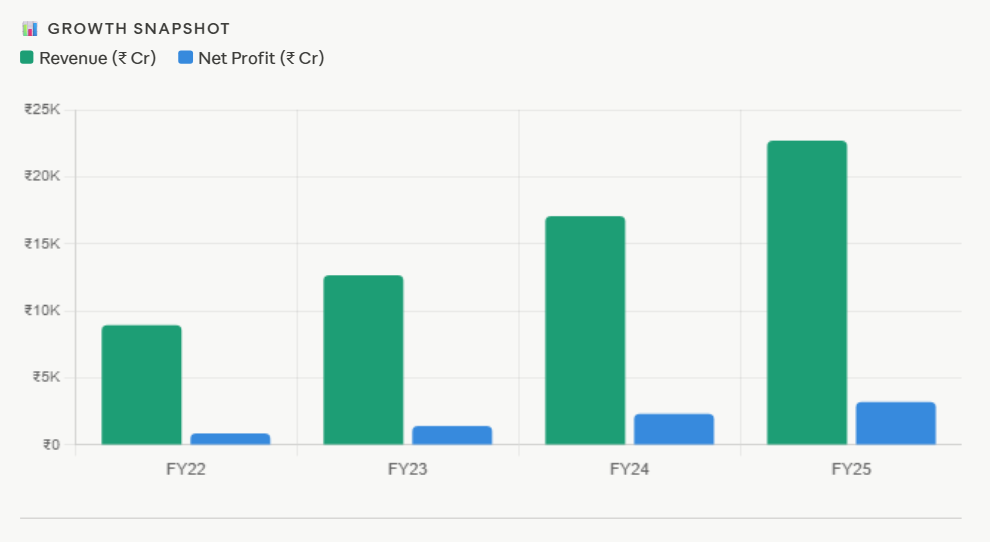

Revenue has been on a consistent upward march for three straight years — through supply chain stress, raw material inflation, and global macro noise.

Q1 CY2026: Revenue ₹6,574 Cr — up 18% YoY. Profit before tax: ₹1,163 Cr — up 19% YoY. EBITDA: ₹1,529 Cr — up 21% YoY. Gross margins improved 62 bps to 55.2%, despite an inflationary raw material environment. That’s not luck. That’s pricing power and scale.

Full-year revenue for FY2025: ₹22,693 Cr. Full-year profit: ₹3,209 Cr. The trajectory is clear and consistent.

This is not just a beverage business.

It’s a territory control business.

Whoever controls the cold chain, controls the shelf. And the shelf is everything.

Section 5

Key triggers to watch

El Niño-driven heatwaves in India → volumes spike, revenue follows

Africa scale-up: Twizza and Crickley Dairy acquisitions entering ramp phase

Sting energy drink gaining urban share, premium pricing lifts blended margins

New greenfield plants in Prayagraj, Himachal, Bihar & Meghalaya boost capacity by ~30%

JV for visi-cooler manufacturing reduces input costs — backward integration kicking in

Carlsberg distribution test in Africa → possible premiumisation lever

FII re-entry as earnings visibility improves could re-rate the stock quickly

Section 6

Smart money signal

The stock is up 36% from its 52-week low. But it’s still 7% below its all-time high. That’s a meaningful gap — and the fundamentals that created the high are improving further.

Institutional funds are holding, not exiting. Promoters have not sold. The stock’s one-year beta is 0.7 — low volatility relative to the market. This is how quiet accumulators build positions before the next leg.

Section 7

Risks

Valuations are full. PE of ~60x is pricing in significant execution. Any earnings miss will be punished hard.

Raw material inflation — PET resin, sugar, and packaging costs remain volatile. Margins could compress if sourcing discipline slips.

Africa integration risk — multiple acquisitions in a short period. Operational complexity grows. Synergies take time.

Monsoon risk — excessive rain in peak summer suppresses beverage demand. Weather is a real variable in this business.

Regulatory risk — health-related taxes on carbonated drinks remain a long-term policy threat globally.

Franchise dependency — the entire business rests on one key relationship. Any disruption to that contract changes everything.

Section 8

Final verdict

Why should someone track this right now?

Because this is one of the few businesses in India that earns money every time someone is thirsty. That sounds simple. The compounding of that simplicity over 14 countries and 30 years is what makes it extraordinary.

The Africa chapter is just beginning. The energy drink tailwind is secular. The capacity expansion is almost done. And the market, for a brief moment, has looked away.

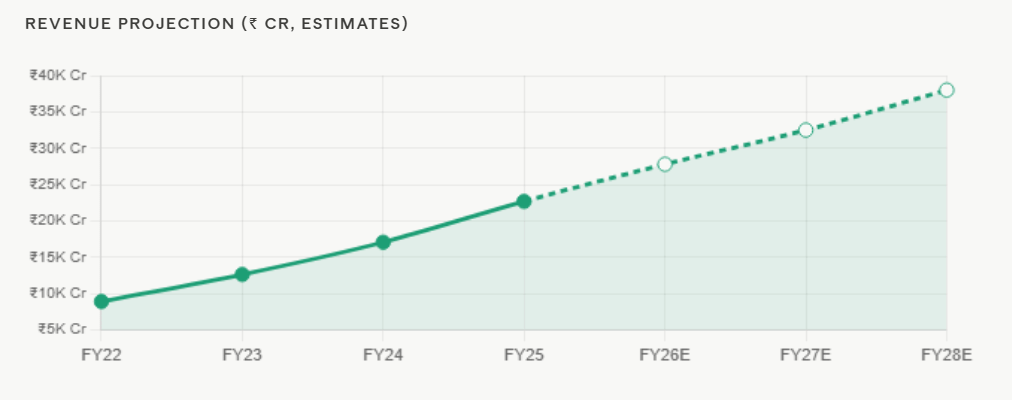

Corrections like these — where fundamentals keep improving but the stock drifts — are not threats to long-term investors. They are gifts. This business has compounded revenue at 36%+ CAGR over three years. Very few companies in India can say that.

Track it. Study the seasonality. Wait for the right entry. The story isn’t over — it’s barely in its second chapter.