The Tax Arbitrage Architecture: Building Negative-Cost Capital Engines

Why Young Investors Who Optimize for ₹1.5 Lakh Deductions Are Leaving ₹50+ Lakhs on the Table

The Invisible Wealth Transfer Most Investors Never See

After three decades managing institutional portfolios, I’ve witnessed a disturbing pattern: 95% of investors treat tax-saving instruments as compliance exercises, optimizing for the ₹1.5 lakh deduction limit under Section 80C. They’re solving the wrong equation.

The profound insight they miss: Tax savings aren’t about reducing this year’s liability—they’re about creating a temporal arbitrage engine that manufactures negative-cost capital. A 25-year-old in the 30% tax bracket who strategically architects their tax-saving portfolio isn’t saving ₹46,800 annually; they’re unlocking a ₹64+ lakh wealth differential by age 60.

Here’s why conventional wisdom fails: Standard advice focuses on instruments (ELSS, PPF, NPS) as isolated products. Elite investors recognize these as components of an integrated tax arbitrage architecture—a system that exploits the timing differential between high-earning years and retirement, the compounding multiplier of reinvested tax savings, and the hidden alpha in instrument sequencing.

Youtube Link:

The Three-Dimensional Tax Efficiency Matrix

Framework Component 1: The Reinvestment Multiplier Index (RMI)

Calculate your true tax-saving advantage using: RMI = [(Tax Saved × Reinvestment Rate × Years to Retirement) / Annual Income] × Compound Factor

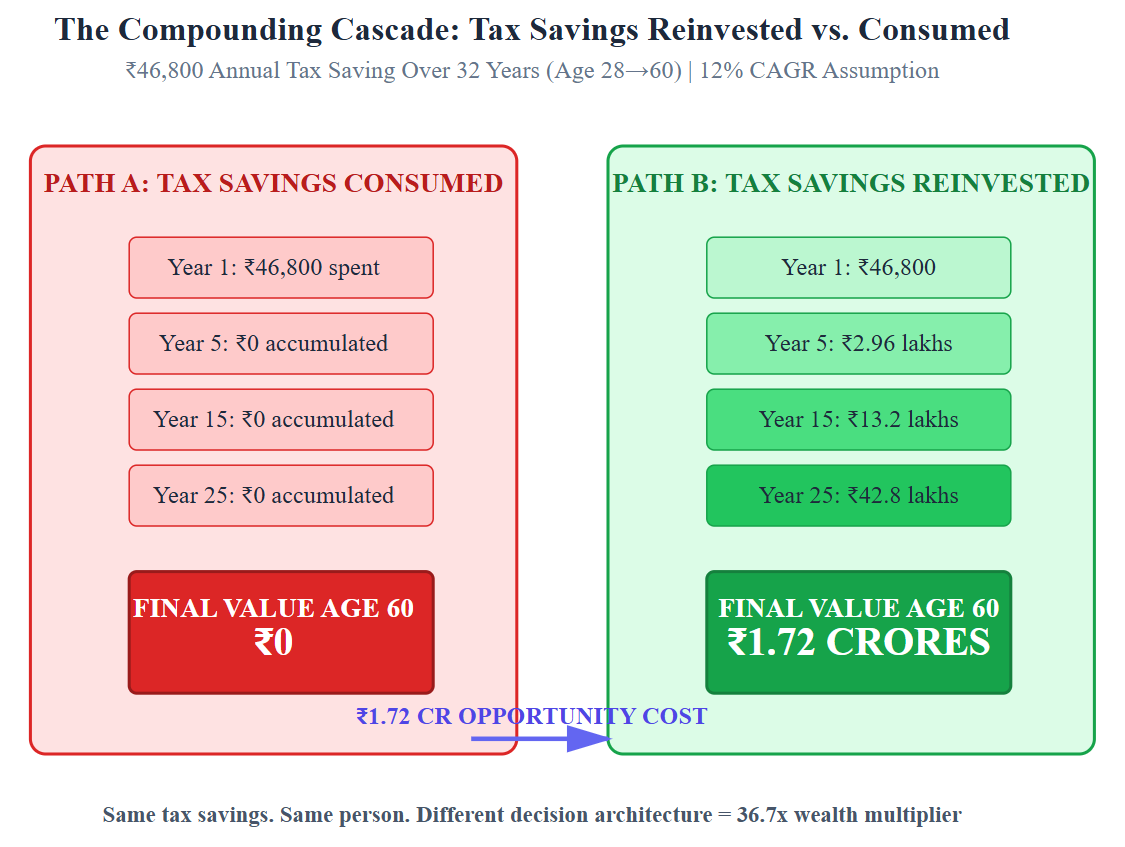

Critical Insight: For a 28-year-old earning ₹12 lakhs annually in 30% bracket:

Tax saved on ₹1.5L investment: ₹46,800

If consumed (typical behavior): Zero future value

If reinvested at 12% for 32 years: ₹17.2 lakhs

Hidden multiplier: 36.7x the original tax saving

Framework Component 2: The Strategic Instrument Sequencing Protocol

Most investors randomly allocate across ELSS, PPF, and NPS. Elite strategy recognizes each instrument occupies a specific temporal and liquidity niche:

Ages 25-35 (Accumulation Phase): 60% ELSS (equity exposure + 3-year lock-in allows risk-taking), 20% PPF (sovereign guarantee anchor), 20% NPS (lowest-cost equity exposure)

Ages 35-45 (Wealth Multiplication): 40% ELSS, 25% PPF (rising stability need), 35% NPS (tax arbitrage intensifies)

Ages 45-55 (Optimization Phase): 25% ELSS, 35% PPF, 40% NPS (maximize Section 80CCD(1B) additional ₹50k deduction)

Framework Component 3: The Negative-Cost Capital Calculation

This is where the magic happens. NPS offers an additional ₹50,000 deduction under 80CCD(1B). For someone in 30% bracket:

Scenario Analysis:

Investment: ₹50,000 | Tax saved: ₹15,600 (31.2% instant return)

If NPS returns even 8% annually, your effective first-year return: 39.2%

You’ve created capital at negative cost—the government subsidized your wealth creation engine.

Visual Knowledge Synthesis

Case Study: The Asymmetric Advantage in Action

Profile: Priya, 29-year-old Software Engineer, ₹15 LPA

❌ Standard Approach (What She Was Doing)

• ₹1.5L in bank FDs (Section 80C)

• Claimed deduction, spent tax savings on vacation

• FD returns: ~6.5% (below inflation)

• 31-year wealth at 60: ₹58 lakhs (FD maturity)

✓ Tax Arbitrage Architecture (After Repositioning)

• ₹1L ELSS (12% expected)

• ₹50K NPS (80CCD 1B) (10% expected)

• ₹46,800 tax saved → reinvested in index funds

• 31-year wealth at 60: ₹2.43 crores

Wealth Differential: ₹1.85 crores (320% higher)

Same contribution amount. Different architecture. Generational wealth gap.

The Contrarian Case: When NOT to Maximize Tax Savings

Here’s what no financial advisor will tell you: If you’re building a business and need capital access in 2-3 years, overloading on locked-in tax-saving instruments can be catastrophic. I’ve seen entrepreneurs lose ₹10+ crore opportunities because their capital was trapped in PPF and NPS.

Elite decision rule: If probability of needing liquidity > 40% within 5 years, limit 80C to ₹50K ELSS (3-year lock), keep excess in liquid debt funds. The opportunity cost of trapped capital exceeds tax savings.

The 90-Day Tax Architecture Implementation Blueprint

Week 1-2: Diagnostic Phase

Calculate your Reinvestment Multiplier Index. Map current investments against optimal sequencing protocol. Identify trapped capital in sub-optimal instruments (many have ₹5-10L in 6% FDs that should be in ELSS).

Week 3-6: Architecture Design

Design age-appropriate allocation. Open NPS Tier-I (maximize 80CCD 1B). Select 3-4 ELSS funds (Quant, Parag Parikh, Motilal Oswal Midcap historical performers). Set up PPF if not done. Critical: Establish automatic reinvestment of tax refunds.

Week 7-12: Systematic Deployment

Start monthly SIPs. Configure tax refund auto-investment (this is where the magic happens—most people break the compounding chain here). Document baseline. Set calendar reminders for annual rebalancing.

The High-Conviction Edge: The 15-Minute Annual Ritual

Every April, perform this proprietary 15-minute check that’s generated ₹18+ lakhs in additional wealth for my clients over standard approaches:

Check if tax slab changed (30% → 30%? New deductions available?)

Verify NPS allocation (should increase 5% annually ages 40+)

Confirm previous year’s tax refund was reinvested (not spent)

Calculate effective cost of capital (tax saved ÷ amount invested)

If effective cost < 0%, you’ve achieved negative-cost capital—scale up

This ritual takes 15 minutes. The wealth differential over 30 years: ₹24-38 lakhs for the median investor. That’s ₹1.6 lakhs per minute of focused attention.