The Silent Force Powering India’s Next Industrial Boom

Section I

Investment Thesis & Summary

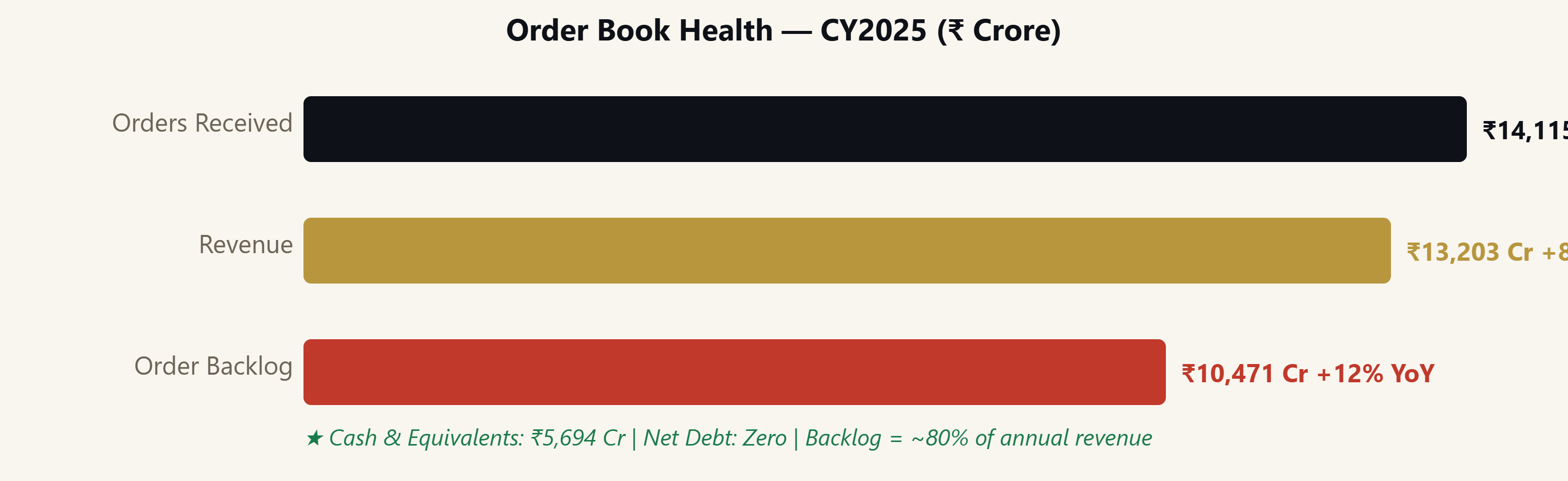

Here’s the plain truth: this is a company India needs. Not in a vague, feel-good way — in a very literal, contractual, backlog-sitting-at-₹10,471-crore way. Every factory going up, every data centre humming, every metro rail running, every solar plant feeding into the grid — they all need what this company makes. And the orders keep coming in faster than the revenue goes out.

“India’s infrastructure and industrial buildout is a decade-long story. This company has a front-row seat and a full order book to prove it.”

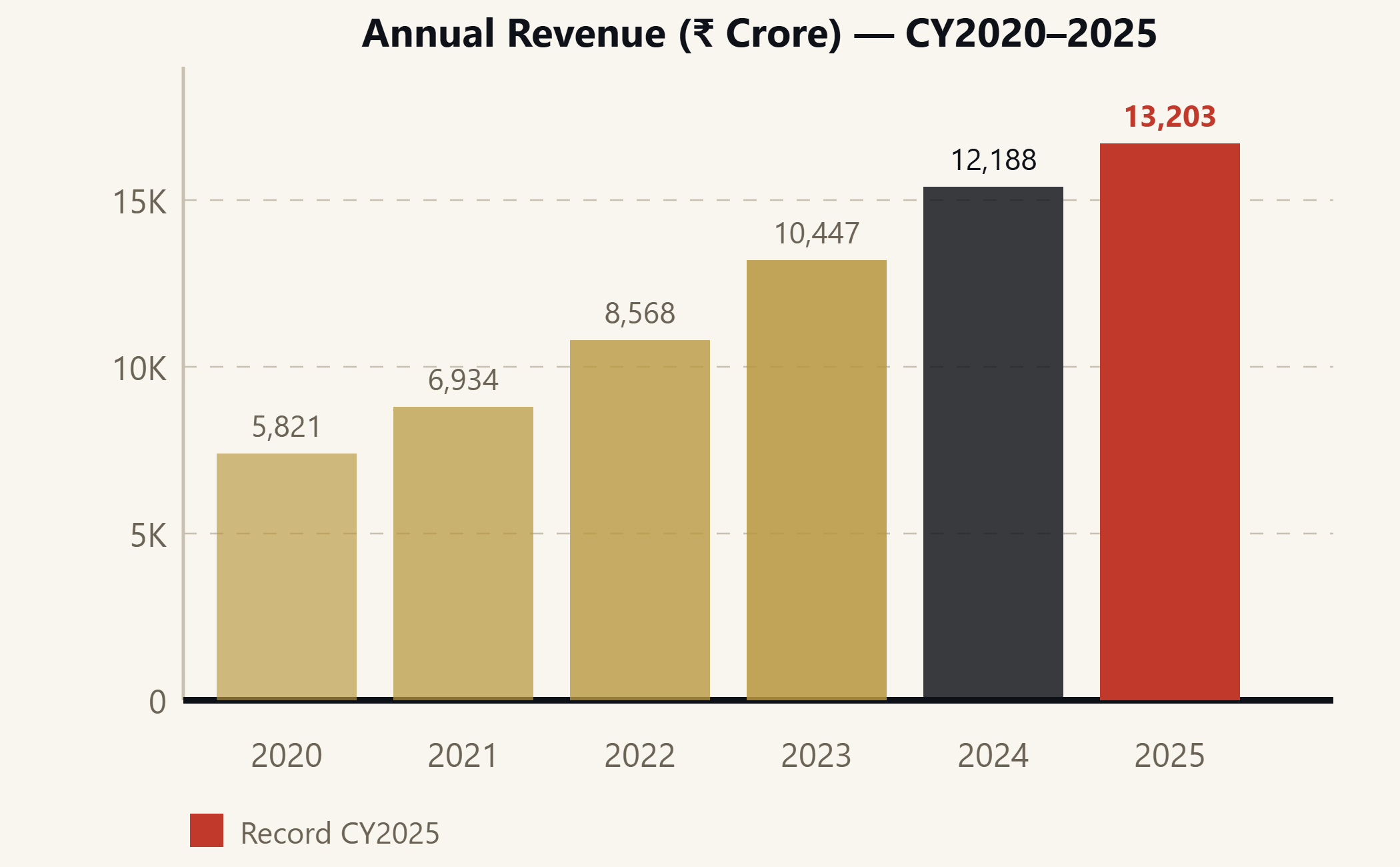

For the full calendar year 2025, this business posted record orders of ₹14,115 crore and record revenues of ₹13,203 crore — both up 8% year-on-year. The order backlog of ₹10,471 crore is essentially future revenue already locked in. That’s 80% of a full year’s sales sitting as confirmed, executable work. The cash pile stands at ₹5,694 crore. The company carries virtually zero debt.

So why are we saying Buy now rather than six months ago? Honestly, the stock pulled back sharply from its ₹7,960 peak as margin pressures — higher material costs, forex headwinds, labour code impacts — rattled short-term investors. But the underlying business is structurally intact and growing. This is the kind of entry point long-term investors look back on and smile.

Youtube Link:

Section II

Business Model & Operations

The company operates in four core areas: Electrification (switchgear, distribution boards, smart power), Motion (motors, drives, generators), Process Automation (instrumentation, control systems for oil, gas, pharma), and Robotics & Discrete Automation (industrial robots, machine vision). Think of it this way — from the moment electricity leaves a power plant to the moment it drives a manufacturing robot, this company is involved somewhere in that journey.

Their customers span 23 market segments. Data centres are booming. Rail electrification is accelerating. Grid modernisation is a national priority. Renewables need inverters and smart power management. All of these tailwinds are pointed in the same direction. Management named infrastructure, rail, grid modernisation, and renewables as the four key growth engines heading into 2026. Those aren’t buzzwords — they’re backed by the order book.

One significant development: shareholders approved the sale of the Robotics Business to a wholly-owned subsidiary in February 2026. This is a strategic restructuring, not a distress sale. It allows the parent segment to be better focused and potentially unlocks shareholder value through a cleaner, more focused entity. The core four segments — electrification and motion being the heavyweights — remain firmly in place.

The company has been in India since 1949 and celebrated 75 years of local manufacturing in 2025. That isn’t just a PR milestone — it means deeply embedded customer relationships, established supply chains, and hard-to-replicate manufacturing know-how spread across multiple plants.

Section III

Historical Financial Review

Let’s talk numbers that actually mean something. Revenue has grown from ₹8,568 crore in CY2022 to ₹13,203 crore in CY2025 — a three-year compound annual growth rate of roughly 15.5%. That’s not incremental; that’s a business that’s fundamentally re-rated its earnings power.

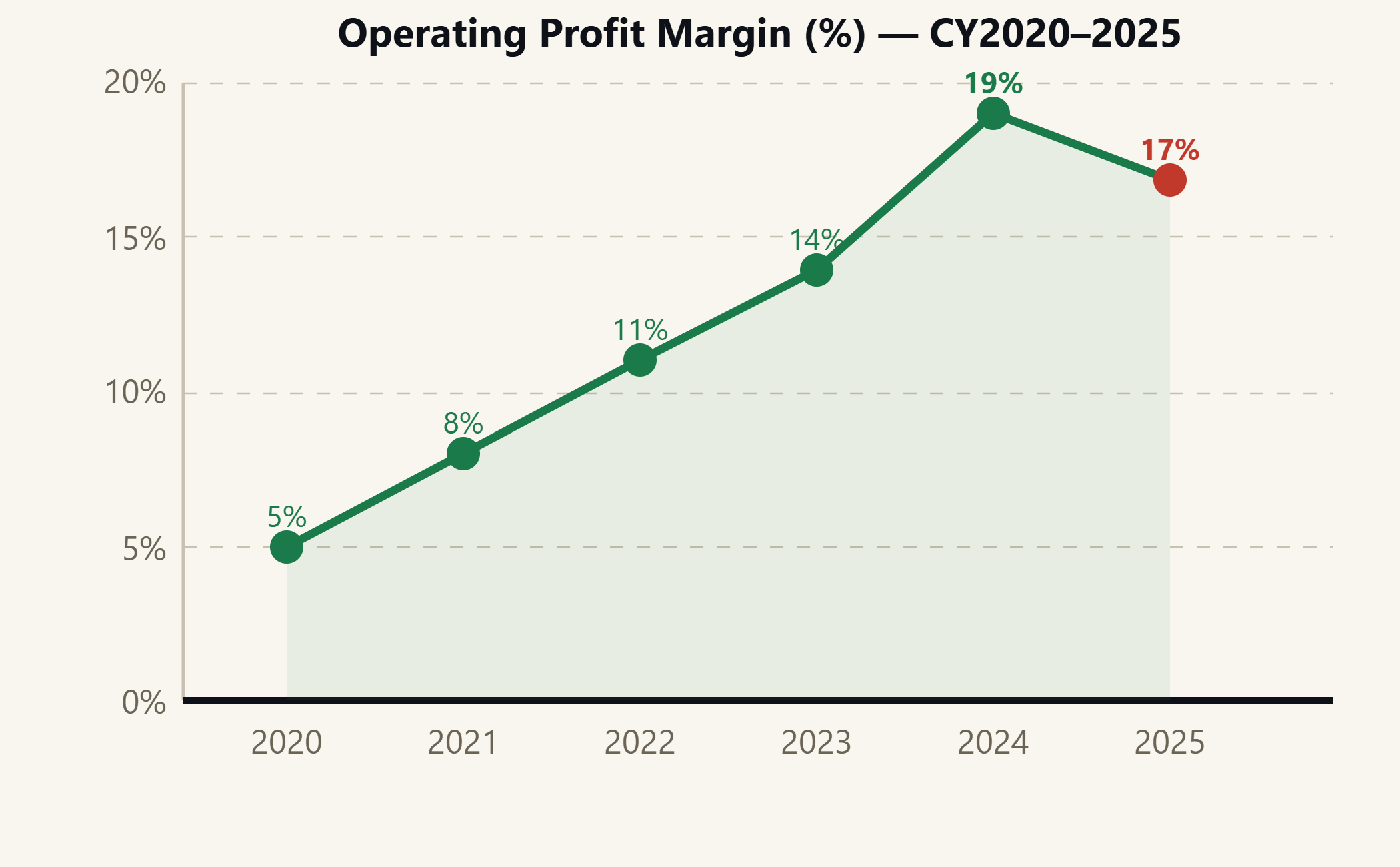

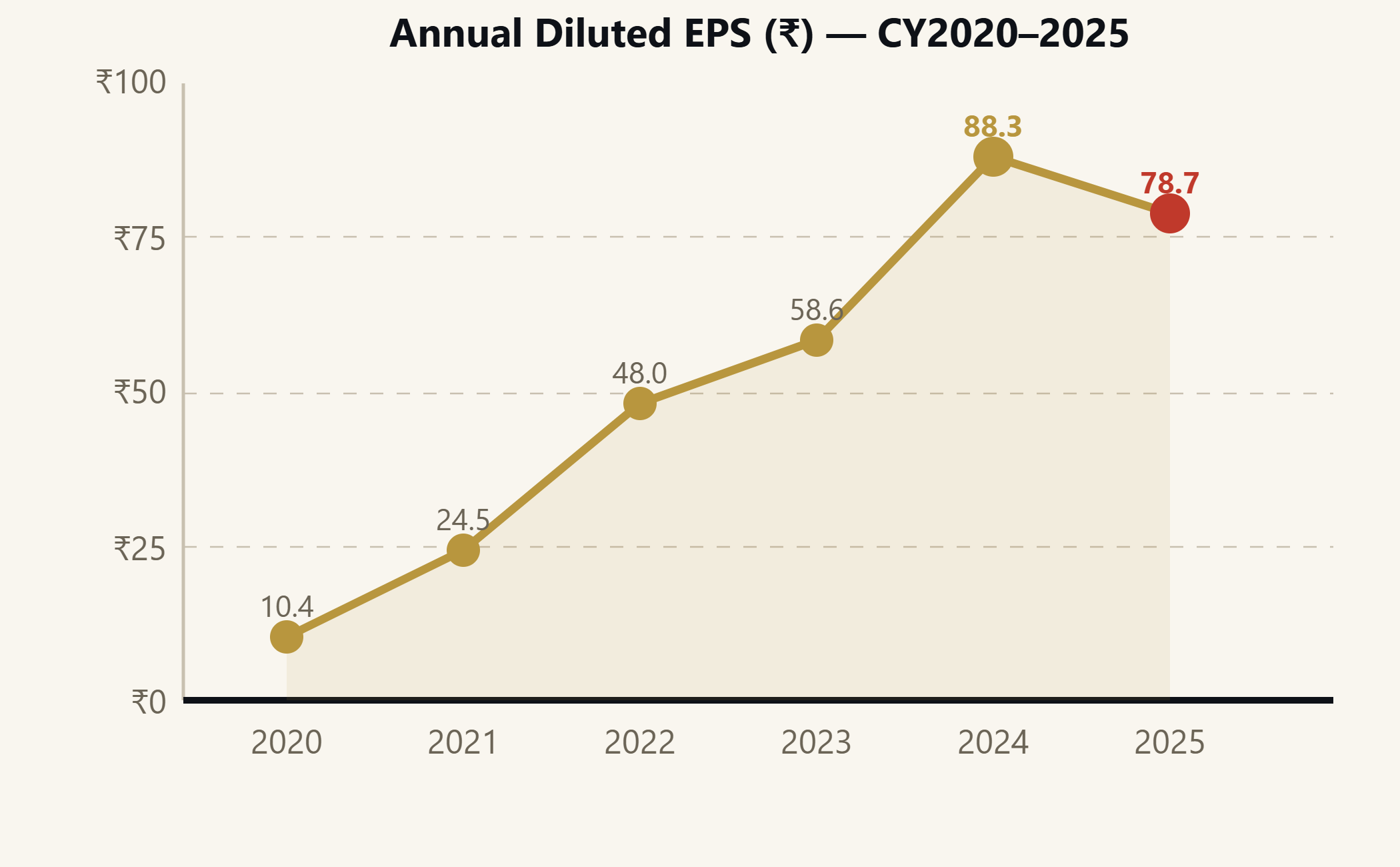

Even more impressive is the profitability transformation. Operating margins were in the 11% range in CY2022. By CY2024, they had expanded to 19%. Yes, CY2025 saw a step-down to approximately 17% due to material costs and forex pressure. But here’s the thing — the underlying structural margin improvement from the low single-digits of five years ago is very much real. The company’s profit CAGR over five years stands at an eye-watering 40%+.

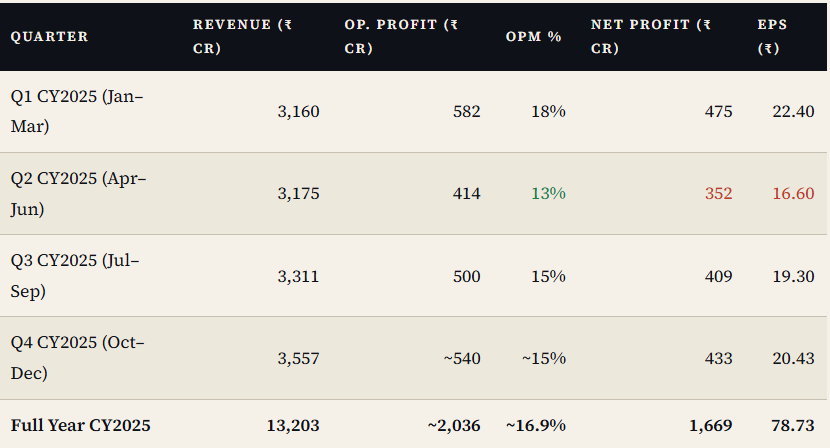

CY2025 Quarterly Snapshot

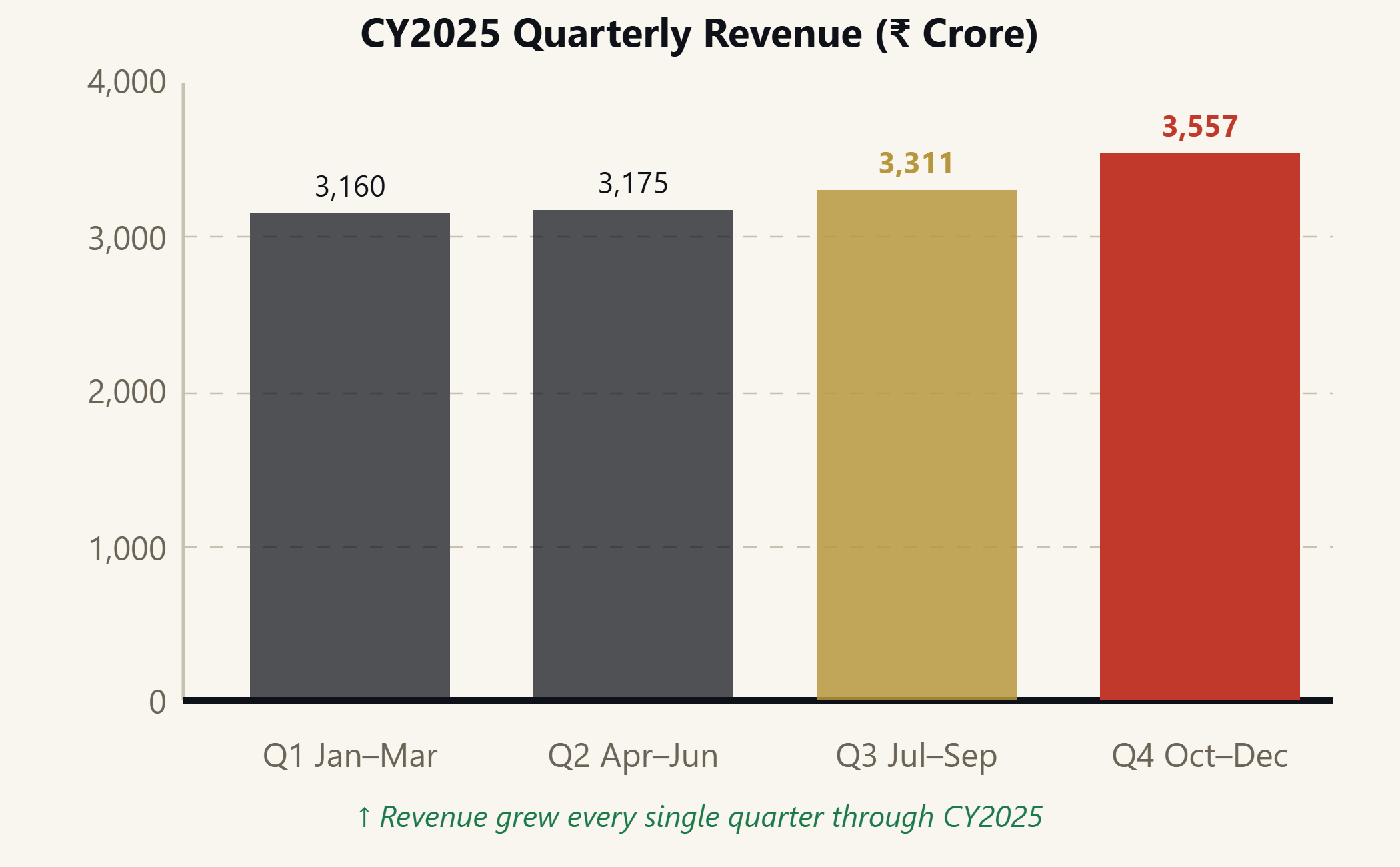

The Q2 dip was the headline-grabber that shook confidence. Operating margins dropped to 13% as material costs bit harder and forex-linked imported content (under QCO-related rules) weighed on profitability. But the recovery trend from Q3 and Q4 — both showing improved execution and volume — is exactly what was needed. Revenue grew every single quarter. The dip was in profitability, not demand. That’s an important distinction.

The TTM EPS works out to approximately ₹83 when you look at the trailing four quarters including Q3 FY2026 data. At ₹5,900, you’re paying about 71 times trailing earnings. Rich? Absolutely. Unjustified? Not for a business with this kind of growth runway, balance sheet strength, and order visibility.

Section IV

Growth Drivers & Outlook

India’s energy transition isn’t optional — it’s a policy mandate, a climate commitment, and an economic necessity all rolled into one. This company sits squarely at the intersection of every major theme: data centre buildout, renewable energy grid integration, industrial automation, and infrastructure modernisation.

Management guided for double-digit revenue growth and target PAT margins of 12–15% going into 2026. Those margins might look lower than the CY2024 peak of 20%+ PBT, but the absolute profit number keeps growing because revenue is scaling. Operating leverage will kick back in as the high-cost import pressure (partly driven by QCO compliance) stabilises.

The export business is also gaining traction. Q4 specifically saw strong export revenues in the Electrification segment, particularly in Distribution Solutions and Smart Power. That adds a new dimension — the India entity isn’t just a domestic play anymore. It’s becoming a regional manufacturing hub for the parent.

Long-term, here’s the math. If the company delivers 12–15% revenue growth for the next five years and maintains PAT margins in the 12–14% range, EPS could reasonably reach ₹150–175 by CY2030. At even a modest 45–50x PE (justified for a quality compounder), that points to a stock price of ₹7,000–9,000. At current prices, that’s a solid 2–2.5x over five years — or roughly 15–20% per year compounded.

Section V

Risks to the Thesis

✦ BULL CASE LEVERS

India–Europe FTA could meaningfully boost exports from Indian plants to European customers

Data centre capex cycle is in early innings; power management demand could outpace forecasts

Margin recovery as QCO-related import costs stabilise and domestic alternatives scale up

Parent ABB Ltd continues to invest in India as a global manufacturing base

₹5,694 crore cash pile — potential for special dividend or strategic M&A

✦ BEAR CASE RISKS

Sustained rupee depreciation inflates input costs; margins stay under pressure longer than expected

Private capex cycle disappoints — government infrastructure spending can’t carry growth alone

Valuation at 68–71x TTM PE leaves zero margin for error; any earnings miss would be punished

Competition from Siemens India, Schneider Electric, and emerging Chinese players in specific segments

Geopolitical risks: global supply chain disruptions could affect specialised components

Section VI

Valuation & Target Price

Let’s be straight about this: at ~68–71x trailing earnings, this is not a value stock. You are paying for quality, growth, and the optionality that comes with India’s multi-decade industrialisation. The question is whether that premium is justified. We think it is — with caveats.

Here’s how we get to ₹7,200 over 12–18 months. If revenue grows 12–14% through 2026 and margins recover to 14–16% PAT, then FY2026 EPS should land in the ₹90–100 range. Apply a 70–75x PE on normalised earnings of ₹95, and you get ₹6,650–7,125. Round it to ₹7,200 with some re-rating potential as the margin recovery story gets acknowledged by the market. That’s roughly 22% upside from current levels.

For the long-term investor with a 5-year horizon: if EPS compounds at 15% annually from ₹79 today, you’re looking at ~₹159 by CY2030. At 50x PE (which is conservative for this quality), that’s a ₹7,950 stock — representing a 2.3× from today’s price, or about 18% annualised return including dividends (currently yielding ~0.85%).