The Silent Backbone Powering India’s Next Energy Boom

SECTION I: Investment Thesis & Summary

India is building out one of the largest power transmission networks in the world, and this company makes the actual wires that carry the electricity. Every new solar park, wind farm, data centre, and railway electrification project needs conductors and cables. And there’s exactly one company in India — actually in the world — that’s the undisputed #1 manufacturer of aluminium conductors. That’s this one.

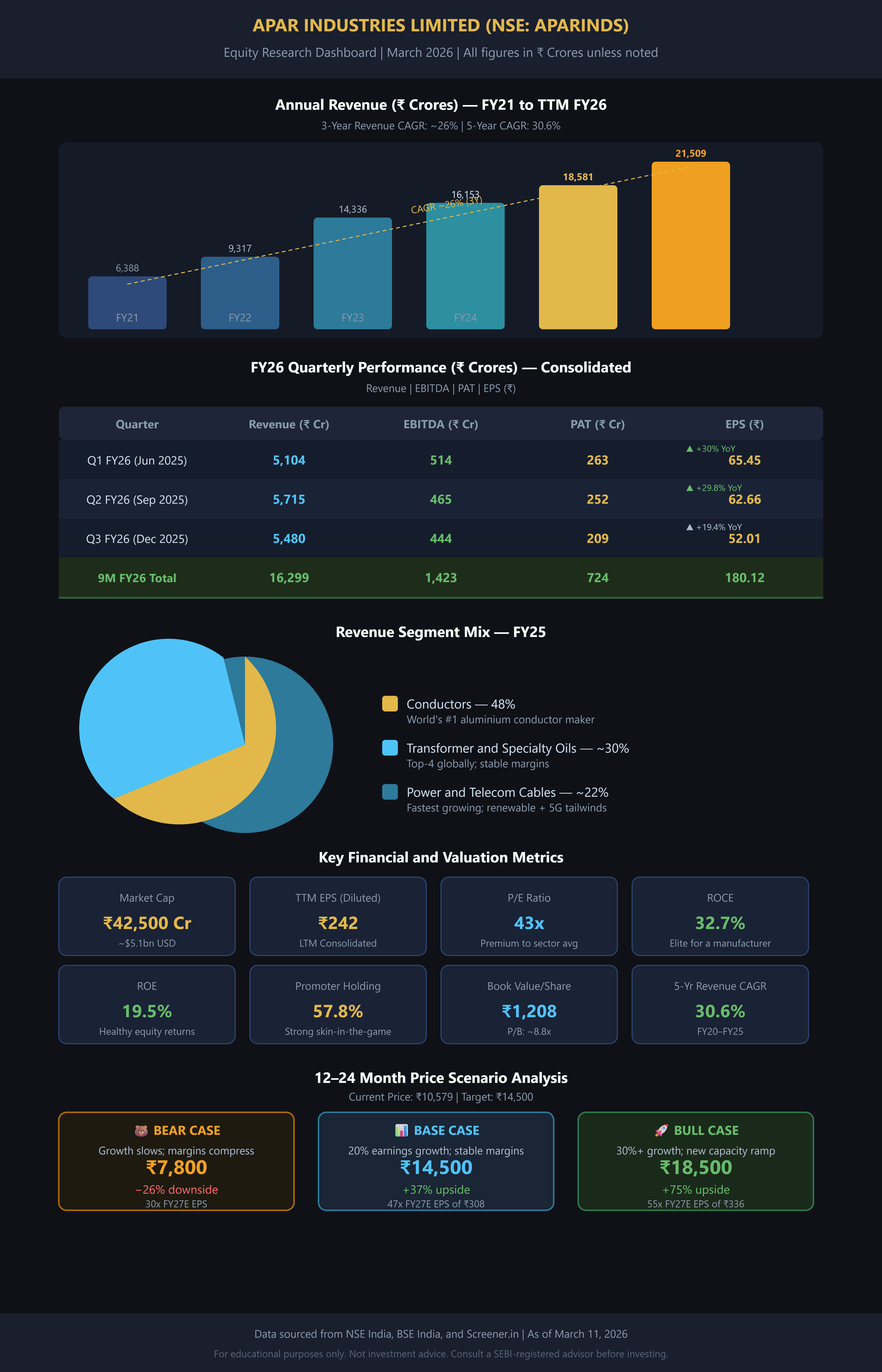

At ₹10,579 per share, the stock isn’t cheap. A P/E of around 41–43x tells you the market already knows this is a quality business. But here’s the thing — the company is growing revenues at roughly 27–30% YoY, margins are holding up, and a massive ₹1,300 crore capacity expansion is coming online just as demand accelerates. The stock already delivered 340%+ returns over 3 years. The question isn’t whether it’s been a great stock. The question is whether it stays great. We think the answer is yes — with the right expectations on valuation.

Our target: ₹14,500 over 18–24 months. That’s roughly a 37% upside from current levels, driven by earnings growth, operating leverage from new capacity, and continued sectoral tailwinds.

Youtube Link:

SECTION II: Business Model & Operations

Let’s be straightforward about what this business actually does.

Three things. That’s it.

One — Conductors (48% of revenue). Think of these as the highways for electricity. The overhead wires strung between transmission towers that carry high-voltage power across hundreds of kilometres. This company is the world’s largest maker of these — particularly the aluminium-based variety. And it’s not just making the old standard type. It’s moved into high-efficiency, high-temperature conductors (called ACSR, HTLS, and ACCC types) that let utilities carry more power over the same infrastructure without rebuilding towers. That’s a premium product, and it commands premium margins.

Two — Transformer & Specialty Oils (around 30% of revenue). Power transformers need insulating oil inside them to keep them cool and safe. This business is one of the top four transformer oil manufacturers globally. It also makes specialty oils for railways, lubricants for industrial use, and petroleum-based products for pharma and personal care. It’s a quieter, steadier business — doesn’t grab headlines but generates consistent cash.

Three — Power & Telecom Cables (around 22% of revenue). Underground and submarine cables for power distribution networks. Fiber optic cables for telecom. Specialty cables for renewable energy farms (connecting solar panels to inverters, etc.). This is the fastest-growing piece, benefiting from India’s push into 5G, data infrastructure, and green energy.

What’s been happening lately:

The company runs 10 manufacturing plants across India and the UAE, exporting to over 140 countries. In Q1 FY26, the domestic conductor business grew 44% year-on-year — that’s not a typo. India’s power sector capex is accelerating at an unprecedented pace, and this company is right in the thick of it.

It recently entered the telecom EPC space — winning a ₹157 crore contract to build towers and lay fiber for Indian Railways’ Kavach safety system. It’s also expanding its Continuous Transposed Conductor (CTC) capacity, which goes into large power transformers, to 20,490 MT annually. New cable plant capacity at Umbergaon is expected online by June 2026.

Management has committed to a 5-year revenue CAGR target of 20%+ and is on track. The January 2026 corporate presentation showed FY25 revenue at ₹18,581 crores, with a 5-year CAGR of 30.6%. That’s a strong track record to back the ambition.

SECTION III: Historical Financial Review

Let’s talk numbers — but in a way that actually means something.

Revenue growth tells the story best. Going from ₹14,336 crores in FY23 to ₹16,153 crores in FY24 to ₹18,581 crores in FY25, that’s a 3-year revenue CAGR of approximately 26%. The trailing twelve months (TTM) revenue is now touching ₹21,509 crores. The business has literally doubled in size in 3 years.

FY26 Quarterly Scorecard — Quarter by Quarter:

Q1 FY26 (April–June 2025): Revenue ₹5,104 crores, up 27.3% YoY. PAT ₹263 crores, up 30% YoY. EBITDA ₹514 crores at 9.8% margin. EPS for the quarter: ₹65.45. Conductor segment alone grew 44% YoY — extraordinary.

Q2 FY26 (July–September 2025): Revenue ₹5,715 crores, up 23.1% YoY. PAT ₹252 crores, up 29.8% YoY. EBITDA margin: 8.7%. EPS: ₹62.66. The half-year PAT was a record ₹515 crores. Cable exports surged 136% in Q1 as US buyers pre-bought ahead of tariff uncertainty — this partially pulled forward demand, creating some noise in Q2.

Q3 FY26 (October–December 2025): Revenue ₹5,480 crores, up 16.2% YoY. PAT ₹209 crores, up 19.4% YoY. EBITDA ₹444 crores. Margins softened slightly to 8.1–8.8% as export headwinds (US tariff uncertainty impacted international cable demand) dented the top line. 9-month EBITDA per tonne: ₹42,311 — significantly above the management guidance of ₹30,000+.

Key ratios as of early March 2026:

TTM EPS (Diluted): ~₹242–247 (LTM consolidated, combining Q4FY25 + Q1+Q2+Q3 FY26 EPS of ₹62.23 + ₹65.45 + ₹62.66 + ₹52.01 = ~₹242)

P/E: ~43x on LTM earnings

ROCE: 32.7% — exceptional for a capital-intensive manufacturing business

ROE: 19.5%

Dividend Yield: 0.46–0.53%

Book Value per Share: ₹1,208

P/B: ~8.8x (the market is clearly pricing in future growth, not current book)

What these numbers tell us: The company is genuinely profitable and highly efficient — a 32.7% ROCE means for every ₹100 of capital deployed, it’s generating ₹32.7 in operating returns. That’s elite territory for any Indian manufacturer. The PAT margin is thinner than it looks (around 4–5%) because the business has high material pass-through costs — aluminium and copper prices flow through both the top line and cost line. The real metric to track is EBITDA per tonne (conductors) and absolute EBITDA growth, both of which are healthy.

Operating cash flow in FY25 was approximately ₹1,300 crores (₹13 billion), giving an operating cash flow per share of roughly ₹325. The business does generate cash, which is key given its working capital intensity.

SECTION IV: Growth Drivers & What Could Go Wrong

Why the growth story is real:

India’s power sector capital expenditure is in a multi-year upcycle. The government’s push to add transmission capacity, connect renewable energy to the grid, and electrify railways creates a long-duration demand pipeline. Every new solar park in Rajasthan needs conductors to connect to the grid. Every metro expansion needs cables. Every data centre needs power infrastructure.

The company’s product mix is also shifting toward premium, high-margin items. High-temperature low-sag (HTLS) conductors, for instance, cost significantly more per tonne but help utilities reconductor existing transmission lines without rebuilding the towers — a cost-effective solution that’s being adopted widely.

Export markets (140+ countries) provide diversification. Even with the US tariff uncertainty that hurt cable exports in Q3, the company has the global reach to redirect product flows.

The ₹1,300 crore CapEx being deployed across conductor and cable capacity will begin generating incremental revenue from FY26–FY27, providing an earnings upgrade cycle.

Now let’s be honest about what could go wrong:

The stock trades at 41–43x earnings. That’s not bargain territory. If growth slows — because of commodity price shocks, a global recession cutting infrastructure budgets, or execution issues at new plants — the stock could re-rate sharply downward.

The company carries meaningful working capital. Revenue growth at 25%+ means receivables and inventory both grow. If payment cycles from government utilities stretch (which historically they do), the balance sheet can get stressed. The cost of borrowing remains elevated, with interest costs running around ₹400–443 crores annually.

Export business, particularly cables, is sensitive to US policy. The pre-buying ahead of tariffs boosted Q1 FY26 but created a hangover in Q3. Management is watching this carefully.

Commodity prices — aluminium in particular — create margin volatility. The company hedges, but imperfectly. A sharp aluminium spike compresses margins even if revenue stays flat.

The CEO of the Cable Solutions division resigned in December 2025. It’s a single event, but leadership continuity is worth watching.

SECTION V: Valuation & Target Price

Here’s how we get to ₹14,500.

The company is on track to report 9M FY26 PAT of approximately ₹724 crores (Q1+Q2+Q3 = ₹263+₹252+₹209). A reasonable Q4 FY26 estimate, assuming seasonal strength that typically shows up in the March quarter, would be ₹280–300 crores, taking full-year FY26 PAT to approximately ₹1,000–1,020 crores.

FY27 PAT, assuming 20% growth (conservative given sectoral tailwinds), would be ~₹1,200–1,250 crores. Diluted shares outstanding: ~4.02 crore shares. FY27E EPS: ~₹298–311.

At a fair P/E of 45–47x (reasonable for a dominant manufacturer in a high-growth sector with a 32% ROCE), target price = ₹298 × 47 ≈ ₹14,006 to ₹14,617. We set the midpoint target at ₹14,500.

For a 10-year horizon, assuming the company compounds earnings at 18% annually (below its 5-year CAGR of 30%+), EPS reaches roughly ₹1,250+ by FY35. At 35x (a more mature-company multiple), that implies a stock price of ₹44,000+. The long-term compounding story is intact.

SECTION VI: The Bottom Line

This is a genuinely world-class Indian manufacturer at the heart of India’s energy transition. The business model is sound, the numbers are real, and the runway is long. The stock has already been a multi-bagger — and yet, the infrastructure cycle it’s riding is arguably just entering its high-growth phase.

The risk? Valuation. At ₹10,579, you’re paying for a lot of good news already. This isn’t the ₹4,000 stock of two years ago. For investors with a 3–5 year horizon who understand manufacturing cycles and can tolerate volatility, this remains a compelling buy. For short-term traders looking for a quick 10%, the risk-reward is less attractive.

The right move: invest with a 3–5 year minimum horizon. The sector tailwind is structural. The company is the dominant player. The capacity expansion is on track. And India’s power grid is nowhere near built out.

This is not a trade. This is an ownership story.