The Only Shipyard That Builds Both Destroyers & Submarines

Section I

Investment Thesis & Summary

Here’s the situation in plain English. This company sits in the most protected corner of Indian defence manufacturing — naval warships and submarines. The government doesn’t just favour it; the government is its customer, its promoter (holding 81.2%), and its biggest fan. You can’t get more captive than that.

The stock has pulled back over 37% from its all-time high of ₹3,778 hit in May 2025, and now trades around ₹2,380. The fall has brought the P/E down from peak levels, but at ~42x trailing earnings, it’s still no screaming bargain. Here’s the thing — for a company growing profits at over 38% CAGR over five years with zero debt and rising margins, a 42x multiple is defensible.

This isn’t a momentum trade. The fundamental story — India’s ₹10-lakh-crore naval expansion, a growing indigenous shipbuilding mandate, and fresh submarine programmes — hasn’t changed one bit. The stock repriced; the business didn’t. That’s what makes this a Hold / Accumulate on dips call, not a full-throttle Buy at current levels.

One-line thesis: India is spending heavily on maritime security, this company is the only one capable of building the most sophisticated vessels the Navy needs — and the pipeline of work runs well into the next decade.

Youtube Link:

Section II

Business Model & How the Money Works

The business is deceptively simple: build and repair very complex things for one very important client — the Indian Navy. Revenue flows from two main streams.

Shipbuilding is the bigger segment. Think Nilgiri-class stealth frigates (Project P17A), P15B guided-missile destroyers, offshore patrol vessels, and various coast guard platforms. These are multi-year, multi-thousand-crore contracts with milestone-based revenue recognition — meaning revenue gets booked when specific stages of a ship’s construction are certified complete. That’s why you’ll see quarterly revenue jump around a lot.

Submarines & Heavy Engineering is the crown jewel. Building the Kalvari-class submarines under Project P75 is not something any other Indian shipyard can do. This segment also handles refits, repairs, and life-certifications for the Navy’s existing submarine fleet — high-margin, recurring work.

On top of these, there’s commercial shipbuilding (offshore platforms for ONGC, cargo vessels, patrol boats) and a growing focus on AI-enabled marine systems. The commercial side is small but adds diversification.

What happened recently? The company commissioned three frontline combatants — INS Nilgiri, INS Surat, and INS Vaghsheer — all in one ceremony in January 2025. That’s a historic moment. A third Nilgiri-class frigate, INS Taragiri, was delivered in November 2025. A Teaming Agreement with Swan Defence for Landing Platform Docks (LPDs) was signed — potentially a massive new contract category. Meanwhile, a partnership with Naval Group France for evolved Scorpène submarines signals the next generation pipeline.

Section III

Historical Financials — The Numbers Behind the Story

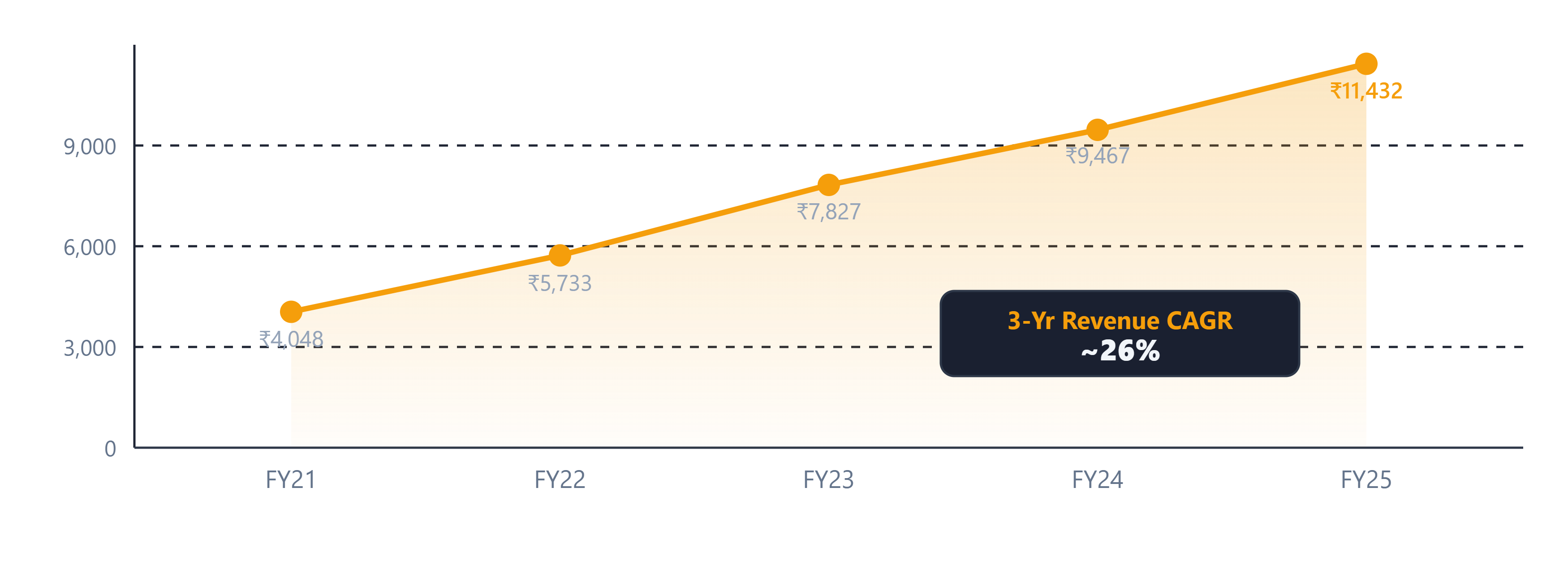

Let’s start with the headline. Between FY22 and FY25, revenue grew at a 3-year CAGR of ~26% — from ₹5,733 crore to ₹11,432 crore. Profit over the same period? A staggering ~58% CAGR. That’s not just a growing company; that’s a company whose profitability is accelerating much faster than its revenue, which tells you margin expansion is real.

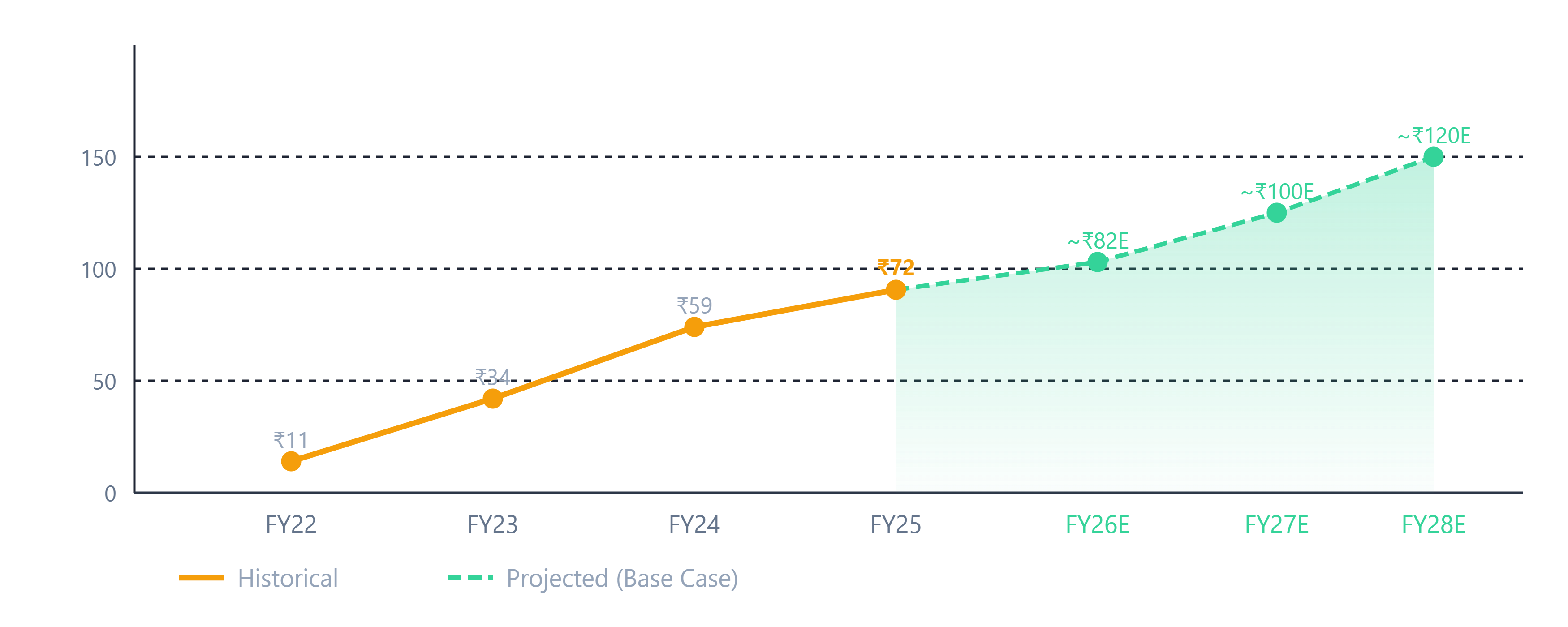

The LTM (last 12 months) diluted EPS stands at approximately ₹57–58 per share, built on 9-month consolidated PAT of ₹2,081 crore for FY26 and a quarterly run rate that continues to improve. Operating cash generation is strong — the company is essentially debt-free and sits on a large cash and treasury portfolio, the interest from which adds ₹1,100+ crore annually to “Other Income.”

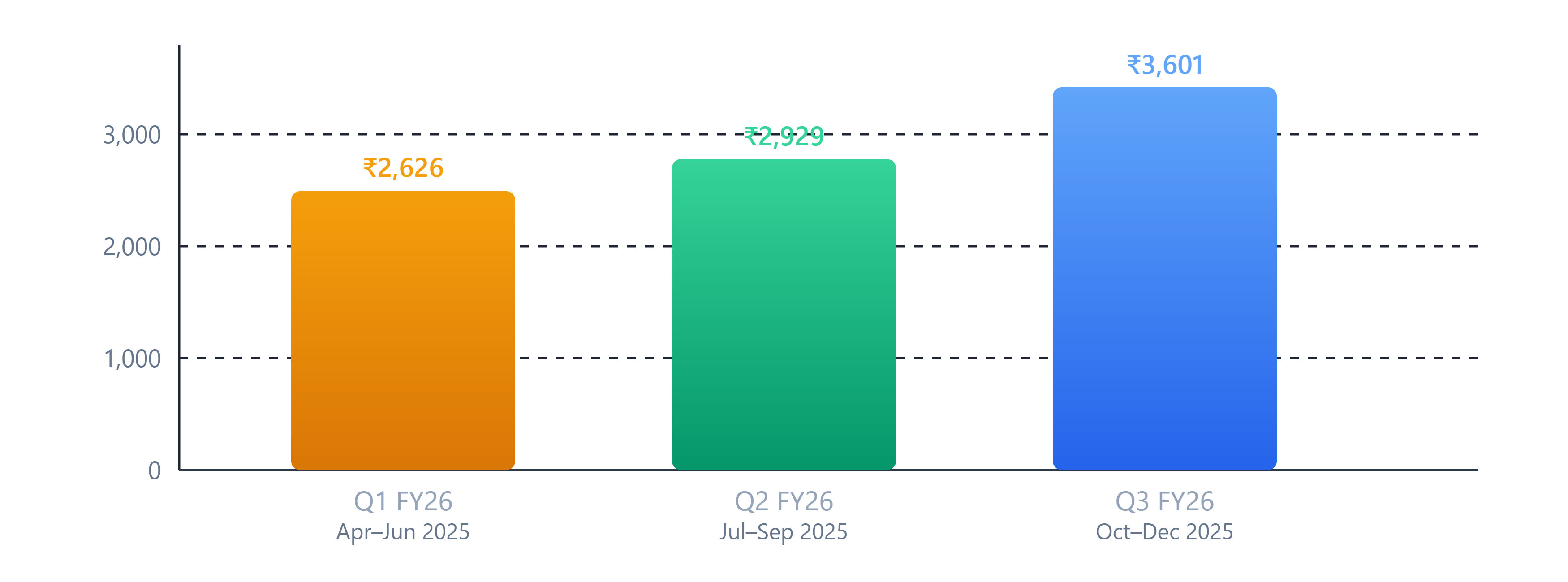

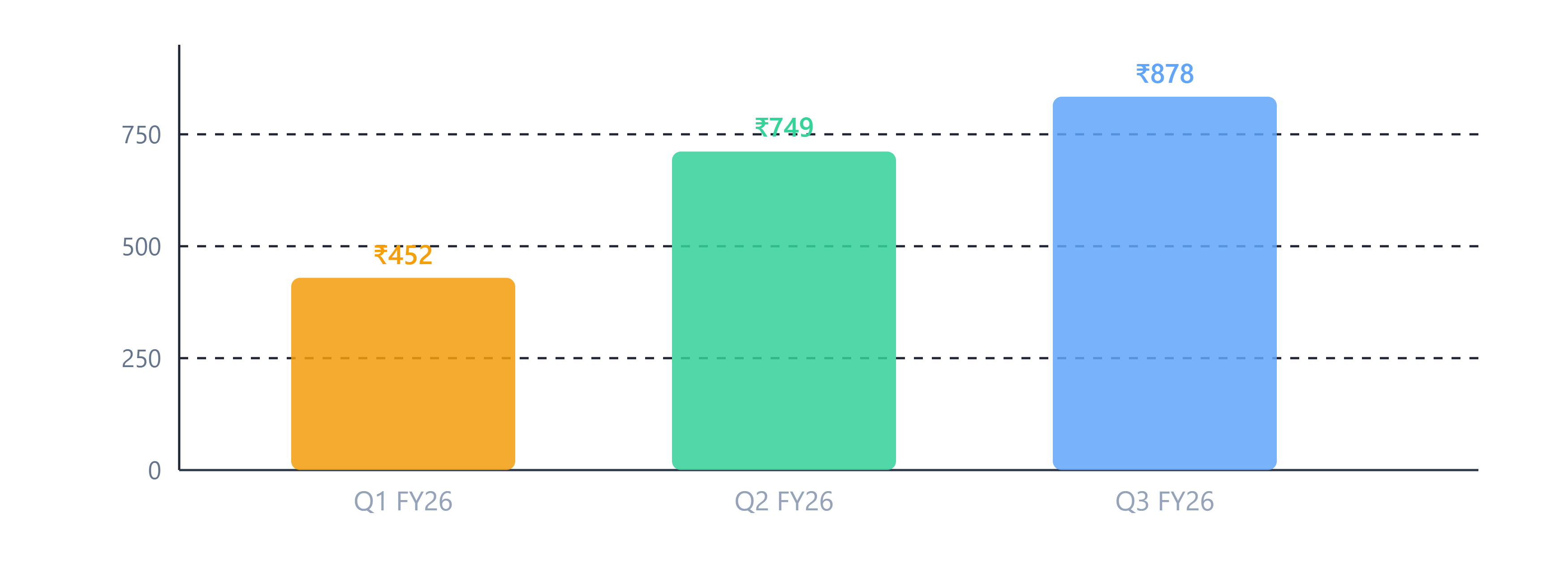

Now the quarterly picture for FY26:

A couple of things stand out. First, Q1 FY26 PAT was relatively low at ₹452 crore because operating margins dipped — this is normal in shipbuilding. Revenue is milestone-based, so in quarters where fewer milestones are certified, margins compress. By Q3, margins rebounded to 24% EBITDA, and profit hit ₹878 crore — the best quarter ever. Second, the nine-month FY26 PAT of ₹2,081 crore already surpasses the entire FY25 first-half performance. The full year is shaping up to be another record.

The operating margin journey is just as impressive. From a thin 6% in FY21, margins expanded to 8% in FY22, 10% in FY23, 15% in FY24, and 18% in FY25. That's not a lucky year — that's a structural shift driven by higher-value vessel mix and better cost management. The TTM EBITDA margin is 16%, tracking consistent with that trend.

Section IV

Growth Potential — Where the Next 5–10 Years Come From

The defence shipbuilding story in India is just getting started. The Navy has laid out a long-term plan to expand its fleet significantly — more submarines, more destroyers, more frigates. The government’s “Make in India” push in defence means that as much work as possible must be awarded to domestic shipyards. And there is exactly one shipyard in India that builds destroyers and submarines. That’s a moat you can’t manufacture overnight.

Three growth engines stand out:

1. Next-generation submarines. The P75I programme — six advanced submarines with Air Independent Propulsion (AIP) — is expected to be one of the largest defence contracts India has ever signed. The company is a frontrunner for this. If awarded, this single contract could add tens of thousands of crores to the order book.

2. Landing Platform Docks (LPDs). The Defence Acquisition Council has approved acquisition of LPDs — large naval vessels for amphibious operations. The Teaming Agreement signed with Swan Defence positions this yard well to capture this order. These projects run into thousands of crores each.

3. Broader government push for maritime infrastructure. Budget 2026 announced a ₹10,000 crore plan to boost domestic container manufacturing. Combined with the Union Cabinet’s ₹69,725 crore package for the broader shipbuilding sector, the demand environment for Indian shipyards has never been better.

For the 5–15 year investment horizon, if revenue continues growing at even 15–18% annually (well below the historical pace), earnings could compound meaningfully. At a modest 25x P/E on FY29 projected EPS of ₹120–130, the stock could reasonably be worth ₹3,000–3,250 within 3 years. The longer the holding period, the more compelling the return profile — especially with dividends being consistently paid (₹13.50/share declared so far in FY26 alone).

Section V

Balance Sheet & Financial Health — The Clean Part

Zero long-term debt. Full stop. For a company executing multi-year projects worth thousands of crores each, this is exceptional. The balance sheet has ₹7,939 crore in shareholder equity and no meaningful borrowings. Debtor days have actually improved from 50.7 days to 34.1 days — the Navy is paying faster, which is a great sign.

Return on Capital Employed sits at 43.2% and Return on Equity at 34% — these are not capital-goods-company numbers; these are software-company-level returns on a shipyard. That tells you the business doesn’t need to continuously eat up capital to grow. The cash it generates stays in the business (or comes back to shareholders as dividends).

Let’s be honest about one thing: the “Other Income” line of ₹1,190 crore in FY25 is substantial — roughly 40% of pre-tax profits. This comes from the company’s massive cash pool (customer advances held as deposits). It’s real income, but it’s passive, not operational. Strip it out, and the core shipbuilding business is still profitable and growing — just important to keep in mind when evaluating earnings quality.

Section VI

Risks — Let’s Be Honest

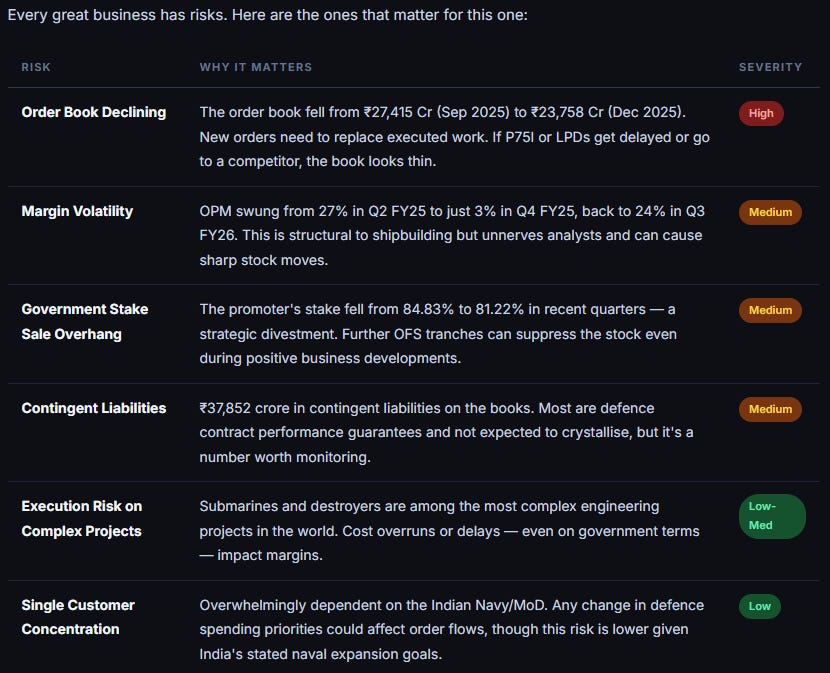

Every great business has risks. Here are the ones that matter for this one:

Section VII

Valuation & Target Price

At ~₹2,380, the stock trades at approximately 42x trailing twelve-month earnings. That sounds expensive for a defence PSU — and it was even more stretched at ₹3,778. But context matters: the five-year profit CAGR is 38%, ROCE is 43%, the company is debt-free, and the business has structural tailwinds from India’s naval build-up that aren’t going away.

Peer comparison puts this in perspective. Garden Reach Shipbuilders trades at comparable multiples with lower margins. Cochin Shipyard is cheaper but with a smaller strategic moat. This company’s premium is justified by its unique capability set and captive government demand.

On a forward basis, if FY26 full-year EPS comes in around ₹82–85 (tracking to ₹2,081 crore PAT in 9 months, with a strong Q4 likely), the stock at ₹2,380 is at ~28–29x forward earnings. That’s a more reasonable entry point than peak valuations.

Target Price Scenarios — Based on FY27E EPS of ₹100

Section VIII

The Bottom Line

This company occupies a unique position in India’s defence ecosystem. It builds the most sophisticated naval platforms in the country, has a government customer that’s committed to expanding its naval fleet, holds Navratna status (the highest autonomy a government enterprise can have), and has delivered 38% PAT CAGR over five years with zero debt.

The stock has corrected meaningfully from its peaks. The business hasn’t. Q3 FY26 was the company’s best quarter on record by profitability. The pipeline — P75I submarines, LPDs, continued frigate deliveries — is real and multi-year. The dividend keeps coming.

Is it the cheapest stock in the market? No. Does it deserve a premium? Absolutely. At ₹2,380 with a 30% upside to a reasonable 12-month target of ₹3,100 and an even stronger 5–10 year story, the call is: Hold current positions, accumulate on dips below ₹2,200. For fresh investors with a 3–5 year horizon, this is a quality compounder in one of India’s most important strategic sectors.