The Invisible Infrastructure Powering India’s Next Decade of Growth

SECTION I: Investment Thesis & Summary

India is in the middle of a decade-long infrastructure and housing boom, and every building, every factory, every solar farm, every EV charger needs one thing before anything else: wire.

This company makes that wire. And it does it better than almost anyone in India.

The stock is down roughly 19% from its 52-week high of ₹1,028, sitting at ₹832 as of late March 2026. The market is penalising it for margin compression driven by rising copper prices. That’s real — but it’s temporary. The revenue engine is roaring, the balance sheet is debt-free, and the company is sitting on a pile of investable cash that keeps compounding quietly.

At a P/E of roughly 17–18x on a trailing basis, this stock trades at nearly a 50% discount to its sector peers. Simply put — the price hasn’t caught up with the business.

Youtube Link:

SECTION II: Business Model & Operations

The company makes electrical cables, communication cables, copper rods, and a growing range of Fast Moving Electrical Goods (FMEG) — switches, fans, LED lights, water heaters, switchgear. Think of it as India’s backbone-in-a-box for electrification.

About 80% of revenue comes from electrical cables. Wires for homes, commercial buildings, solar installations, automobile harnesses — if electricity moves through it, chances are they make it.

The remaining 20% comes from communication cables (fiber, CCTV, LAN, telephone), copper rods (sold to other cable manufacturers — essentially trading on metal), and the newer FMEG vertical which is still small but growing.

They sell through over 5,000 channel partners, 28 depots, and more than 50,000 retailers across India. That distribution network is a real competitive moat. It took decades to build and can’t be replicated overnight.

A few things happening on the ground right now:

Electrical wire volumes grew 28% year-on-year in the December 2025 quarter — that’s remarkable, and it’s demand-driven, not just pricing.

Optic Fiber Cables grew 34% in the same quarter. The government’s BharatNet rollout and enterprise fiber builds are structurally driving this.

FMEG remains the wild card — it’s a crowded space with Havells, Polycab, and others, but the brand recall and distribution scale gives this company a real shot at meaningful market share over 5–7 years.

Energy efficiency regulation changes (effective January 2026) caused temporary trade destocking in FMEG ahead of the quarter. That’s a one-time headwind, not a structural problem.

The company holds approximately 25% market share in the organised electrical wires segment in India. That’s a leadership position, and it’s held firm for years.

SECTION III: Historical Financial Review

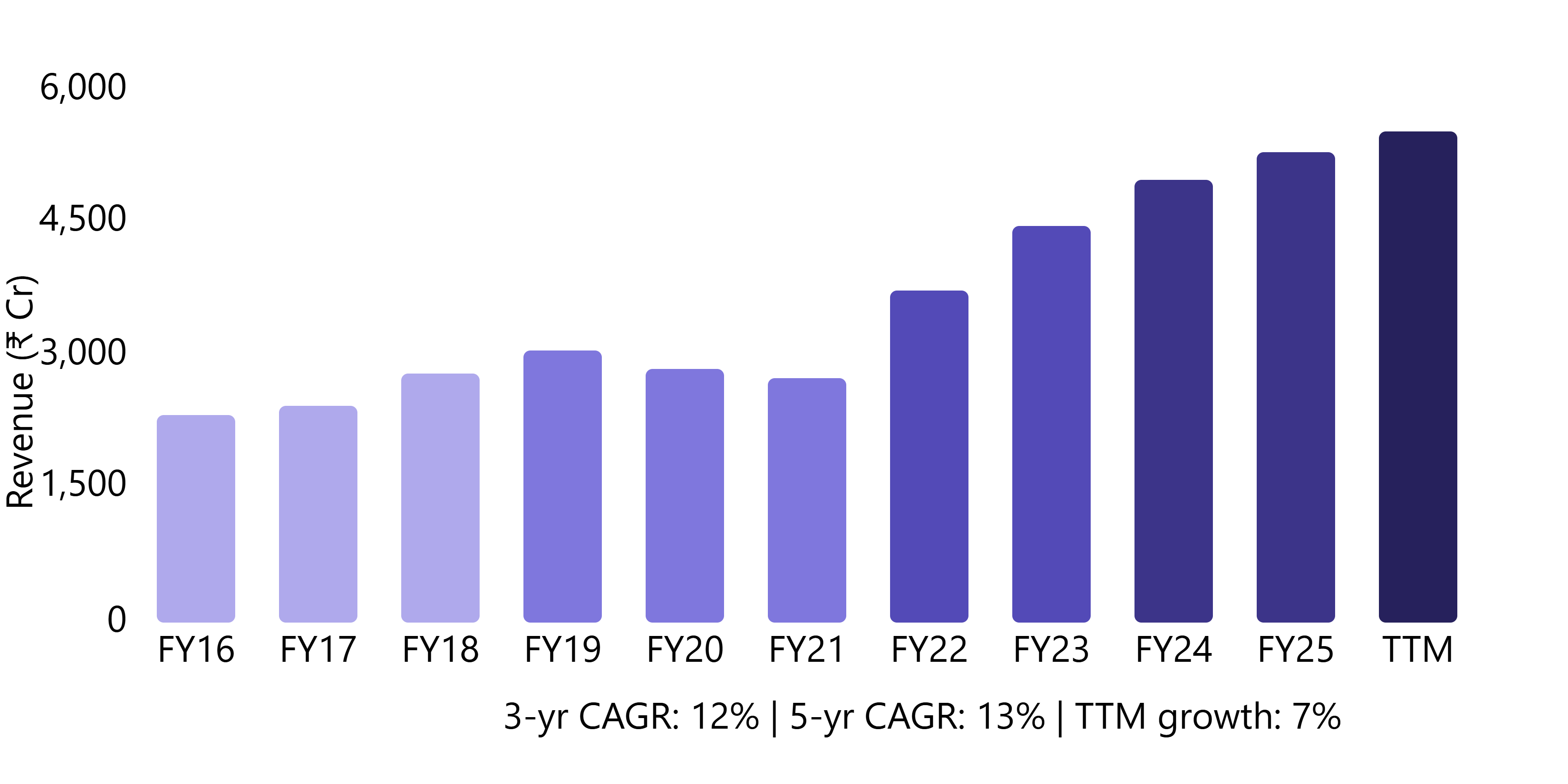

The numbers tell a solid story, with one asterisk.

3-Year Revenue CAGR: ~12% Revenue has grown from roughly ₹4,481 Cr in FY23 to ₹5,319 Cr in FY25, and the trailing twelve months suggest over ₹5,540–5,600 Cr. Consistent, visible, demand-driven growth.

LTM Diluted EPS: ~₹43.4 At the current price of ₹832, that means you’re buying this business at roughly 19x trailing earnings — while sector peers trade closer to 38–40x. Either the entire sector is overvalued, or this company is being undervalued. The answer is somewhere in between, but the discount is stark.

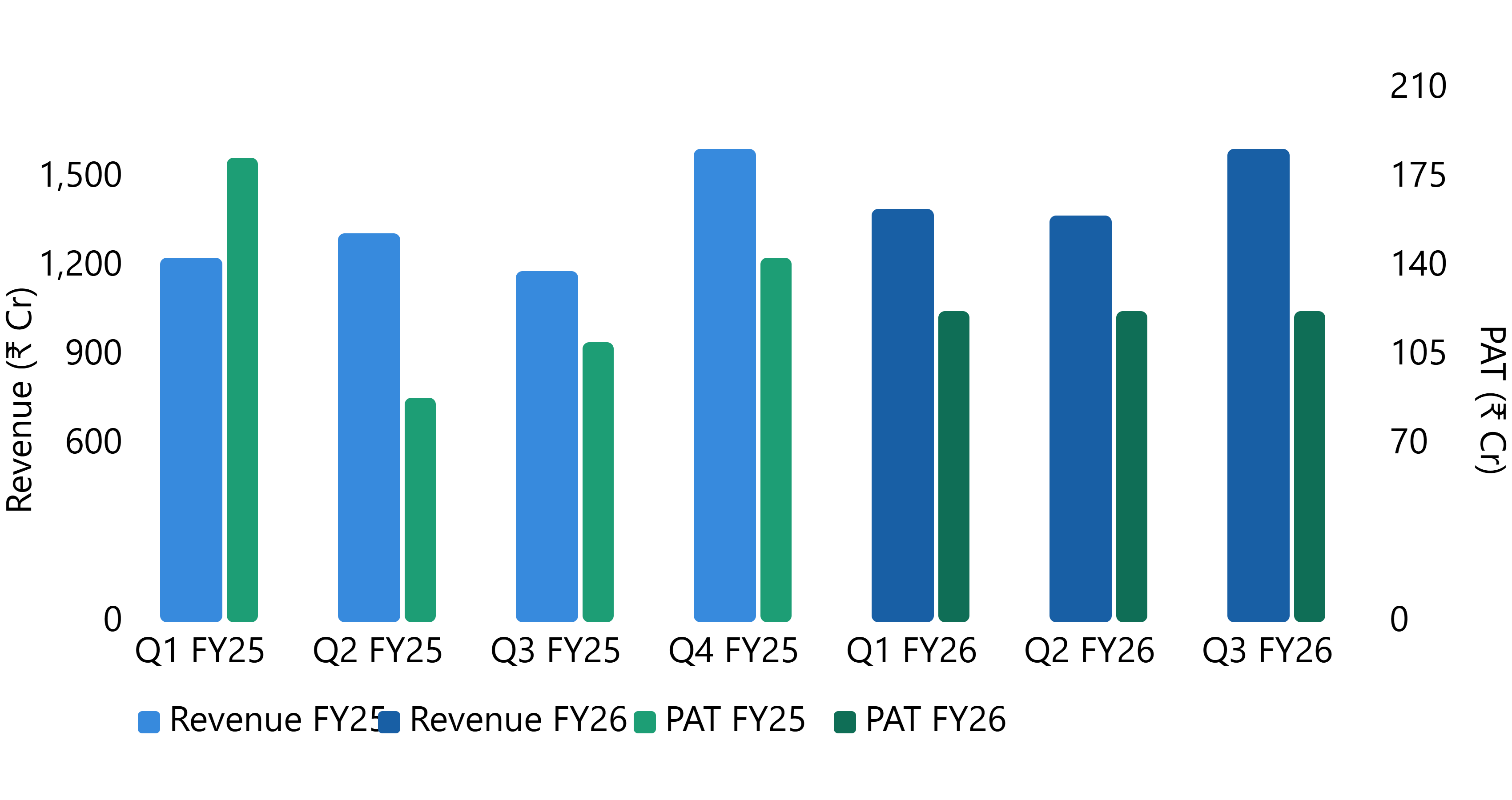

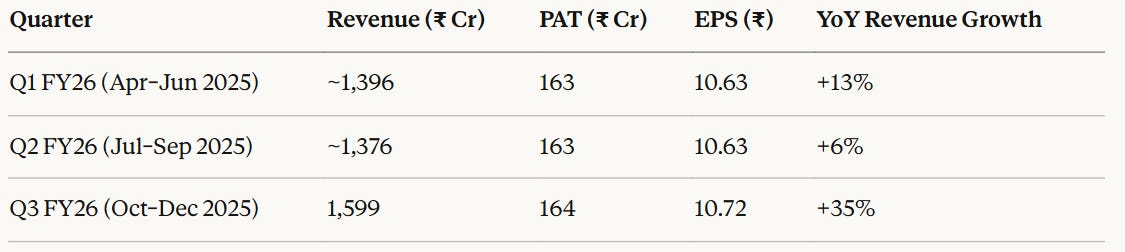

Quarterly Scorecard — FY26 So Far:

Look at Q3. Revenue jumped 35% year-on-year. That is the highest quarterly revenue in the company’s recent history — ₹1,599 crore in a single quarter. That’s the electrical wire volume surge coming through.

The asterisk? Margins are under pressure. Operating margins slipped to ~9.9% in Q3 FY26 from 11.7% a year ago. Copper prices have risen sharply, and the company hasn’t been able to fully pass that through to customers yet — partly competitive dynamics, partly channel caution.

PAT grew only ~11% year-on-year even as revenue grew 35%. The operating leverage that should have kicked in didn’t, because raw material costs ate the upside. This is the key risk to watch.

SECTION IV: Balance Sheet & Capital Efficiency

This is where the company genuinely shines.

Debt-free. Zero long-term debt. That’s not common in a capital-intensive manufacturing business.

Other income of ₹326 Cr (LTM) — the company has built up a substantial treasury investment corpus over years of strong cash generation. That other income line cushions reported profits and funds future capex without needing to raise debt.

ROCE: ~17.7% | ROE: ~13.4% These are decent but not spectacular numbers. The ROE is suppressed by the large cash and investment pile sitting on the balance sheet. Strip that out and the underlying business returns are materially higher.

Working capital has improved significantly — down from 82 days to ~59 days. That’s cash being freed up from the operating cycle, which is exactly the right direction.

Dividend yield: ~1.0% — modest, but the company paid ₹8/share as final dividend for FY25 (400% on face value of ₹2). Consistent dividend payer over the last decade.

SECTION V: Growth Drivers & What to Watch

The Bull Case:

India’s infrastructure supercycle — Roads, railways, metro rail, data centres, renewable energy, smart cities. Every one of these needs cable. The company is positioned right at the intersection of all of them.

Housing boom — Real estate activity is at multi-year highs. Every new home needs wiring, and at 25% market share in organised wires, this company benefits disproportionately.

Solar & EV tailwinds — Speciality cables for solar installations and EV charging infrastructure are growing fast. The company has dedicated product lines here.

Communication cables ramp — After a soft patch due to client-side delays, optic fiber orders are back. BharatNet Phase 2 and enterprise fiber connectivity will drive multi-year demand.

FMEG optionality — If the electricals segment (switches, fans, MCBs) gets traction through the distribution network, it could re-rate the company’s multiple meaningfully.

The Bear Case / Risks:

Copper price volatility — The company is a significant net buyer of copper. When copper prices spike (as they did in FY26), margins get squeezed. There’s limited ability to hedge multi-month forward exposure.

Intensifying competition — Polycab, KEI Industries, and Havells are all investing aggressively. Market share defence will require continuous capex and distribution investment.

FMEG scale remains elusive — The company has been trying to build the FMEG business for years and it remains a small contributor. Established players have stronger brand equity in switches and fans.

Margin recovery timeline uncertain — If copper stays elevated through FY27, the earnings upgrade cycle could be muted even as revenues grow.

SECTION VI: Valuation & Target Price

Current P/E: ~18–19x (trailing) Sector median P/E: ~38–40x Our target P/E: 22–24x (reasonable premium for market leadership, balance sheet quality, and growth)

The company doesn’t deserve to trade at sector median — it’s slower-growing and has margin issues. But the current 50%+ discount is excessive.

At 23x on FY27E EPS of ~₹46–48 (assuming moderate margin recovery), the fair value range is ₹1,050–1,100.

That’s approximately 25–30% upside from current levels over 12–18 months.

For a longer-term investor (5–7 years), if the company compounds earnings at 12–15% annually (consistent with the last 5-year track record), with a fair exit multiple, total returns of 3x–4x from current prices are reasonable.

The risk-reward is skewed in the investor’s favour — a debt-free, market-leading manufacturer in a structurally growing sector, at a near-decade low P/E, is not a stock that stays cheap forever.

This newsletter is for informational purposes only and does not constitute investment advice. Please consult a SEBI-registered investment advisor before making investment decisions. Equity investments are subject to market risks.