The Invisible Engine Powering India’s Retail Investing Boom

Section I — Investment Thesis & Summary

Here’s the simplest way to think about this business: every time someone in India opens a demat account, buys a stock, sells a bond, or transfers mutual fund units, this company quietly earns a fee. It doesn’t take on market risk. It doesn’t lend money. It just runs the plumbing of India’s capital markets — and collects a toll every single time the system is used.

The stock has pulled back roughly 37% from its 52-week high of ₹1,829. That drop is partly justified — earnings came under pressure in FY26 due to higher operating costs and the absence of one-off subsidiary dividends that had padded prior-year profits. But the underlying growth story? Very much intact. India’s retail investor wave is still in its early innings. At ₹1,150, you’re getting a structurally dominant, debt-free, high-ROE business at a more reasonable entry point than what was available a year ago.

The target of ₹1,550 implies roughly 35% upside, supported by earnings normalization in FY27 and continued demat account expansion.

Youtube Link:

Section II — Business Model & Operations

The business is elegantly simple. Think of it as the country’s official electronic vault for securities. When you buy shares through your broker, someone has to safely record that ownership in electronic form. That’s exactly what this company does — and it charges for every service along the way.

Revenue flows from three main buckets:

Annual Issuer Charges — companies pay to keep their securities registered here. More listed companies = more income. This is sticky and recurring.

Transaction Charges — every time securities change hands (buy, sell, pledge, transfer), a small fee is earned. This is the volume-sensitive piece, and it tracks market activity.

KYC & Online Data Services — the company runs a KYC Registration Agency used by mutual funds and other financial intermediaries. As digital financial services expand, this stream keeps growing.

As of the latest reported quarter, the business had crossed 16.5 crore active demat accounts — that’s 165 million investors. It holds over 80% market share in new account openings. Its closest competitor has roughly 4–5 crore accounts by comparison. That’s not a competitive edge. That’s a moat.

The only real competitor in India is NSDL, which recently filed for an IPO at a P/E of around 46–47x — a useful benchmark for valuation purposes.

Section III — Historical Financial Review

The numbers tell a clear story of acceleration.

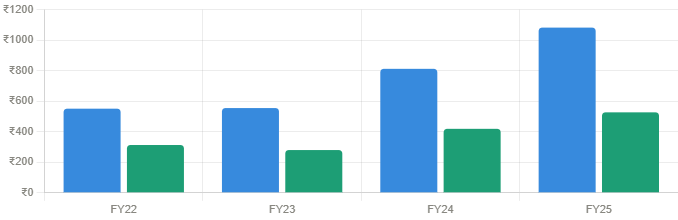

Revenue trajectory (₹ Crore):

YearRevenuePATFY22₹551 Cr₹313 CrFY23₹555 Cr₹280 CrFY24₹812 Cr₹419 CrFY25₹1,082 Cr₹527 Cr

The 3-year revenue CAGR from FY22 to FY25 works out to approximately 25%. PAT grew at a 5-year CAGR of roughly 38%. These are not ordinary numbers for a capital markets infrastructure company.

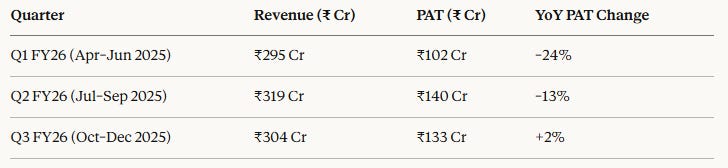

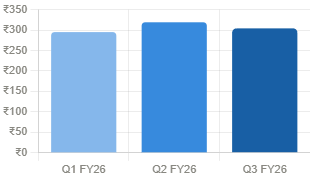

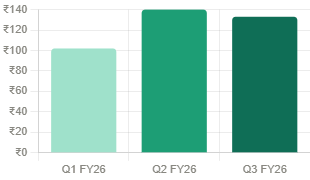

FY26 so far — the wobbly year:

Here’s the thing — FY26 looks worse than it actually is. Prior-year quarters benefited from large one-time dividend payouts from subsidiaries. Strip those out, and core operations are actually growing. The sequential rebound from Q1 to Q2 (PAT up 37% quarter-on-quarter) shows the underlying engine is running fine.

LTM (last 12 months) Diluted EPS stands at approximately ₹22–24. At ₹1,150, that puts the stock at roughly 48–50x trailing earnings. Not cheap by absolute standards. But for a business with this kind of moat, this return profile, and this growth runway, it’s fair — especially compared to NSDL’s IPO pricing.

ROE over the last three years has averaged ~30%. The company is debt-free. Dividend payout is consistent at ~55% of earnings.

Section IV — Growth Catalysts & Risks

Why this business keeps growing:

India’s financial penetration story is real. The number of demat accounts has grown from roughly 4 crore in FY20 to over 16.5 crore today. But here’s the kicker — India’s adult population is around 100 crore. Penetration is still under 17%. In developed markets, it’s 50–70%. The runway is enormous.

Every new account that opens is a permanent revenue stream. Every new mutual fund transaction, every pledge, every corporate action, every e-voting event — all fees. And this business gets to participate in all of it passively.

SEBI’s push for dematerialization of physical securities, digitization of insurance accounts, e-warehouse receipts, and digital government bonds all expand the addressable opportunity beyond traditional equity markets.

The subsidiary, CDSL Ventures Limited, runs the KYC Registration Agency (KRA) business for mutual funds. As SIP registrations and mutual fund folios grow, this subsidiary earns more. It’s a compounding multiplier on the core business.

Annual revenue & profit (₹ Crore)

What could go wrong:

Let’s be honest about the risks.

Market downturn risk: Transaction fee revenue is directly correlated to market volumes. In a prolonged bear market or low-activity period, this line item suffers. FY26 is a live example of this pressure.

Regulatory risk: SEBI controls the fee structure. Any revision to annual issuer charges or transaction fee caps could directly impact margins. This is a real and recurring risk for market infrastructure entities.

NSDL competition: NSDL’s upcoming listing will bring capital and management attention to the competitor. It won’t dislodge the incumbent’s market share overnight, but it sharpens the competitive dynamic.

Cost creep: Total expenses rose ~17% YoY in Q2 FY26 even as revenues dipped. Technology upgrades, regulatory compliance, and headcount are pushing costs higher. Margins have compressed from the peak of ~62–65% operating margins to the low-50s. If this continues, it’s a concern.

Concentration risk: The majority of revenues are still India-specific and capital market activity-specific. Global parallels like DTCC (US) or Euroclear suggest this model scales beautifully — but only within the domestic ecosystem.

Section V — Valuation & Target Price

The valuation framework here is straightforward. This is a capital-light, high-ROIC, monopoly-adjacent business. Comparable global market infrastructure entities trade at 30–60x earnings historically. NSDL’s IPO pricing at ~47x provides the closest domestic benchmark.

Base case assumptions (FY27 normalized EPS):

Assuming Q4 FY26 results come in around ₹130–140 Cr PAT (conservative), and FY27 shows a clean year without year-ago base effect distortions, normalized EPS could reach ₹26–28 by FY27.

Applying a 55x multiple (a slight premium to NSDL’s IPO pricing, justified by CDSL’s listing, liquidity, and market share dominance): Target = ₹27 × 55 ≈ ₹1,485–₹1,540

We’re pegging the target at ₹1,550, implying ~35% upside from current levels.

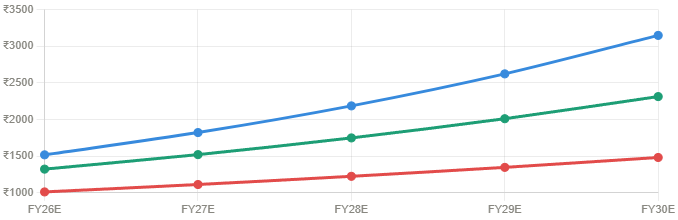

5-year return projection:

If EPS compounds at 15% annually (conservative, given the 38% 5-year historical CAGR), FY30 EPS could reach ₹42–45. At a 50x multiple, the stock trades at ₹2,100–2,250. That’s roughly 85–95% total return over 5 years, or ~13–14% CAGR — reasonable for a quality compounder purchased at fair value.

15-year perspective: If India’s demat account base reaches 50–60 crore (still only ~50% adult penetration), transaction volumes and issuer base grow proportionally, and the business continues to compound earnings at 12–15% annually, the stock could realistically deliver 8–12x from current levels. Patient capital will be rewarded.

FY26 quarterly performance (₹ Crore)

Section VI — Our Take

This is a business that benefits from India’s financial deepening without making any bets on individual companies, sectors, or market direction. It collects tolls on the highway. More cars on the highway = more tolls. India is putting more cars on the highway every single quarter.

The FY26 earnings dip is real, but explained. The long-term thesis is unbroken. The stock’s pullback from ₹1,829 to ₹1,150 has made the entry point materially better.

Buy. Add on dips below ₹1,050. Stop loss at ₹900. Target ₹1,550 in 12–18 months.

5-year return projection

Note: This newsletter is for informational purposes only and does not constitute SEBI-registered investment advice. Past performance is not indicative of future results. Please consult a registered financial advisor before making investment decisions.