The Hidden Infrastructure Stock Powering India’s Construction, Water & Housing Boom

Section I — Investment Thesis & Summary

India’s plastics sector is not glamorous. Nobody puts it on a list of “hot themes.” And yet, this company — India’s largest diversified plastics manufacturer — has quietly compounded wealth for patient investors for decades. The question today is whether the current price fairly reflects that track record, or whether the market is being too generous.

“The fundamentals are solid. The valuation is the problem.”

The stock trades near ₹3,950 against a 52-week range of ₹3,095–₹4,739. A P/E of roughly 62x on trailing earnings is hard to justify unless you believe the next two to three years will see a sharp earnings recovery. The good news: that recovery is actually plausible. The bad news: it is not here yet.

The call is HOLD. If you already own it, sit tight — the long-term thesis remains intact. If you are looking to add fresh capital, wait for either a better entry price (closer to ₹3,200–₹3,400) or confirmation of margin recovery, expected from Q4 FY26 onwards.

Youtube Link:

Section II — Business Model & Operations

Think of this company as the plumbing backbone of India’s construction boom. It manufactures and sells plastic products across eight distinct categories — but the one that really matters is plastic pipes and fittings, which alone drives about 67% of total revenue.

Here’s what that means in practical terms: every new apartment building, every irrigation project, every water distribution network — they all need pipes. This company makes over 14,000 variants of those pipes, from uPVC and HDPE to CPVC and polypropylene systems. That’s an enormous product catalogue that would take years for any competitor to replicate.

The remaining 33% of business is spread across:

Industrial moulded components

Packaging films

Moulded furniture

Cross-laminated films

Composite LPG cylinders

That last one — LPG cylinders made from composites instead of steel — is a niche but growing segment. The company just won a major supply order from BPCL for 2,00,000 cylinders of 10 kg capacity. Meaningful.

“14,000 product variants, zero meaningful debt. That’s a serious moat.”

Operations span multiple manufacturing plants across India. The company funds its own capital expenditure internally — ₹1,031 crore in recent capex cycles — without borrowing. Debt-equity ratio sits at an irrelevant 0.09x. That’s effectively debt-free.

In February 2026, the board elected M.P. Taparia as Chairman while he continues as Managing Director. The Taparia family has controlled this company since 1966. Long-tenured promoter families can be a double-edged sword, but here it comes with decades of capital discipline and consistent dividend payouts.

Section III — Historical Financial Review

Annual Revenue Trend (₹ Crore)

FY20 ████████████░░░░░░░░░░░░░░░ 5,512

FY21 ████████████████░░░░░░░░░░░ 6,355

FY22 ████████████████████░░░░░░░ 7,773

FY23 ████████████████████████░░░ 9,202

FY24 ██████████████████████████░ 10,134

FY25 ███████████████████████████ 10,446

TTM ███████████████████████████+ 10,717Revenue has grown from roughly ₹7,773 crore in FY22 to ₹10,446 crore in FY25 — a 3-year CAGR of ~10.4%. That sounds decent until you realise that earnings growth has been much weaker. The last twelve months diluted EPS sits around ₹64–₹66, but for FY26 the 9-month cumulative EPS is only ₹41.65, implying the full-year number will likely come in at ₹56–₹60. That would be a year-on-year decline.

FY26 Quarterly Performance

QuarterRevenue (₹Cr)Op. Profit (₹Cr)OPM %Net Profit (₹Cr)EPS (₹)YoY PATQ3 FY25 (Dec’24)2,51030912.3%18714.72—Q4 FY25 (Mar’25)3,02741613.7%29423.14—Q1 FY26 (Jun’25)2,60931912.2%20215.93—Q2 FY26 (Sep’25)2,39429712.4%16512.97-20.3%Q3 FY26 (Dec’25)2,68731411.7%15312.07-18.0%

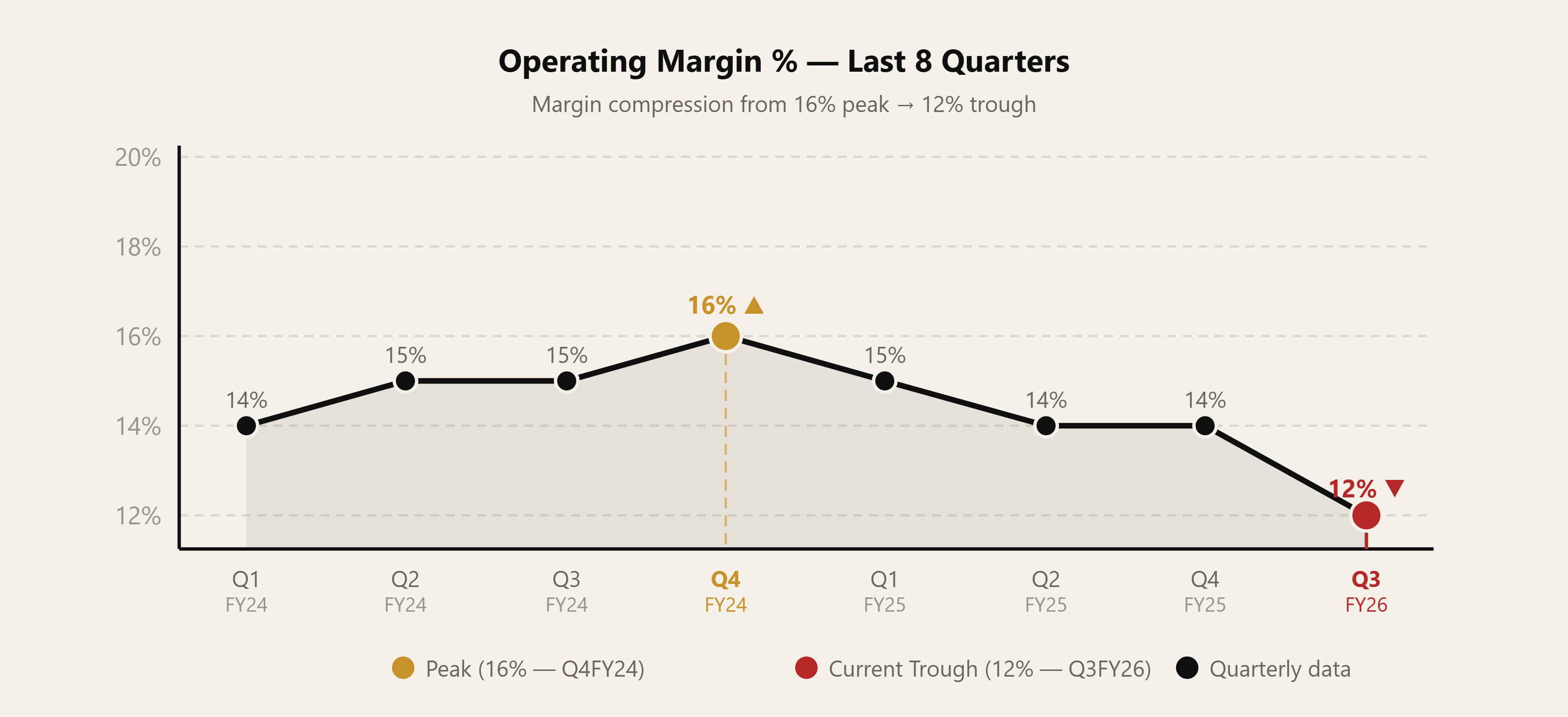

Operating Margin Trend (Last 8 Quarters)

Q1FY24 ████████████████ 14%

Q2FY24 █████████████████ 15%

Q3FY24 █████████████████ 15%

Q4FY24 ██████████████████16% ← Peak

Q1FY25 █████████████████ 15%

Q2FY25 ████████████████ 14%

Q4FY25 ████████████████ 14%

Q3FY26 ████████████ 12% ← CurrentThe pattern is uncomfortable but not unusual. PVC resin prices — the key raw material — have been volatile and unfavourable. Operating margins have compressed from 15–16% two years ago to around 12% now. Net profit in Q3 FY26 fell 18% year-on-year.

But here is the important context: the Managing Director noted that polymer prices have started moving up in 2026, which typically leads to better realisation for manufacturers. If that holds, margins should begin recovering in Q4 FY26 and into FY27.

Revenue actually grew 7% year-on-year in Q3 FY26 — it’s not a demand problem. It’s a margin problem. And that’s a very different, more solvable problem.

Section IV — Growth Potential & Key Risks

There’s a clear bull case here and it rests on three pillars:

India’s housing and infrastructure buildout — The government’s sustained push on Jal Jeevan Mission, urban infrastructure, and affordable housing creates structural demand for plastic piping for at least another decade.

Value-added product growth — Value-added product revenue grew 16% year-on-year in Q3 FY26, reaching ₹1,118 crore. These products carry better margins and signal a deliberate shift up the value chain.

Polymer price recovery — If PVC resin prices normalise or turn favourable in CY2026, operating margins could recover to 14–15%, which would push earnings meaningfully higher.

Catalysts to Watch 🟢

Polymer/PVC price recovery in CY2026

Government infra capex acceleration (Jal Jeevan, urban housing)

Value-added products hitting 25%+ of revenue mix

Composite LPG cylinder order book expansion

Margin recovery to 14%+ from Q4 FY26 onwards

Risks to Monitor 🔴

Prolonged PVC resin price volatility

Slower-than-expected government infrastructure spending

Real estate sector demand slowdown

Competition from unorganised sector on price

Valuation at 62x leaves no margin of safety

Let’s be honest about the valuation concern. A P/E of 62x is expensive — especially when earnings are declining. The market is essentially pricing in a full recovery AND a premium for quality. That’s not wrong, but it means the stock needs everything to go right. Any negative surprise — a bad monsoon, delayed government spending, another spike in polymer costs — and the stock has meaningful downside from here.

Section V — Valuation & Return Expectations

EPS Recovery Scenario

FY24 ₹84.2 ●────────────────

FY25 ₹75.6 ●────

FY26E ₹58E ●

FY27E ₹82E (recovery) ● ← Target scenario

╌╌╌╌ (estimated)The LTM diluted EPS is approximately ₹64. On a 12-month forward basis, if FY27 EPS recovers to ₹80–₹85 — a reasonable assumption if margins normalise — a fair P/E of 50–55x would give a target price of ₹4,000–₹4,700. The mid-point: ₹4,400.

5-Year Return Scenario

AssumptionValueFY27E EPS₹82EPS CAGR FY27–FY3212–14%FY32E EPS₹140–₹160Normalised P/E45–50xImplied Price FY32₹6,300–₹8,000Expected Return (5-yr)~60–100% total / ~10–15% CAGR

For a 5-year horizon, the math becomes more interesting. If the company grows EPS at 12–14% annually from FY27 (conservative, given its historical track record), the stock could deliver 10–15% CAGR — consistent with what this stock has historically delivered. Not spectacular, but reliable.

For a 10–15 year investor, this remains a strong compounding vehicle. It’s not cheap, but few truly quality businesses in India ever are.

Section VI — Balance Sheet Strength

This is the part that doesn’t get enough credit. The company runs a ₹10,000+ crore revenue business with essentially no debt. Capex is funded internally. Dividends are consistent. The balance sheet is one of the cleanest in its peer group among Indian mid-cap industrials.

That matters — especially in an environment where leveraged peers face real headwinds. When input cost cycles turn adverse (as they have), a debt-free company can absorb the pain and emerge stronger. A leveraged competitor cannot.

The Bottom Line

“India needs pipes. This company makes them better than anyone else. The only debate is the price you pay.”

The long-term story is not broken. Structural demand from India’s housing and infrastructure growth is real and enduring. The balance sheet is pristine. The brand and product depth are genuine competitive advantages built over decades.

What’s broken is near-term earnings, driven by input cost pressures that appear cyclical rather than structural. The recovery in polymer prices and margin normalisation are the key catalysts to watch.

At ₹3,950, the stock is not cheap enough to be an obvious buy, but not overvalued enough to sell a long-term holding.

HOLD. Target ₹4,400. Review at Q4 FY26 results.