The Business of Being the Default Choice

SECTION I: Investment Thesis & Summary

Most people haven’t consciously thought about buying its stock, but they’ve almost certainly used its products today. That’s not an accident. That’s a moat.

The stock has drifted ~13% below its 52-week high, largely because earnings growth has moderated from the blistering pace of FY23–24. Margin compression fears, input cost noise, and a general de-rating of premium-valued midcaps have all weighed on sentiment. But the core business? Completely intact. Actually, quietly getting stronger.

Simply put: A quality compounder at a price that’s gone from “extremely expensive” to just “expensive.” That’s usually when you should be buying, not avoiding.

SECTION II: Business Model & Operations

The company makes money the same way a great brand always does — by being the default choice. You don’t go to the hardware store and ask for “adhesive.” You ask for Fevicol. That’s brand equity worth infinitely more than any patent.

Here’s the revenue breakdown:

Adhesives & Sealants (~53%): Consumer-facing. Fevicol, Fevikwik, Fevistik. This is the heartland — carpenters, plumbers, homeowners, contractors. Volumes here are tied directly to India’s construction and renovation boom.

Construction & Paint Chemicals (~20%): Dr. Fixit, Roff. Waterproofing, tile-fixing, surface prep. Think of every new apartment getting finished — this product is in the walls.

Industrial Chemicals & Resins (~13%): Araldite, industrial adhesives, pigments. B2B customers, lower margins than C&B but growing steadily.

Art & Craft / DIY (~6%): Fevicryl, Hobby Ideas. Smaller but high-margin and insulated from economic cycles.

What’s happening right now operationally?

The Consumer & Bazaar (C&B) segment is firing on all cylinders — Unique Volume Growth (UVG) of 9.7% in Q3 FY26. This isn’t revenue inflation from price hikes; it’s actual physical volume being sold. Management has been clear that rural distribution expansion and the trade channel deepening are the primary growth levers.

FY25 saw the successful exit from the Pulvitec Brazil business (generating some one-time exceptional charges in prior quarters) — that’s now behind them, cleaning up the P&L substantially. The company is also investing behind new manufacturing capacity and the B2B segment, which they’ve flagged as the next big growth runway alongside the core C&B business.

In September 2025, the company rewarded shareholders with a 1:1 bonus issue — every existing share got one new share. This halved the stock price (mechanical adjustment) but doubled the share count. It’s a shareholder-friendly signal from management about their confidence in sustaining earnings.

Youtube Link:

SECTION III: Historical Financial Review

Revenue Growth Story (3-Year CAGR): ~11–12%

Revenue has grown from approximately ₹10,100 crores in FY22 to roughly ₹14,160 crores on a trailing twelve-month basis. That’s consistent, compounding growth — not a one-year spike. Volumes have led this, not just price increases.

Earnings Per Share (Diluted, LTM): ~₹22–24 per share (post-bonus adjusted)

The bonus issue makes direct year-on-year EPS comparisons tricky unless you adjust. On a pre-bonus basis, FY25 EPS was ~₹40–41, which post-bonus translates to ~₹20–21. Q1 FY26 showed ₹6.61 EPS (post-bonus equivalent), Q2 FY26 at ₹5.68, and Q3 FY26 at ₹6.06 — suggesting annualised run-rate of around ₹23–25 per share.

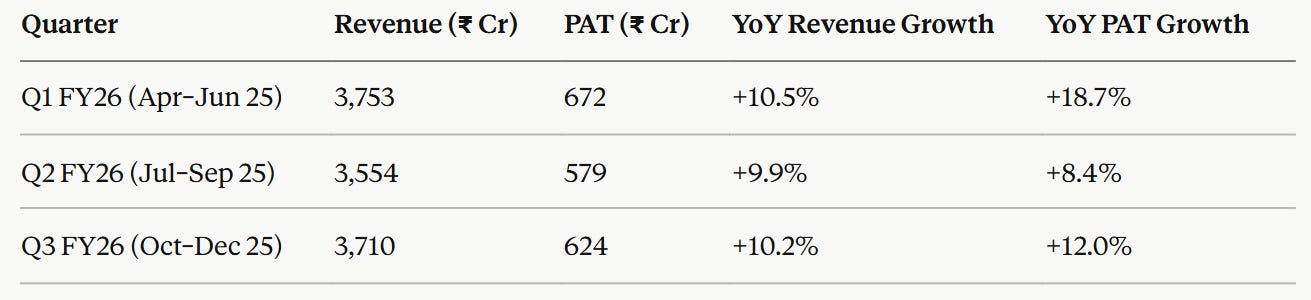

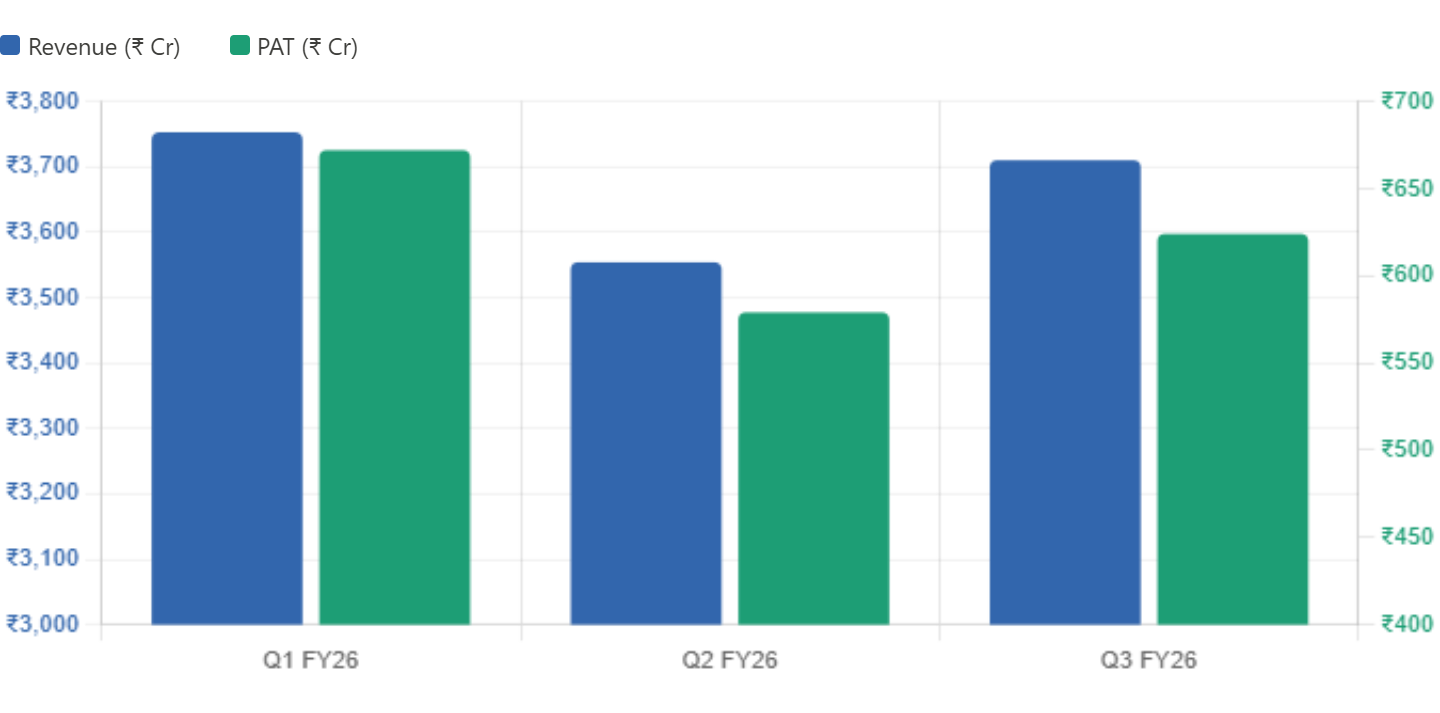

FY26 Quarterly Performance:

Q1 was the star quarter — strong volumes, margin expansion to 25% EBITDA, and exceptional profit growth. Q2 dipped sequentially (this is seasonal — Q2 is typically softer) but still showed healthy YoY improvement. Q3 bounced back well with 10.2% revenue growth and a 24.2% EBITDA margin.

The pattern here is a company delivering consistent 10%+ revenue growth every single quarter while holding margins above 23–24%. That’s not easy to do in a commodity-input business.

Return Metrics:

Return on Equity (ROE): ~22–23% — exceptional. This means for every ₹100 of equity capital, the company earns ₹22–23 in profit.

Return on Capital Employed (ROCE): ~41.7% — this is an outstandingly capital-light business.

Net Profit Margin: ~16–17%

Operating Cash Flow: Strong and consistent, supporting both capex and dividend payments.

SECTION IV: Valuation — The One Honest Conversation

Let’s be direct about this: the stock is not cheap. It never has been.

Current P/E: ~58–60x trailing earnings Price-to-Book: ~13.5x

Those are big numbers. At ₹1,370, the market is paying a massive premium for certainty — for the near-certainty that Fevicol will remain the dominant adhesive brand in India for the next two decades, that margins will stay elevated, that volume growth will compound.

Is that premium justified?

Here’s the calculus: If the company grows EPS at 15% annually for the next 5 years (which is below its historical average), you’d reach ~₹47–50 EPS by FY31. Apply a 40x multiple (still very premium, but warranted for this quality) and you get a stock price of ₹1,880–₹2,000. That’s a ~38–45% return from current levels over 5 years.

Not spectacular. But the margin of safety comes from the downside protection: a business with 70% promoter holding, near-zero debt, 23%+ EBITDA margins, and ₹14,000 crore revenue doesn’t typically crater.

Target Price: ₹1,750 (12–18 month view, ~27% upside from ₹1,370) This assumes EPS recovery to ₹28–30 post-FY26 and multiple compression to 58–60x as growth normalises.

For a 10-year horizon: The case is much more compelling. A 14–16% CAGR in PAT puts EPS well north of ₹80–90 (post-bonus adjusted) by FY35. At a reasonable 45x, that’s a stock price in the ₹3,600–₹4,000 range. Not a 10-bagger, but a solid 3–4x compounder with far lower risk than most alternatives.

SECTION V: Risks — The Honest Part

Raw Material Volatility: VAM (Vinyl Acetate Monomer), a key input, is an imported petrochemical. When crude oil prices spike, margins compress. The company has managed this well historically but it’s a recurring risk.

Valuation Risk: This is real. At 58–60x P/E, there’s little room for disappointment. If volume growth slips to 5–6% for two consecutive quarters, expect a 15–20% de-rating.

Competition in Construction Chemicals: Dr. Fixit and Roff face increasingly well-funded competition from Asian Paints’ Smartcare and BASF’s construction chemicals division. Market share erosion here is a slow but watchable risk.

Rural Slowdown: About 35–40% of C&B volumes come from Tier 3–5 towns and rural markets. A prolonged rural consumption slowdown would hurt volume growth meaningfully.

B2B Segment Margins: As the company pushes harder into B2B (industrial customers), margins in that segment are structurally lower than the premium C&B business. A revenue mix shift toward B2B over time could weigh on blended margins.

SECTION VI: Final View

This is a business most investors understand intuitively — because they’ve used Fevicol, applied Dr. Fixit sealant, or fixed something with Fevikwik. What’s underappreciated is the financial quality behind those brands.

₹14,000 crore in revenue. 23%+ EBITDA margins. ₹2,300+ crore in annual profit. 40%+ ROCE. Near-zero debt. 70% promoter ownership. Consistent 10%+ volume growth.

The stock has underperformed the Sensex by a meaningful margin over the past 12 months — down ~13% from highs while the broader market recovered. That’s your entry window.

Verdict: BUY on dips toward ₹1,300–₹1,350. Hold with a 3–5 year horizon.

This is not a trade. This is the kind of stock you buy, tuck away, and check once a year.