The ₹50 Lakh Regret: What I Learned from Those Who Waited

A Successful software architect, owns two flats, drives a decent car. But when the conversation turned to investments, his face clouded over. "I've been meaning to start investing for eight years now," he said, almost whispering. "Every Diwali, I tell myself 'next month for sure.'"

Eight years. That's not just procrastination—that's compound interest working in reverse.

See, here's what most people don't grasp about delayed investing. It's not just about the money you don't make. It's about the exponential growth you never get to experience. And after three decades of watching brilliant people make this same mistake, I've noticed some patterns that might surprise you.

The "Perfect Timing" Trap

Rohit, a CA from Mumbai, waited for the "right market conditions" to begin investing in 2016. He wanted to time his entry perfectly. The Sensex was around 27,000 then. Today? It's crossed 80,000. His perfectionism cost him nearly 200% returns.

But here's the kicker—even professional fund managers rarely time markets correctly. I remember analyzing data from 2008 to 2023, and discovered something fascinating. Investors who started during market crashes (2008, 2020) didn't necessarily outperform those who began during seemingly "expensive" periods. Time in the market consistently beat timing the market.

The real enemy isn't market volatility. It's analysis paralysis disguised as prudence.

The Income Excuse That Doesn't Add Up

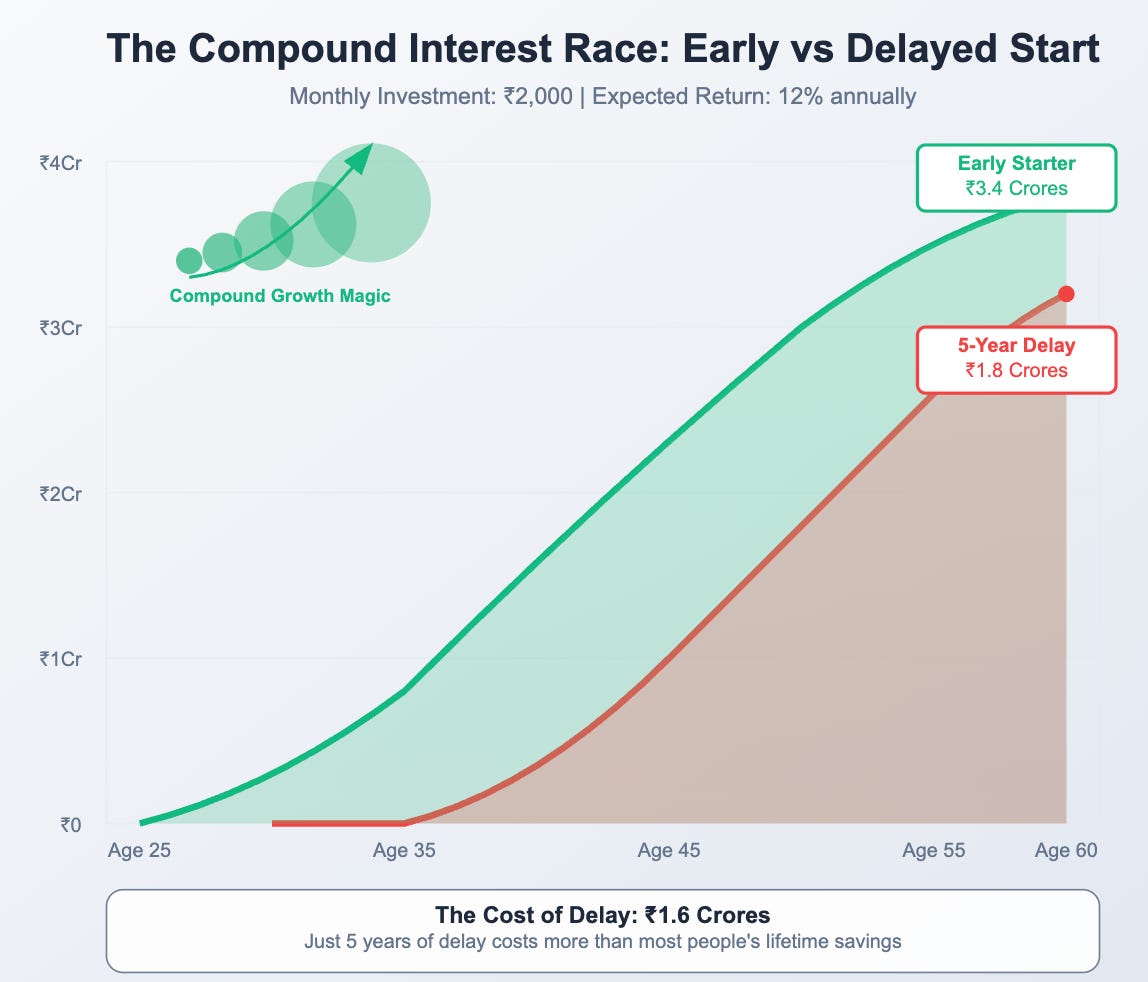

"I'll start investing when I earn more," said Meera, a marketing executive earning ₹8 lakhs annually. She was convinced that starting with ₹2,000 monthly wouldn't make a difference.

Let me show you something that might change how you think about small amounts. If Meera had started with just ₹1,000 monthly at age 25, assuming a conservative 12% annual return, she'd have ₹1.7 crores by age 60. Double that to ₹2,000, and she's looking at ₹3.4 crores.

But wait, here's where it gets interesting. If she delays by just five years and then starts with ₹3,000 monthly (50% more), she'll still end up with only ₹2.9 crores. The five-year delay cost her ₹50 lakhs, even with higher contributions.

That's the mathematics of compound interest. It rewards early starters disproportionately.

The Knowledge Paralysis

Somewhere along the way, we've made investing seem impossibly complex. Suresh, an engineering manager, spent two years researching different mutual funds, reading annual reports, comparing expense ratios. Two years of research. Zero rupees invested.

Here's what I've observed after managing portfolios worth thousands of crores: the difference between a "good enough" start and a "perfect" start is often negligible over long periods. But the difference between starting and not starting? That's everything.

You don't need to understand derivative pricing models to begin. You need to understand this: inflation is silently eroding your savings every single day you delay.

The Family Pressure Reality

This one's uniquely Indian, and rarely discussed in financial literature. Ajay from Pune couldn't start his SIPs because every spare rupee went to his sister's wedding preparation. Then his father's medical expenses. Then property down payment for the family home.

I get it. Indian families are ecosystems, not individuals. But here's a perspective shift that helped Ajay: he started viewing his investment journey as building a financial safety net for his family, not just himself. When the next family emergency hits—and it will—who do you think they'll turn to? The family member with investments, or the one with just a salary?

The Behavioral Economics of Regret

After interviewing hundreds of delayed investors, I noticed something curious. The regret isn't proportional to the financial loss. People who delayed by two years often felt worse than those who delayed by five. Why?

Because the two-year delayers could clearly visualize the alternative timeline. They knew exactly which mutual funds they had shortlisted, remembered the specific conversations about starting. The five-year delayers had hazier memories, making the regret feel less acute.

This suggests something profound about human psychology and investing. The pain of regret might actually be more about clarity than magnitude.

So what can freshly employed individuals learn from these stories?

Start imperfectly, but start immediately. Open that demat account this weekend, not next month. Begin with whatever amount doesn't strain your budget—even ₹1,000 monthly makes a difference. Choose a simple diversified mutual fund rather than spending months researching the "optimal" portfolio.

Your future self won't care that you started with a basic strategy. But they'll definitely care that you started.

The wedding conversation with Pradeep ended with him asking for my fund recommendations. I gave him something better: I made him promise to invest his first ₹5,000 within 48 hours, regardless of which fund he chose.

Because sometimes, the best investment advice isn't about which stocks to buy. It's about overcoming the inertia that keeps you from buying anything at all.