Tech Mahindra Share Price Target 2026: Growth Outlook, Risks & Long-Term Potential

The IT Giant Under Pressure: Can This Stock Weather the Storm?

The stock’s trading at ₹1,571 right now with a market cap of ₹1,53,885 Crores. Fair value sits around ₹1,950, giving you a 24% upside over the next 12 months. My call? HOLD for existing investors, ACCUMULATE on dips below ₹1,450.

Here’s why: the company’s grinding through a tough turnaround after getting hammered in FY24, but the latest quarters show momentum’s finally building. They’re clawing back margins and landing bigger deals. The catch? Growth is still sluggish and the entire IT sector’s facing headwinds.

Youtube Link:

How They Make Money

This is one of India’s top five IT service companies. They write code, manage tech infrastructure, and help businesses go digital. Think of them as the company that telecom operators call when their networks need upgrading, or banks hire to build their mobile apps.

The revenue split is straightforward: about 45% comes from communications (telecom companies), 25% from manufacturing and financial services combined, and the rest from retail, healthcare, and government work. They’ve got operations across 90 countries serving 1,100+ clients globally.

The big differentiator?

They’re part of the Mahindra Group, which gives them muscle in manufacturing and automotive tech. They’ve been aggressively pushing into AI and cloud services lately - every major deal now has these elements baked in. The deal pipeline’s been strong with consistent large contract wins.

The Numbers Tell a Recovery Story

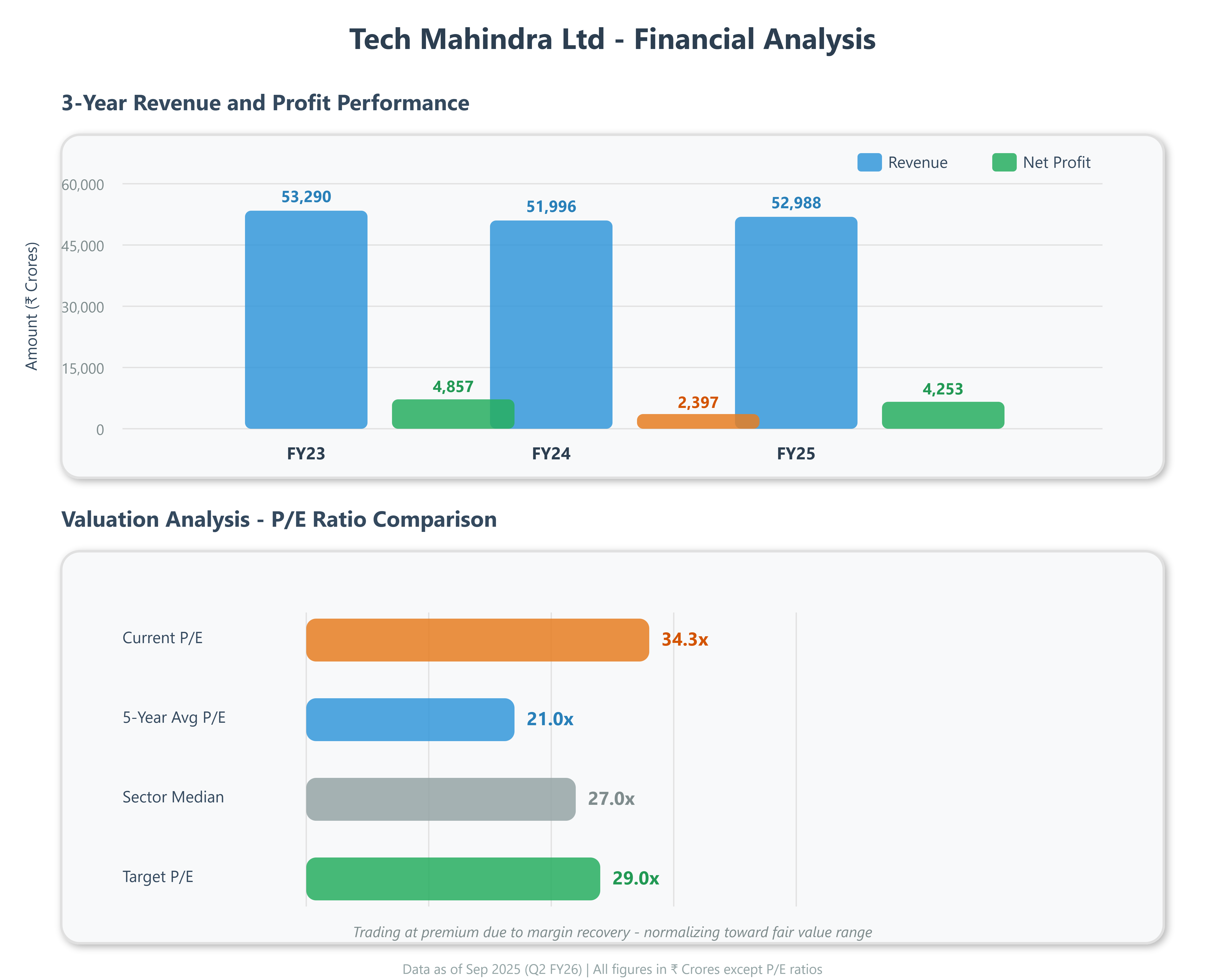

Revenue’s grown at just 6% annually over the past three years. That’s weak for an IT company. FY24 was brutal - profits dropped significantly as they bled margins trying to restructure the business. Things started improving from mid-FY25 onwards.

For FY25, they did ₹52,988 Crores in revenue with net profit of ₹4,253 Crores. That’s earnings per share of ₹43.43. The trailing twelve months through September 2025 shows revenue of ₹54,016 Crores with EPS at ₹45.81 - showing the recovery trend.

The latest quarter (Q2 FY26 ending September 2025) delivered ₹13,995 Crores in revenue and ₹1,202 Crores profit. Operating margins hit 15%, up from the 9% low during FY24. That’s six straight quarters of margin expansion - they’re executing the turnaround.

Cash generation’s solid - they generated ₹5,786 Crores from operations in FY25. Debt’s minimal at ₹2,025 Crores against a strong balance sheet. They’re almost debt-free, which is impressive for a company this size. Book value per share is ₹281.

They paid out ₹40.50 in dividends during FY25 - that’s a 94% payout ratio. For FY24 it was even higher at 150% as they returned cash during the tough year. They’ve maintained consistent dividend payouts even through the rough patch.

Valuation: Premium for the Recovery

The stock’s trading at a P/E of 34.3x based on FY25 earnings. That looks expensive at first glance. The 5-year average P/E was around 20-22x. You’re paying a premium because the market’s betting on the turnaround gaining steam.

Price-to-book is 5.6x - that’s reasonable for quality IT firms with asset-light models. ROE is 14.6% currently, recovering from the lows. It’s below the historical 18% but trending in the right direction. ROCE sits at 18.6%, which is decent but still below the 22-25% these companies delivered in better times.

Here’s the thing: if they can stabilize margins at 14-15% and get revenue growth back to 8-10%, the stock deserves 28-30x earnings. That gets you to ₹1,950-2,000 as fair value. If execution falters, it could drop back to ₹1,300-1,400.

Dividend yield is 2.86% - not spectacular, but they’re committed to returning cash. The sector median P/E is around 26-28x. Tech Mahindra’s trading above that because margins are improving faster than peers - they’ve shown consistent operational leverage for six quarters now.

The stock’s down 12% over the past year even as earnings recovered. That disconnect creates opportunity if you believe the turnaround’s real.

What Could Go Right (and Wrong) Over the Next Decade

If management executes their plan, you’re looking at 12-16% annual returns over the next 10 years. That assumes revenue grows 7-9% annually and margins stabilize at 14-15%. Add in dividends, and you’re pushing 14-18% total returns.

The bull case: Deal wins have been strong. The communications vertical (their biggest chunk) is stabilizing after years of pain. Manufacturing and auto clients are spending on digital transformation and 5G rollouts. AI services are ramping up as a new revenue stream. If global tech spending picks up, they’re positioned to capture share.

Promoter holding is steady at 35% (Mahindra & Mahindra owns the stake through Mahindra Group). They’re not selling, which signals confidence. DIIs increased their stake from 26% to 35% over the past two years - domestic institutions are clearly betting on the recovery. FIIs reduced from 27% to 21%, but that’s sector-wide, not company-specific.

Capital allocation’s sensible: they’re paying out 60-90% of profits as dividends, doing small tuck-in acquisitions, and reinvesting in AI and automation capabilities. No crazy empire building or value-destroying M&A.

The risks?

First, the IT sector’s facing structural headwinds. Clients are cutting costs, deals are taking longer to close, and pricing power’s weak. Second, Tech Mahindra’s concentrated in telecom, which is a slow-growth segment globally. Third, they’re heavily exposed to developed markets - any recession in the U.S. or Europe kills demand immediately.

Fourth, wage inflation in India runs 6-8% annually. They need to keep hiring to grow, which constantly pressures margins. Fifth, competition’s brutal - TCS, Infosys, HCL, and Wipro are all chasing the same deals with aggressive pricing. Sixth, the recovery could stall if large deal execution stumbles.

Currency risk is real - most revenue comes from exports, so a strong rupee directly hurts reported numbers. They hedge some of this but not all. Regulatory risk is minimal since they’re a pure services play with no controversial businesses.

The India angle: The government’s pushing digital infrastructure, manufacturing, and telecom upgrades under various initiatives. Tech Mahindra’s well-positioned for domestic contracts. This could become a bigger revenue driver over time as India digitizes.

The 10-15 year outlook depends entirely on whether they can grow revenue at 8%+ while maintaining 14-15% margins. If yes, the stock works at current levels. If revenue growth stays stuck at 5-6%, you’ll get mediocre returns even with the dividend yield.