Tata Elxsi – Stock Research Report | Q4 FY2025 Results Analysis (as of April 2025)

Ticker: TATAELXSI | CMP: ₹4,900 | Market Cap: ₹30,522 Cr | P/E: 38.9x

Executive Summary

Tata Elxsi delivered a mixed performance in Q4 FY25, with flat year-over-year revenue growth (+0.3%) at ₹908.3 crore but concerning profitability metrics as PAT declined 12.4% YoY to ₹172.4 crore. The board has declared a final dividend of ₹75/share, translating to an attractive yield of 1.53% at current market price, despite margin pressures and slowing growth compared to its historical trajectory.

📌 Detailed Quarterly Results Breakdown

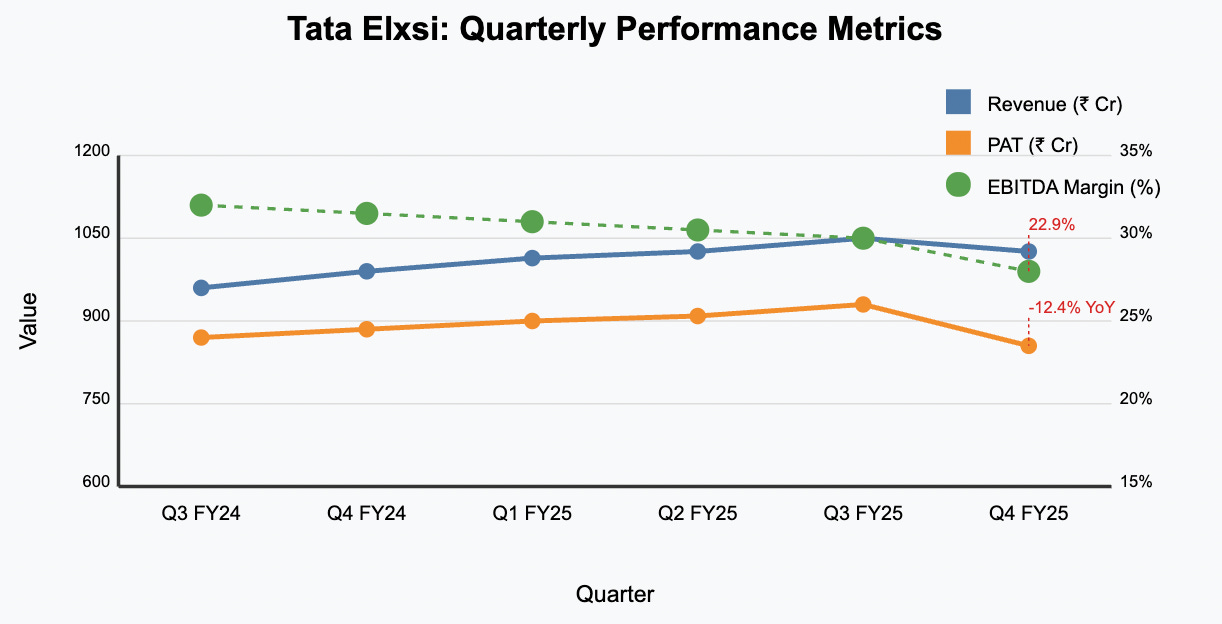

Consolidated Total Revenue: ₹908.3cr (+0.3% YoY, -3.3% QoQ) - Revenue remained essentially flat, suggesting growth challenges in key segments

Operating EBITDA: ₹208cr (-20.3% YoY) - Significant margin contraction from 28.8% to 22.9% reflects operational pressures

Net Profit After Tax: ₹172.4cr (-12.4% YoY, -13.4% QoQ) - Double-digit profit decline signals intensifying cost pressures

Diluted Earnings Per Share: ₹27.68 (-12.5% YoY) - EPS deterioration directly impacting shareholder returns

📊 Visualizing Performance Trends

📈 Comprehensive Growth Analysis

Sequential Revenue Growth (QoQ): -3.3% | Annual Revenue Growth (YoY): +0.3% - Growth has stalled considerably compared to the company's 3-year average of 14.7%

Sequential Profit Growth (QoQ): -13.4% | Annual Profit Growth (YoY): -12.4% - Profit deceleration continues amid margin pressures

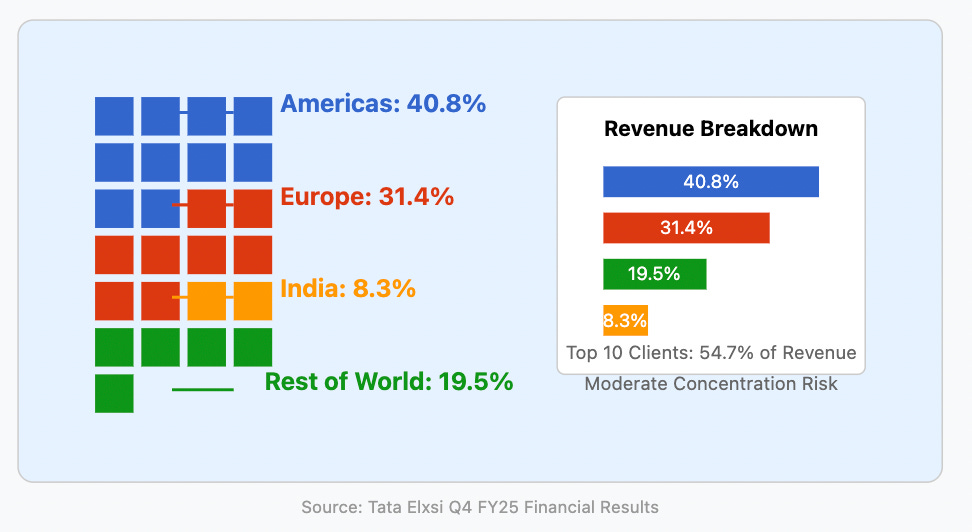

Revenue Mix Diversification: Geographic exposure remains well-balanced with Americas (40.8%), Europe (31.4%), India (8.3%), and RoW (19.5%)

Profitability Margin Trend: Declining - EBITDA margins contracted substantially from 28.8% in Q4FY24 to 22.9% in Q4FY25

🌍 Geographic Revenue Distribution

💰 Operational Cost Structure Analysis

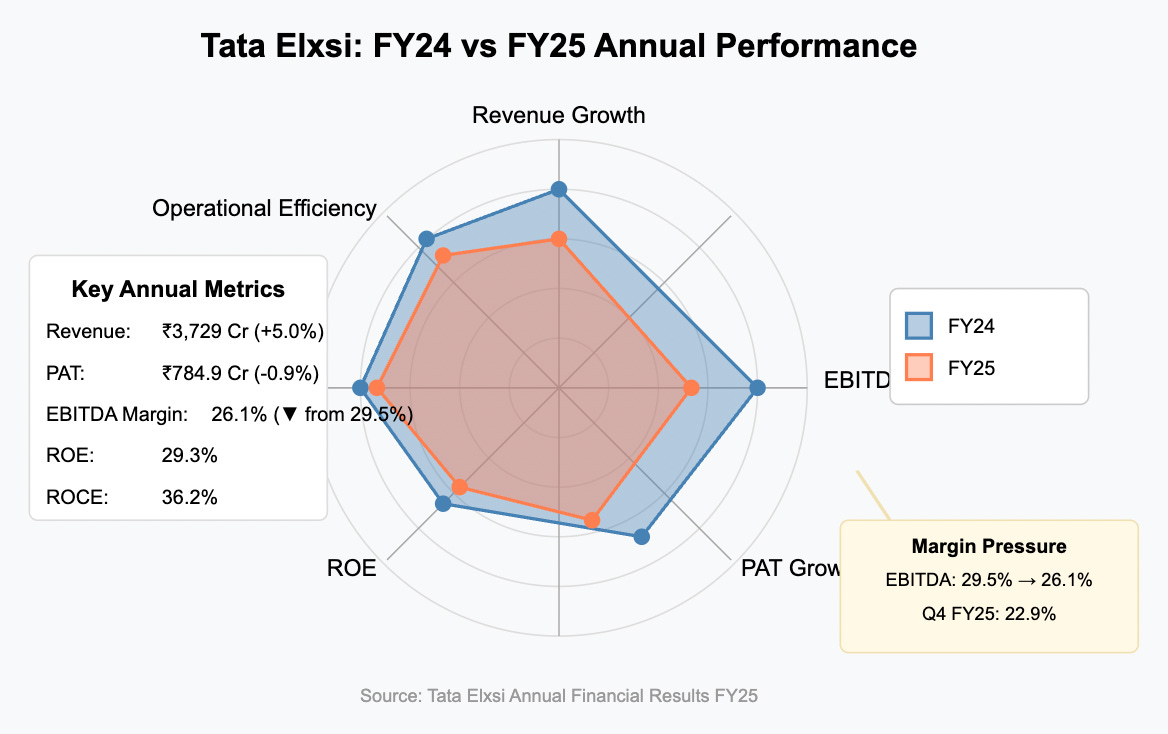

Employee/Personnel Expenses: Increasing pressures with rising attrition at 13.3%, marginally up from previous periods

Finance/Interest Expenses: Minimal impact with debt levels remaining low at ₹192cr, maintaining the company's strong balance sheet

Margin Compression: EBITDA margin declining from 29.5% (FY24) to 26.1% (FY25), with Q4FY25 further deteriorating to 22.9%

📊 Annual Performance Metrics

🏗️ Strategic Growth Roadmap

Transportation Vertical: Expanding SDV capabilities with new European OEM deals, Suzuki/Nidec ODCs, and UK design hub expansion

Media & Communications: Leveraging AI-driven platforms like NEURON for network automation and securing significant streaming platform modernization deals

Healthcare & Life Sciences: Building momentum in connected care, digital therapeutics, and AI-enhanced diagnostics with new multi-year deals

Aerospace & Defense: Strengthening domestic partnerships (HAL, ISRO) while focusing on emerging UAV and eVTOL technologies

💸 Valuation Analysis & Fair Value Assessment

Current Price-to-Earnings Ratio: 38.9x - Trading at premium multiples despite growth challenges

Enterprise Value to EBITDA Multiple: ~29x - Above sector averages, reflecting investor confidence in long-term potential

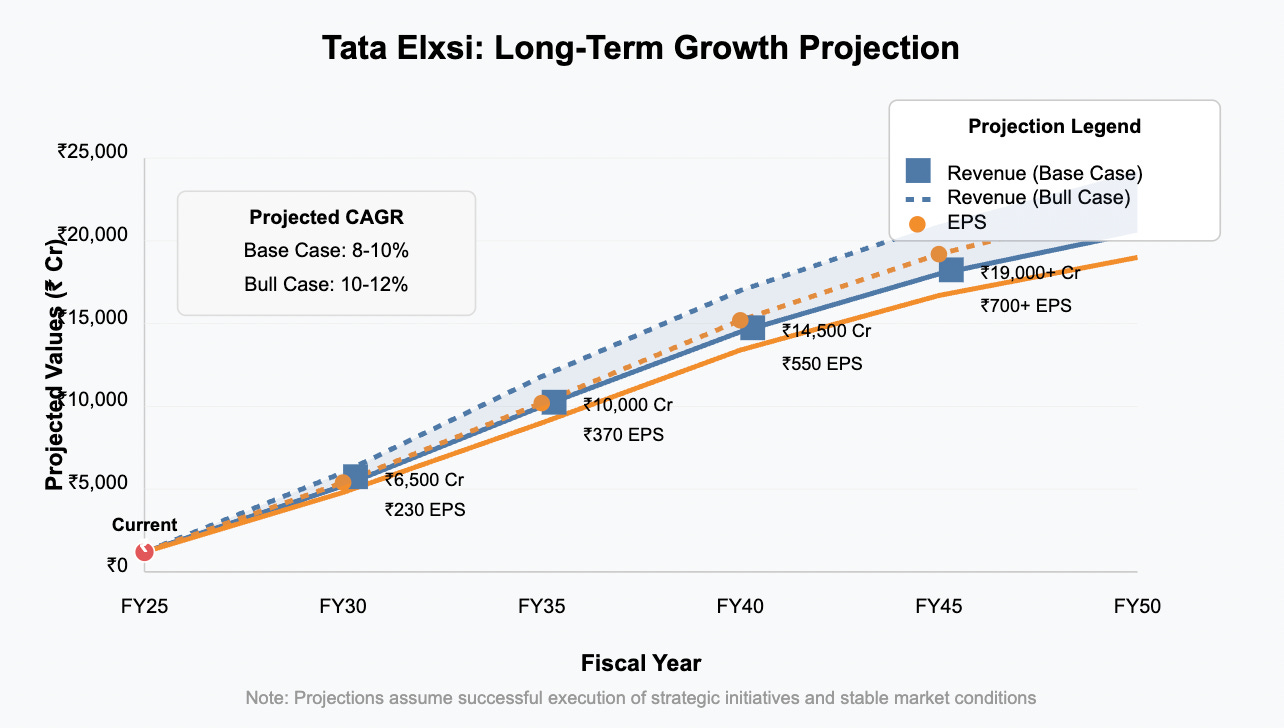

Estimated Fair Value Range: ₹4,200-₹5,600 based on DCF models with 8-10% CAGR growth assumptions

Long-Term Potential: Projected 8-10% CAGR returns over 15-20 years if execution remains strong

📊 Long-Term Growth Trajectory

Management Commentary Highlights

"While we faced near-term growth challenges amid global macroeconomic uncertainties, our landmark deals in transportation and media verticals provide strong revenue visibility. Our investments in IP and next-generation technologies position us well for when spending normalizes," stated CEO Manoj Raghavan during the earnings call.

"The margin contraction this quarter stems primarily from investments in new capabilities and some pricing pressures in mature service lines. We expect margins to stabilize as our strategic deals ramp up in the coming quarters," noted CFO Muralidharan HV.

Industry Context & Competitive Positioning

Tata Elxsi continues to outperform the broader IT services industry with its specialized focus on high-value design-led engineering services. While tier-1 IT firms struggle with low single-digit growth, Tata Elxsi's specialized positioning in emerging technologies like SDVs, digital health platforms, and media tech automation provides structural advantages despite the current growth pause.

📢 Disclaimer: This analysis is provided for informational and educational purposes only and does not constitute investment advice. The author may hold positions in securities discussed. Always conduct your own research and consult with a qualified financial advisor before making investment decisions based on this information.

Good insights