Supporting Our Parents: Investing to Secure Family Well‑Being

Father needed a knee replacement surgery, and the family's savings had been wiped out by her younger brother's engineering fees just six months earlier. "I wish I'd started investing the day I got my first salary," she said. "I thought I had time."

Here's the thing about time – it's both our greatest ally and our most deceptive enemy when it comes to building family wealth.

The Indian Family Financial Reality Check

Let's be honest. As young professionals in India, we're not just planning for ourselves. We're often the financial backbone for multiple generations. Your wedding, your parents' retirement, your sibling's education, maybe even a grandparent's medical expenses – it all somehow becomes... well, your responsibility.

I remember when I got my first job at 23, earning ₹35,000 a month. My dad sat me down and said, "Beta, now you can start helping with the household expenses." What he didn't say (but I realized later) was that I also needed to start thinking about his retirement. And my wedding. And that inevitable medical emergency that seems to hit every Indian family.

The math is actually quite scary when you break it down. Average wedding costs in metro cities? ₹15-20 lakhs. Parents' retirement needs? At least ₹50 lakhs if you want them to maintain dignity. Medical emergencies? Sky's the limit.

But here's where early investing becomes your superpower.

The Wedding Fund That Builds Generational Wealth

Most people think wedding planning means opening a fixed deposit two years before the big day. Wrong approach entirely.

Start investing ₹10,000 monthly in equity mutual funds from your very first salary. Sounds impossible? Let me break this down differently. That's ₹333 per day. Less than what you probably spend on coffee and snacks combined.

In seven years – a typical timeline from first job to marriage – that ₹8.4 lakhs becomes approximately ₹12-15 lakhs (assuming 12% returns). Not life-changing money, but here's the beautiful part: you've built the investment habit, and more importantly, you haven't touched your emergency fund or your parents' savings.

Now, let's talk about something most financial advisors won't tell you...

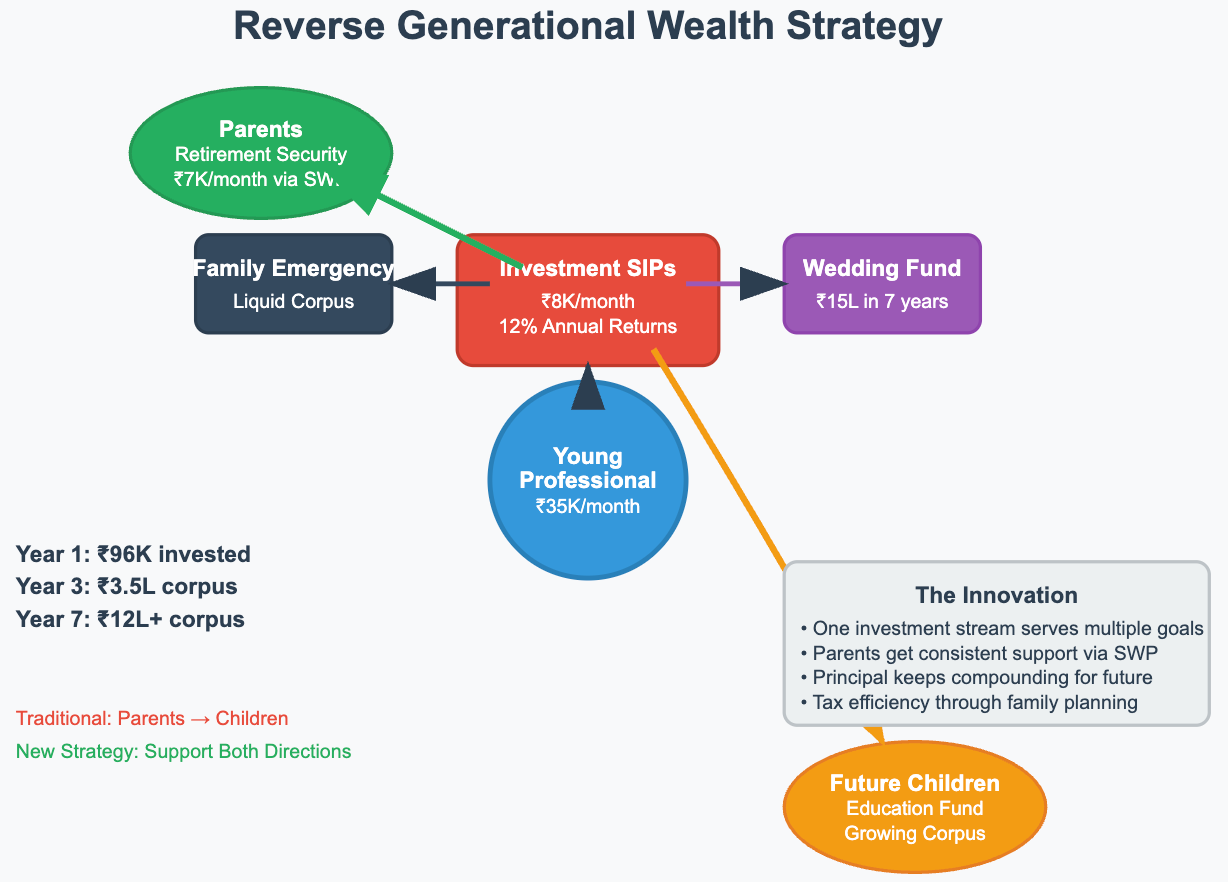

The Reverse Generational Wealth Strategy

Traditional wealth building flows downward – parents to children. But in modern India, we need to think differently. Your early investments can create an upward flow that supports your parents while simultaneously building downward wealth for your future children.

Consider this: instead of giving your parents ₹5,000 monthly for household expenses from your salary, invest ₹8,000 in an SIP and give them ₹3,000. After three years, start a SWP (Systematic Withdrawal Plan) that gives them ₹7,000 monthly while your principal keeps growing. You've essentially created a pension fund for your parents using compound growth.

This isn't just about money – it's about dignity. Your parents don't want to be dependent on your monthly salary fluctuations. They want security.

The Unknown Insights That Change Everything

Here's what most young investors miss: taxation efficiency in family wealth building.

Use your parents' lower tax brackets. If your dad is retired and in the 5% tax bracket while you're paying 20% plus cess, let him be the primary holder on long-term investments. The tax savings alone can boost your family's wealth by 15-20% over a decade.

Another hack? PPF accounts. Open one for yourself, encourage your parents to open theirs. That's ₹4.5 lakhs of tax-free growth potential per year per family member. Most families never maximize this because they think of individual planning instead of collective wealth building.

But perhaps the most powerful strategy is the "Family Emergency Corpus." Instead of each person maintaining separate emergency funds, create a larger family corpus in liquid funds. Better returns than savings accounts, and the collective size provides better risk coverage.

The Compound Growth of Family Security

The real magic isn't just in the numbers – it's in the peace of mind compound interest creates for your entire family. When your parents know there's a growing corpus for their medical needs, they sleep better. When you know your wedding won't derail your career savings, you make better life decisions.

I've seen friends postpone marriages because they couldn't afford them, then rush into ill-planned financial decisions later. I've seen others take personal loans for parent's medical emergencies, creating debt cycles that last years.

Early investing breaks these cycles.

Your Next Steps

Start tomorrow. Not next Monday, not next month. Tomorrow.

Open three SIP accounts: one for family emergencies (hybrid funds), one for wedding expenses (balanced advantage funds), and one for long-term wealth (equity funds). Start with whatever amount doesn't hurt – even ₹2,000 each is fine. The habit matters more than the amount initially.

And remember – you're not just investing money. You're investing in your family's dignity, your parents' security, and your own peace of mind. That's generational wealth in its truest form.

The best time to plant a tree was 20 years ago. The second-best time is now. Your family's financial tree is waiting.