Stock Analysis: Chemical Sector Multibagger Potential?

This stock’s trading cheap because the market hasn’t noticed how consistently they’re growing their cash flow and profits - they’re up 73% over three years while the stock’s barely moved.

How They Make Money

Xxxxxxxx does something pretty unique - they turn industrial waste into cash. They’re India’s biggest producer of low bulk density aluminum fluoride, making about 15,000 metric tons a year at their Visakhapatnam plant. Think of aluminum fluoride as a flux that helps aluminum smelters lower their melting point during production - basically an essential industrial chemical.

Here’s what’s smart: they source their raw materials from fertilizer plant effluents. So they’re taking what would be waste and converting it into aluminum fluoride, plus useful byproducts like silica and calcium fluoride. It’s a “wealth from waste” model that gives them a cost advantage.

They sell to aluminum smelters across India and export too - they even have a regular contract with Dubai Aluminium. Recently, they finished expanding their Visakhapatnam plant in 2021 and added a 3 MW solar plant to cut energy costs. In 2022, they set up a joint venture in Jordan to tap into Middle Eastern markets.

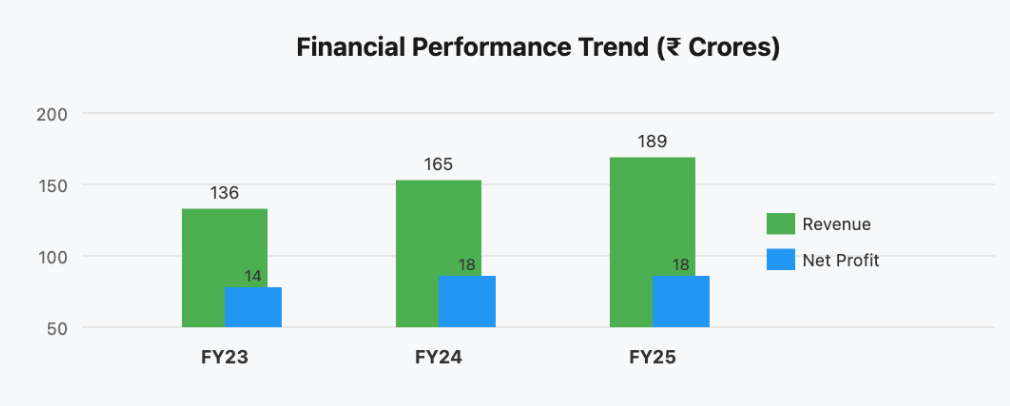

The Numbers Tell a Growth Story

Revenue’s been climbing at 29% annually over the last three years, hitting ₹189 crores in FY25. That’s real growth, not accounting tricks. The trailing twelve-month revenue is around ₹200 crores as of September 2025.

Earnings per share hit ₹24 in FY25, up from ₹23.20 the year before. More importantly, profits have jumped 73% over three years - from ₹4 crores in FY22 to ₹18 crores in FY25. The latest quarter (Q2 FY26) showed net profit of ₹7.93 crores, up 19% from last year and a whopping 156% jump from the previous quarter.

Operating margins are solid at 19-20%, and they’re throwing off good cash. Operating cash flow in FY25 was ₹12 crores. They’re also keeping debt reasonable - debt to equity is around 19%, which is healthy. The company paid out ₹3 per share as dividend in FY25.

Why This Stock Makes Sense

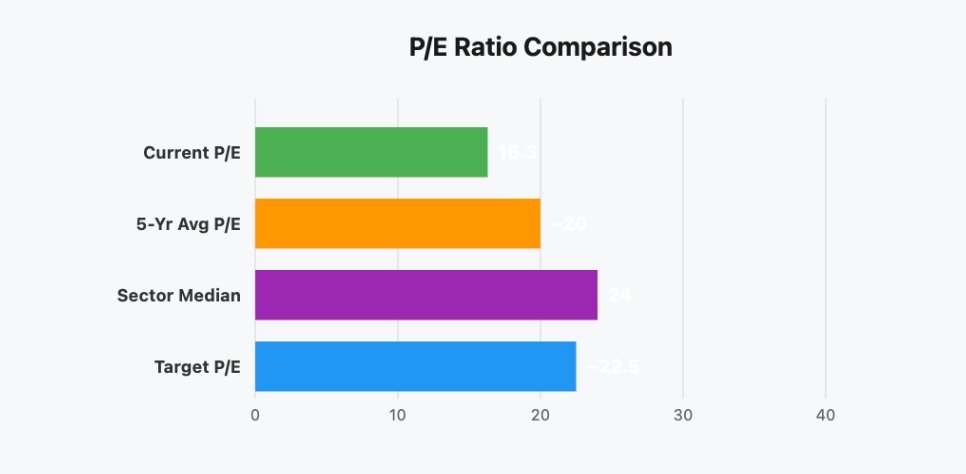

At ₹428, you’re paying a P/E ratio of 16.3 times earnings. Compare that to the five-year average P/E (which has typically been higher) and the sector median of around 24 times - you’re getting a 30% discount to peers for a company that’s actually growing faster.

The P/B ratio is 3.0 times book value of ₹144 per share. For a company generating 21% return on equity and 24% return on capital employed, that’s not expensive. These ROE and ROCE numbers mean management’s good at turning capital into profits.

EPS growth has been strong - up from ₹4.87 in FY22 to ₹24 now. That’s nearly 5x in three years. If they can maintain even half that pace, the stock’s undervalued.

Dividend yield is modest at 0.7%, but that’s fine when a company’s reinvesting for growth. Their payout ratio is only 13%, leaving plenty for expansion.

Where This Goes Long-Term

Over the next 10-15 years, I’d expect 14-18% annual returns. Here’s why: India’s aluminum industry is growing as infrastructure and manufacturing expand. More aluminum production means more demand for aluminum fluoride. The government’s push for Make in India and infrastructure spending should keep aluminum demand strong.

They’ve got the Jordan JV that could start contributing meaningfully. Management’s also shown they’re willing to invest smartly - the solar plant cut energy costs, the plant expansion increased capacity from 3,500 to 15,000 metric tons.

Promoters hold about 60% with zero pledging, which shows confidence. They’re not selling out.

The risks? Raw material availability could be an issue if fertilizer plants change processes. Aluminum prices are cyclical, so if smelters cut production, demand for their product drops. Competition could emerge, though their “waste to wealth” model and established relationships give them an edge. Regulatory changes around industrial effluents could affect operations.

But the upside looks bigger than the downside here. The Indian chemicals sector is benefiting from global supply chain shifts, and specialty chemicals have good pricing power. With margins steady at 20%, efficient operations, and growing capacity, this small-cap has room to run.

Subscribe to unlock the stock name.