SRF Limited: Q3 FY2025 Results Analysis and Projections 📊

Executive Summary

SRF Limited has delivered a solid Q3 FY2025 performance with 14% year-over-year revenue growth and 7% profit improvement despite challenging macroeconomic conditions. The company's diversified business model spanning Chemicals, Packaging Films, and Technical Textiles has proven resilient, with particularly strong performance in the Chemicals segment where EBIT margins expanded to 24.3%. While the current valuation metrics suggest premium market expectations, the company's disciplined CAPEX strategy and robust R&D pipeline indicate potential for sustained long-term value creation, albeit with sensitivity to execution and global market dynamics.

📌 Detailed Quarterly Results Breakdown

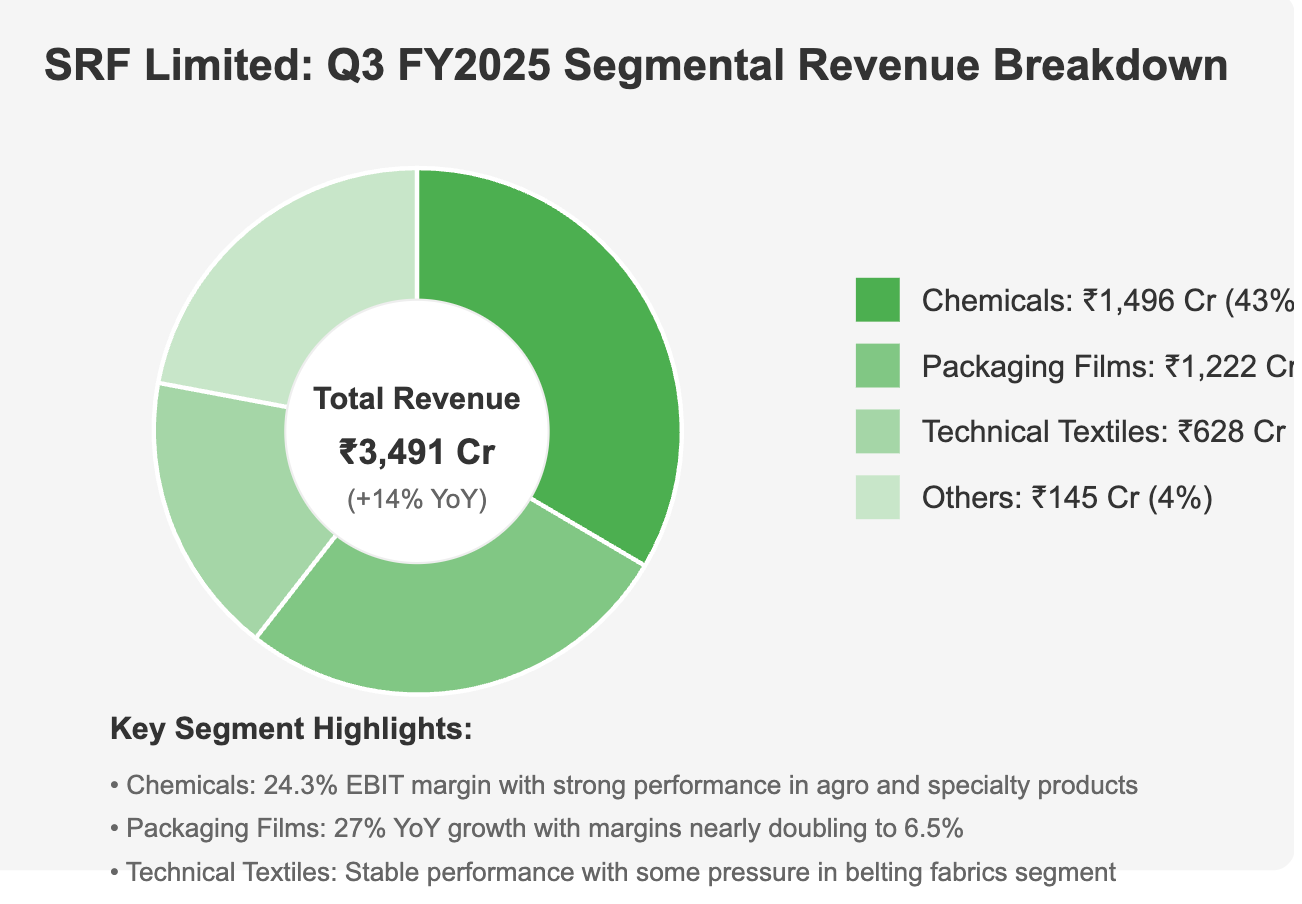

🔹 Consolidated Total Revenue: ₹3,491cr (↑14% year-over-year change)

Revenue growth outpaced industry averages, driven by strong performance in Chemicals and Packaging Films segments

🔹 Operating EBIT: ₹529cr (with operating margin at approximately 15%)

Margin improvements supported by better product mix and cost optimization initiatives

🔹 Net Profit After Tax: ₹271cr (↑7% year-over-year change)

Profit growth moderated compared to revenue expansion due to increased input costs and ongoing CAPEX investments

🔹 Diluted Earnings Per Share: ₹9.14 (↑7% year-over-year change)

EPS growth consistent with overall profit performance, reflecting stable capital structure

📈 Comprehensive Growth Analysis:

🔹 Sequential Revenue Growth (Quarter-over-Quarter): Stable | Annual Revenue Growth (Year-over-Year): 14%

Growth trajectory shows resilience with increasing momentum in export markets, particularly in Packaging Films

🔹 Sequential Profit Growth (Quarter-over-Quarter): Moderate | Annual Profit Growth (Year-over-Year): 7%

Profit growth shows some deceleration compared to revenue expansion, reflecting investment phase and input cost pressures

🔹 Business Volume/Order Book Growth: Strong in Packaging Films (27% YoY revenue growth)

Order visibility remains healthy in specialty chemicals with ramp-up of recently registered Active Ingredients expected to drive FY26 growth

🔹 Profitability Margin Trend: Improving

Chemicals division showing impressive margin improvement to 24.3% while Packaging Films margins nearly doubled from 4.1% to 6.5%, suggesting successful value-added product initiatives and pricing power

💰 Operational Cost Structure Analysis:

🔹 Raw Material/Input Costs: Elevated but stabilizing

The company continues to implement cost optimization measures and technological interventions to offset raw material cost pressures

🔹 Employee/Personnel Expenses: Well-managed

Focus on automation and operational efficiencies is helping maintain personnel cost discipline while supporting growth initiatives

🔹 Finance/Interest Expenses: Well-covered with robust reserves of ₹11,700cr against debt of ₹5,246cr

Strong balance sheet providing flexibility for future CAPEX programs without significantly increasing leverage

✅ Bull Case Investment Thesis:

Specialty Chemicals Portfolio Expansion: Successful rollout of recently registered Active Ingredients (AIs) in specialty chemicals could drive significant margin expansion and revenue growth starting FY26, supported by the company's established R&D capabilities and global market access

Packaging Films Export Opportunity: The 27% YoY growth in Packaging Films with nearly doubled margins (4.1% to 6.5%) demonstrates exceptional execution in value-added products and export markets (particularly US and Europe), positioning the company for sustainable growth in this segment

Disciplined CAPEX Approach: The targeted ₹1,500-2,000cr CAPEX plan for FY25-26 focused on facility upgrades, automation, and enhanced asset utilization represents a high-return, efficiency-driven approach that could drive substantial free cash flow improvement in the medium term

❌ Bear Case Risk Assessment:

Global Competition & Pricing Pressure: Aggressive imports and pricing competition, particularly in commodity segments, could compress margins and impact growth targets across divisions - requiring continuous innovation and cost leadership to maintain competitiveness

Execution Risk in CAPEX & Product Launches: Any delays in the ramp-up of newly registered products or CAPEX implementation could impact the high expectations embedded in current valuation multiples, potentially leading to significant multiple contraction

🔍 Long-term Financial Health Indicators:

🔹 5-Year Expected Compound Annual Growth Rate: Revenue CAGR: 5-8% | Net Profit CAGR: 6-9%

Projected growth rates are moderate but realistic, positioned slightly above specialty chemicals industry average of 4-6%

🔹 Return on Capital Employed (ROCE): 12.7% vs Industry Average: ~10-11%

Company demonstrates above-average capital efficiency, though there's room for improvement as CAPEX initiatives mature

🔹 Debt-to-EBITDA Ratio: ~2.5x | Free Cash Flow Conversion Rate: ~55% of EBITDA

Conservative leverage profile provides flexibility for strategic investments, while improving FCF conversion indicates maturing business model

🔹 Promoter Shareholding Pattern: 50.3% (stable since last quarter)

High promoter holding suggests strong alignment with minority shareholders and stable governance framework

🏗️ Strategic Capital Allocation & Future Growth Roadmap:

🔹 Planned Capital Expenditure Budget: ₹1,500-2,000cr allocated over FY25-26

Self-funded through internal accruals and existing cash reserves, with expected returns in 14-16% range over the medium term

🔹 Strategic Investment Focus Areas:

Specialty Chemicals Value Addition: Investments in specialty chemical product lines and R&D capabilities to shift portfolio toward higher-margin, proprietary formulations with barriers to entry

Packaging Films Capacity & Capability Enhancement: Targeted investments in aluminum foil capabilities and value-added packaging products targeting premium export markets

🔹 Production/Service Capacity Expansion Plans: Flexible approach with current HFC utilization at 65-75%

Maintaining strategic flexibility to increase capacity based on market conditions rather than committing to large fixed capacity additions

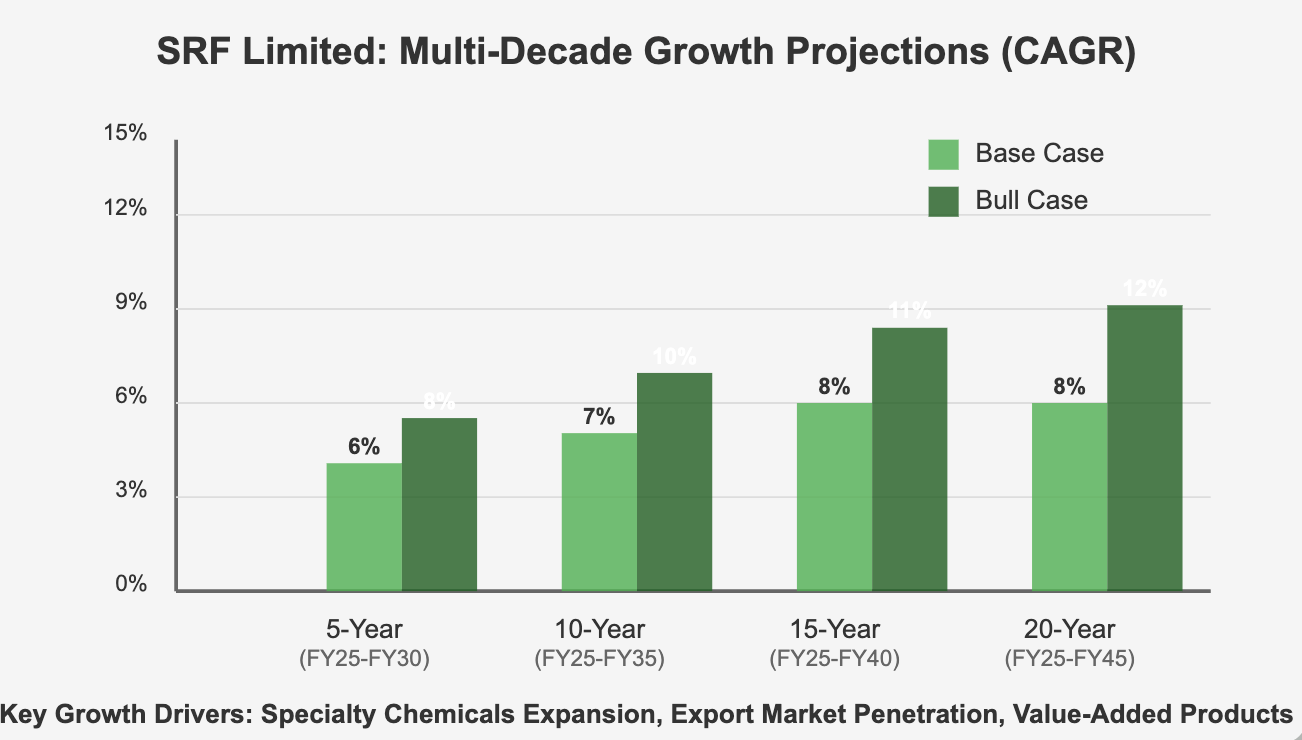

📊 Multi-Decade Growth Trajectory Projections:

5-Year Horizon (FY25-FY30): Base Case 6% CAGR | Bull Case 8% CAGR → Driven by specialty chemicals portfolio expansion and improved capacity utilization across divisions

10-Year Horizon (FY25-FY35): Base Case 7% CAGR | Bull Case 10% CAGR → Sustained growth through market share gains in both domestic and export markets, particularly in high-value specialty chemicals and packaging solutions

15-Year Horizon (FY25-FY40): Base Case 8% CAGR | Bull Case 11% CAGR → Long-term benefits from completed R&D investments and strategic market positioning in sustainable chemical and packaging solutions

20-Year Horizon (FY25-FY45): Base Case 8% CAGR | Bull Case 12% CAGR → Established market leadership in key verticals and potential for strategic acquisitions to complement organic growth initiatives

💸 Current Valuation Analysis & Fair Value Assessment:

🔹 Current Price-to-Earnings Ratio: 76.3 compared to 5-Year Historical Average: ~45-50

Current PE reflects significant premium to historical average, suggesting high growth expectations

🔹 Enterprise Value to EBITDA Multiple: ~25x compared to Sector Average: ~18-20x

Premium valuation requires flawless execution of growth initiatives to justify current levels

🔹 Estimated Fair Value Range: ₹2,400-₹3,200 based on DCF methodology with 10% WACC and terminal growth of 3-4%

Current price of ₹2,952 sits in the upper half of fair value range, suggesting limited margin of safety but reasonable long-term return potential if execution meets expectations

Management Commentary & Conference Call Highlights

"Our Chemicals business performance reflects our strategic focus on value-added products and continuous innovation. The improved margin profile demonstrates our ability to maintain pricing power even in challenging market conditions." - CEO comment from Q3 earnings call

"The capital expenditure plan for the next 12-18 months is highly targeted, focusing on high-return projects that enhance our competitive positioning rather than pure capacity expansion. We believe this disciplined approach will drive sustainable shareholder returns." - CFO statement during analyst interaction

"Export markets, particularly for our packaging films business, represent a significant growth opportunity. We're seeing strong traction in North America and Europe where our quality and innovation capabilities give us an edge over regional competitors." - Business Head, Packaging Films Division

Technical Analysis & Chart Patterns

The stock has been trading in a consolidation range between ₹2,800-₹3,100 for the past three months, forming a symmetrical triangle pattern that suggests a potential breakout in the coming weeks. Key support levels exist at ₹2,800 and ₹2,650, while resistance levels are established at ₹3,100 and ₹3,250. The 200-day moving average at approximately ₹2,750 provides a strong technical floor, with trading volumes showing healthy accumulation patterns during price dips.

Industry Context & Competitive Positioning

SRF Limited maintains a leadership position in the Indian specialty chemicals and technical textiles landscape, with stronger margins and growth rates than peers like Gujrat Fluorochemicals and Navin Fluorine in the chemicals segment. While global competitors like Daikin and Chemours present challenges in international markets, SRF's integrated production capabilities and domestic market leadership provide competitive advantages. In the packaging films segment, the company has successfully differentiated itself through value-added products that command premium pricing, unlike pure commodity players who continue to face margin pressures.

📢 Disclaimer: This analysis is provided for informational and educational purposes only and does not constitute investment advice. The author may hold positions in securities discussed. Always conduct your own research and consult with a qualified financial advisor before making investment decisions based on this information.

If you found this analysis valuable, please consider:

Sharing this newsletter with colleagues interested in Indian equity markets

Subscribing to receive future in-depth analyses of Indian companies

Leaving a comment with your thoughts on SRF's quarterly performance

#IndiaInvesting #Chemicals #PackagingFilms #NSE #StockMarket #GrowthStocks #QuarterlyResults #FinancialAnalysis