SN E-Commerce Ventures Share Price Target 2026: Business Model, Growth Drivers & Risks

SECTION I: Investment Thesis & Summary

This company is currently trading at ₹258 on the NSE (ticker will be revealed at the end). Market cap sits at around ₹74,000 Crores. Here’s my call: Hold.

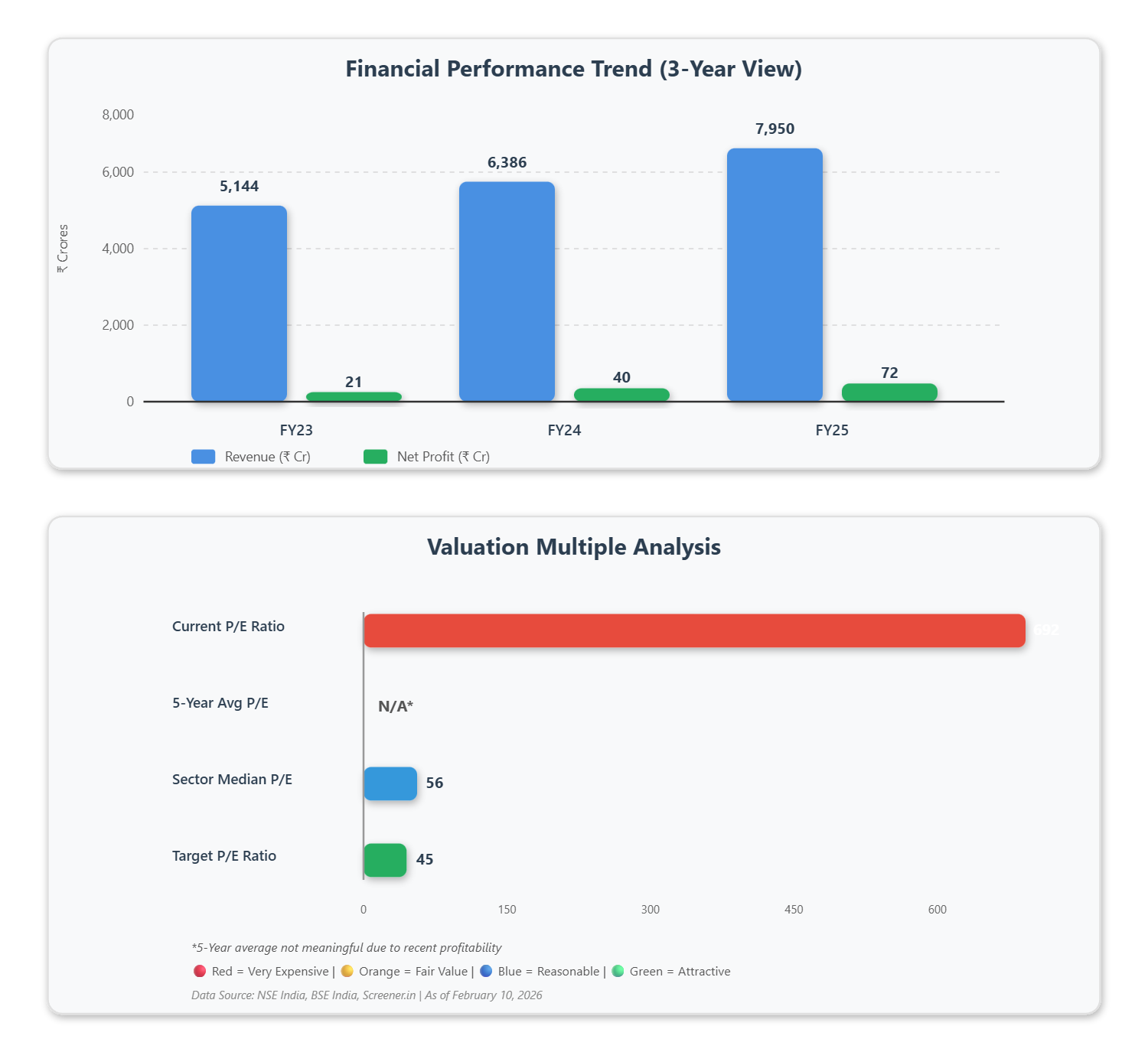

Why? The stock’s expensive - really expensive. We’re talking a P/E ratio above 600. But here’s the thing: this business is finally starting to click. They just posted their best quarter ever, profit more than doubled, and margins are moving in the right direction. The problem is, the market already knows this - the price has run up fast, and you’re paying a massive premium for future growth that needs to actually happen.

Target Price: ₹280 (roughly 8-10% upside from current levels over 12-18 months)

The upside is there, but it’s limited at these valuations. If you already own it, hold on - they’re executing well. If you don’t own it yet, wait for a better entry point. This isn’t a bargain hunting situation; it’s a quality growth story that’s gotten ahead of itself.

SECTION II: Business Model & Operations

Think of this as India’s answer to Sephora meets Zalando, all wrapped into one digital platform. They make money selling beauty products - makeup, skincare, haircare, fragrances - and fashion items through their website, app, and physical stores. The beauty side is the cash cow, bringing in about 75% of total sales. Fashion is the smaller sibling, growing fast but still finding its footing.

Here’s how they actually make money: They buy products from brands (L’Oreal, Estée Lauder, local Indian brands) at wholesale prices and sell them to customers. They also have their own brands - Nykaa Cosmetics, Dot & Key, Kay Beauty - which carry fatter profit margins because there’s no middleman. They’ve built 276 stores across 94 cities, which might sound old-school for an e-commerce company, but it’s smart. People still want to touch lipstick and smell perfume before buying.

Lately, they’ve been busy. In the December quarter, they launched exclusive partnerships - they’re now running Nike’s India website, brought in La Roche-Posay exclusively, and took over Kiehl’s operations in India. They’re also pushing hard on quick delivery - 30 to 120 minutes through something called Nykaa Now, which operates out of 53 rapid stores in 7 cities. The customer base hit 52 million people, up 31% from last year. That’s real traction, not just hype.

Youtube Link:

SECTION III: Historical Financial Review

Over the last three years, revenue has grown at 28% annually - that’s solid, consistent growth. For the most recent twelve months, they did ₹8,830 Crores in sales. Last year’s earnings per share came in at ₹0.23, and for the trailing twelve months, it’s now ₹0.36 - so earnings are moving up.

Let’s talk about what actually changed. Three years ago, they were barely profitable. Operating margins were stuck around 5%. Fast forward to the December 2025 quarter - operating margin hit 8%, the highest it’s ever been. They finally figured out how to make money while growing. Profit jumped 142% year-over-year to ₹63 Crores in Q3 alone.

The company’s been smart with cash. They’re finally generating positive operating cash flow - ₹467 Crores in the last fiscal year after years of burning cash for growth. Debt is manageable at around ₹1,320 Crores, which is less than 10% of market cap. Working capital has improved - they’re turning inventory faster and collecting money quicker.

The beauty business is a machine now. It grew 27% in the December quarter with 29% growth in net sales. Their own brands hit a ₹3,500 Crore annual run rate, growing 48%. Dot & Key alone is approaching ₹1,900 Crores in sales. Fashion is still struggling to make money but getting better - it grew 31% and the losses are narrowing.

SECTION IV: Fundamental Valuation Metrics & Investment Call

Let’s talk numbers, and this is where it gets uncomfortable:

P/E Ratio: 692 - You’re paying ₹692 for every rupee of annual profit. The e-commerce sector average is around 50-60. Even high-growth consumer companies rarely trade above 100. This is stratospheric.

P/B Ratio: 52 - For every rupee of book value, you’re paying ₹52. That’s not a typo. The stock is trading 52 times its book value. Historical average for the company has been around 30-40, and even that was expensive.

ROE: 5% - They’re making 5% return on shareholder equity. That’s low. For context, good companies generate 15-20%. They’re improving (it was 3% two years ago), but 5% doesn’t justify a 52x P/B ratio.

ROCE: 10% - Return on capital employed is 10%, better than ROE but still modest. They’re using capital more efficiently than before, but you’d want to see this above 15% at minimum.

EPS Growth: Strong - This is the one bright spot. EPS went from ₹0.11 (FY24) to ₹0.23 (FY25) to ₹0.36 (TTM). That’s doubling roughly every 18-24 months. If this continues, the valuation starts making sense three years from now.

Dividend Yield: 0% - They don’t pay dividends. All profits get reinvested back into growth.

Here’s the honest take: The stock is absurdly expensive by every traditional metric. A P/E of 692 means the market is betting this company will grow earnings at 40-50% annually for the next 5-7 years straight. That’s a huge ask. But they are executing - margins are expanding, the business model is working, they’re profitable and growing. The problem is, all this good news is already baked into the ₹258 price. You’re not getting a discount here; you’re paying full price for perfection.

SECTION V: Long-Term Outlook & Risk Assessment

5-15 Year Return Estimate: 12-18% annually

That’s decent, but not spectacular given the risk. Here’s why I think that range makes sense:

If they can sustain 25% revenue growth for the next 3-4 years (which is what management has been delivering), and if margins expand from 8% to 12-15% over 5 years (totally doable given their scale advantages and owned brands), then earnings could grow at 30-35% annually. The problem is, the stock already trades at 692 times earnings. Even if you give them credit for perfect execution, the P/E will need to compress to 40-50 times (still expensive but more reasonable) for the math to work.

So your returns come from two things: (1) earnings growth of 30-35%, and (2) multiple compression that wipes out half of that gain. Net result: 12-18% returns if everything goes right.

Here’s what management is planning: They’re opening more stores - targeting 300+ by next year. They’re building out their own brands aggressively, which should push gross margins from 45% to 50%. They’re investing heavily in tech and quick commerce. Capex has been around ₹200-250 Crores annually, most of it going toward new stores and warehouses. No buybacks, no dividends - all cash goes back into growth.

Promoters still hold 52%, which is good. They’ve been selling tiny amounts (down from 52.4% three years ago to 52.1% now), but nothing alarming. FII ownership is 12.5%, and DIIs are at 25% - institutional ownership is strong and growing.

Now the risks - and there are several:

Valuation Risk - This is the big one. At 692 P/E, any stumble kills the stock. If they miss even one quarter’s expectations, you could see a 20-30% correction overnight.

Competition - Amazon is pushing Beauty hard. Flipkart isn’t sleeping. Quick commerce players like Blinkit and Swiggy Instamart are eating into the convenience angle. Tata’s getting aggressive with their omnichannel play. The moat here isn’t wide.

Fashion Profitability - Their fashion business is still losing money. It’s getting better, but it’s been a drag for years. If they can’t fix this in the next 2 years, it becomes a problem.

Execution Risk - They need to keep growing at 25%+ while expanding margins. That’s threading a needle. Most companies can do one or the other, not both simultaneously.

Regulatory - E-commerce rules in India keep changing. FDI limits, data localization, seller requirements - any of these could hurt the business model.

Working Capital - They’ve improved to 30 days of working capital, but e-commerce businesses can blow up if inventory doesn’t move or if brands squeeze payment terms.

What’s going right:

India’s beauty market is booming. It’s growing at 12-15% annually, and online penetration is still only 10-12%. Massive headroom.

Premiumization trend - Indians are trading up to better products. Their average order value keeps growing.

Store economics are working - physical retail is actually profitable for them, unlike many e-commerce players.

Brand portfolio is winning - their owned brands are sticky and high-margin.

The honest conclusion: This is a good company at a crazy price. The business is sound, management is capable, the market opportunity is real. But you’re paying for 5-7 years of perfect execution upfront. If they deliver, you’ll make 12-18% a year, which is fine. If they slip, you’ll lose money fast because there’s no margin of safety.

For existing holders: Hold tight. The execution is there. For new buyers: Be patient. Wait for a 15-20% pullback, or wait for earnings to catch up to the valuation.

COMPANY NAME: FSN E-Commerce Ventures Limited (NYKAA)