The Market Calls It Boring. The Numbers Call It a Compounder.

Everyone chases the next multibagger. No one looks at the stock that’s already compounding quietly for two decades.

This company controls bathroom shelves across 500 million households. Yet the market treats it like a slow, boring FMCG play.

Margins are expanding. International revenue is growing faster than domestic. And institutional buying is at a multi-year high.

The boring ones are often the best ones. Keep reading.

Section 1

A capital-light, brand-moat business re-rating on international growth and rural recovery.

Section 2

What the market is missing

The market sees it as a saturated domestic FMCG play. That’s the wrong lens entirely.

Nearly 25–30% of revenue now comes from international markets — Bangladesh, Vietnam, South Africa, the Middle East. These geographies are growing at double-digit rates while domestic India grows at high single digits.

Second, digital-first brands and D2C entrants are eating into legacy FMCG players. But this company’s moat isn’t distribution — it’s brand equity built over 30+ years. That doesn’t erode in a quarter.

Third: gross margin recovery. Input costs (copra, vegetable oils) have softened significantly. The company is running at near-peak margins. Most analysts haven’t fully adjusted their models for this yet.

Youtube Link:

Section 3

The business, simplified

Think of brands you reach for without thinking. Hair oil. Edible oil. Skin care. Value-added foods. This company owns the category leaders in each.

Who pays them? Hundreds of millions of Indian households — middle-class and aspirational. Plus consumers across 25+ international geographies.

Why is it sticky? Because consumers don’t switch hair oils. They’re taught by their mothers which brand to buy. Habit-based purchasing is the strongest moat in FMCG — no algorithm can disrupt it.

Distribution reach: 5+ million outlets in India. That’s a channel advantage built over decades and nearly impossible to replicate at cost.

Section 4

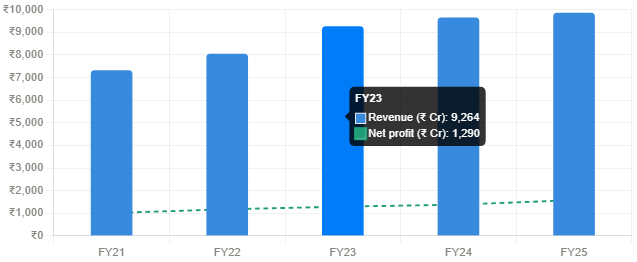

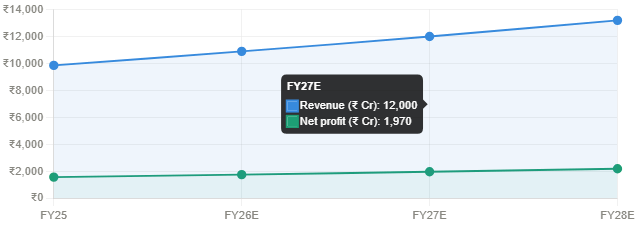

Financial momentum

Revenue has compounded at ~8–10% CAGR over five years. Profit growth has been sharper — closer to 12–14% — driven by margin expansion as commodity costs eased.

EBITDA margins hover in the 19–21% range. For an FMCG company with heavy brand investment, that’s a strong number. Return on equity consistently above 35%.

The balance sheet is nearly debt-free. Free cash flow is generous. And the company returns cash to shareholders through buybacks and dividends reliably.

Section 4.5 — Pattern interrupt

This is not just a hair oil company.

It’s a household habit company.

Habits don’t show up in P&L. They show up in repeat purchase rates, decade after decade. That’s the real asset — and it’s not on the balance sheet.

Section 5

Key triggers to watch

Rural consumption recovery — monsoon and wage growth driving FMCG volume upticks

Copra price correction — direct uplift to gross margins in the hair oils segment

International markets inflecting — Bangladesh and Vietnam scaling meaningfully

Foods portfolio gaining traction — category expansion beyond core hair care could re-rate the stock

Premiumisation — consumers trading up to value-added products, expanding revenue per household

Section 6

Smart money signal

Domestic institutional holdings have increased steadily over the last four quarters. FII ownership remains robust — a sign that global EM funds view this as a quality compounder, not just a domestic story.

Promoter stake has been stable. No pledging. That matters more than people realize — it signals confidence in the business without desperation for liquidity.

Stock has been quietly consolidating near key support levels, even as broader FMCG has underperformed. That kind of resilience usually precedes the next leg up.

Section 7

Risks — no sugarcoating

Copra inflation can reverse fast — a 20% spike in raw material costs compresses margins sharply

Valuations are not cheap — stock trades at 45–50x earnings; any growth disappointment is punished hard

Currency risk in international markets — Bangladesh and Vietnam earnings can get eroded by FX moves

Foods portfolio is still a bet, not a proven business — scaling it profitably is an open question

D2C disruption in personal care is real — younger consumers are experimenting, and legacy brands must respond

Section 8

Final verdict

Here’s the honest pitch.

This isn’t a 10x story in two years. But it might be a story where you look back in five years and wish you’d simply held it.

Branded consumer businesses with 30+ years of household penetration, expanding international footprint, nearly debt-free balance sheets, and consistent free cash generation are rare. Genuinely rare.

The market is waiting for “something to happen” before it gets excited. That’s exactly the window. Because by the time everyone agrees it’s a good buy, the price will have already moved.

Track this one. Closely.