Shakti Pumps Q3 FY25 – Strong Performance & Massive Growth Ahead!

📢 Shakti Pumps (India) Limited (NSE: SHAKTIPUMP | BSE: 531431)

📢 Shakti Pumps (India) Limited has delivered an outstanding Q3 FY25 performance, with robust revenue growth, stellar profit expansion, and a solid future growth trajectory.

This quarter, the company reported a record-breaking surge in revenue, EBITDA, and profit, driven by strong government orders, increased exports, and capacity expansions. Let's break down the numbers, analyze future growth strategies, and project where Shakti Pumps is headed.

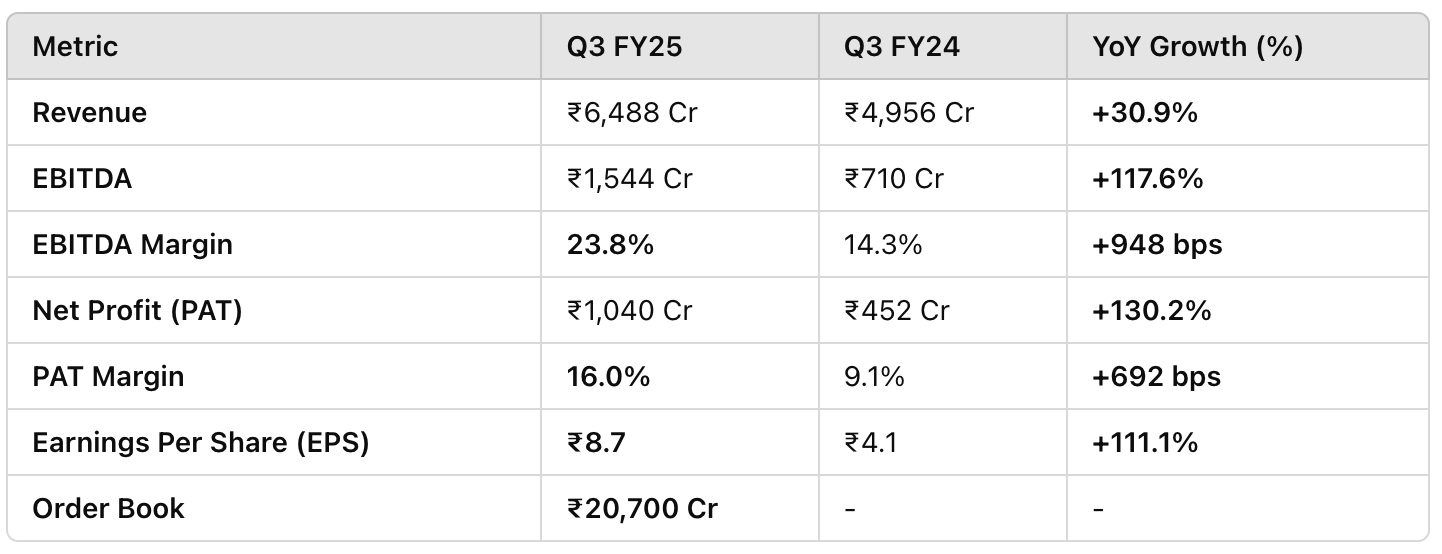

📊 Q3 FY25 Financial Performance – Key Metrics

🚀 Strong Year-on-Year (YoY) Growth Across All Financial Metrics

✅ Shakti Pumps has more than doubled its profitability while maintaining industry-leading margins!

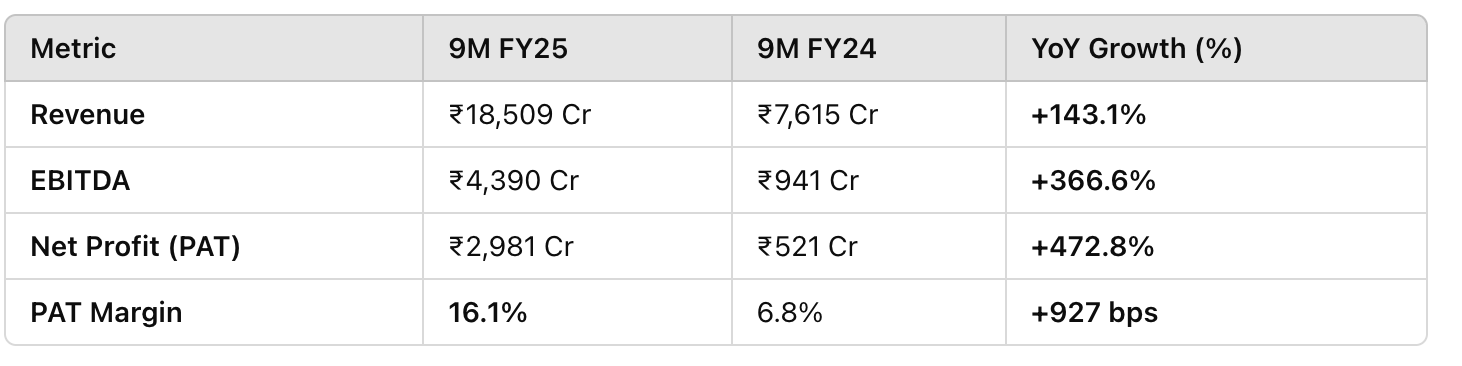

📅 9M FY25 (April-Dec 2024) Performance – Strong Momentum Continues

🔎 Key Takeaways:

Revenue surged by 143.1% in 9M FY25 due to higher government orders and export growth.

PAT skyrocketed by 472.8%, showcasing improved operational efficiencies and cost control.

EBITDA margins expanded to 23.7% (+1136 bps YoY), signaling strong profitability.

📈 Growth Drivers & Future Expansion Plans

🔋 1. Massive Order Book – ₹20,700 Cr Pipeline

Shakti Pumps has a robust order backlog of ₹20,700 Cr (inclusive of GST) to be executed over the next year.

Key Orders in Q3 FY25:

Maharashtra (Magel Tyala Saur Krushi Pump Scheme) – ₹7,543 Cr (25,000 solar pumps).

Haryana (HAREDA) – ₹1,163.6 Cr (3,174 solar pumps).

Other Government & Export Projects – ₹4,782 Cr.

🔎 What This Means?

This ensures strong revenue visibility for FY25-FY26, with continued momentum from government projects and international contracts.

🌞 2. Expansion into Solar Rooftop Business

PM Surya Ghar: Muft Bijli Yojana (₹75,000 Cr government outlay) is a major catalyst.

Solar rooftop demand is booming, creating new revenue streams.

Shakti Pumps is positioned to dominate this segment, leveraging its existing distribution network and expertise.

⚡ 3. Electric Vehicles (EV) – New Growth Frontier

Shakti EV Mobility Pvt. Ltd. (subsidiary) is focusing on EV motors, controllers, and charging stations.

₹114.3 Cr investment approved over 5 years for EV expansion.

Recently granted patent for Permanent Magnet Rotor, boosting EV motor efficiency.

Already supplying EV parts to OEMs and expanding into two-wheeler & three-wheeler segments.

🔎 Why This Matters?

Shakti Pumps is diversifying beyond solar pumps into high-growth EV components, adding a new revenue stream for the future.

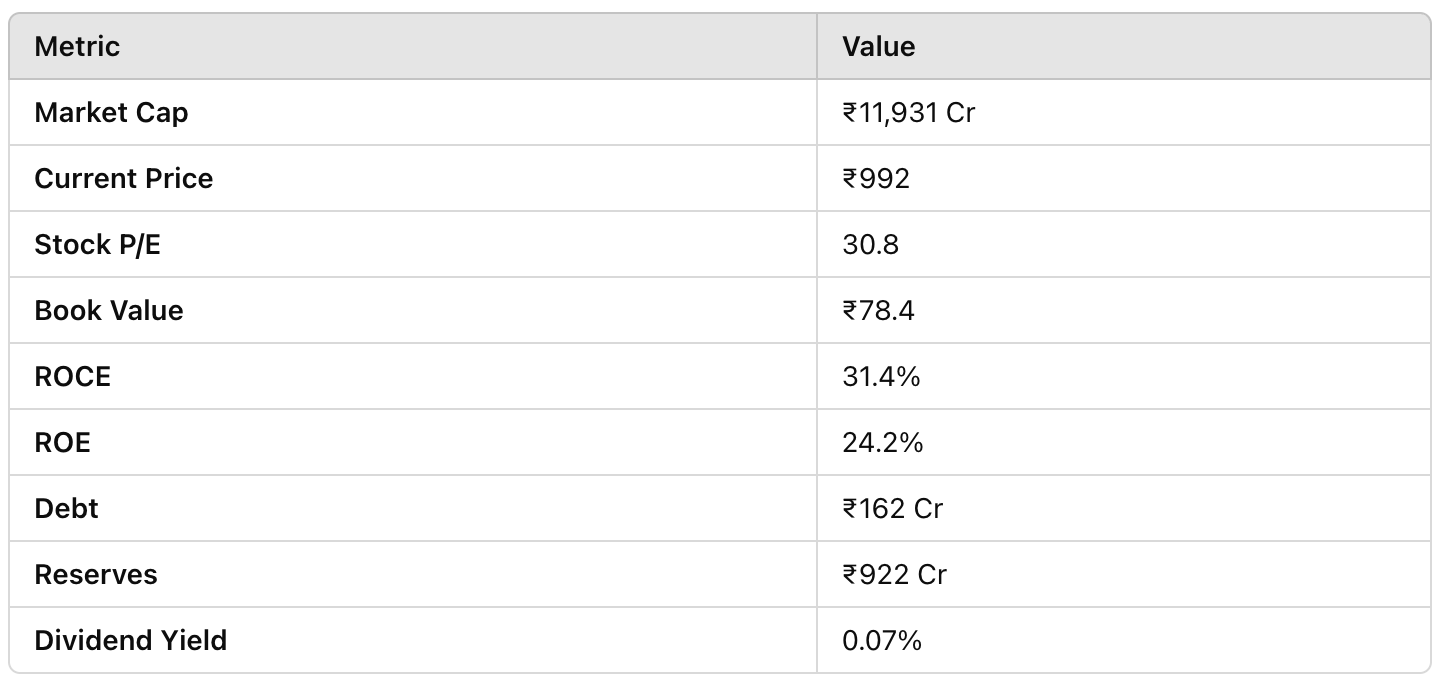

💰 Financial Strength & Valuation

📌 Key Financial Ratios

📊 Shakti Pumps is trading at a reasonable valuation considering its strong earnings growth and improving margins.

🔮 Stock Target Price Projection

Given the 161% sales growth & 614% profit growth, a P/E multiple of 35-40x is justified.

12-Month Target Price: ₹1,300 – ₹1,500 🚀

Upside Potential: +30% - 50% from current levels.

🚨 Key Risks to Watch

⚠️ Government Dependency – Revenue heavily depends on PM-KUSUM and solar subsidies.

⚠️ Raw Material Costs – Rising copper, stainless steel, and semiconductor prices could impact margins.

⚠️ Working Capital Constraints – High order execution requires efficient cash flow management.

⚠️ Competition from Domestic & Global Players – New entrants in solar & EV segments could impact market share.

🏆 Final Verdict: Strong Buy with a Long-Term Growth Story

✅ Why Invest in Shakti Pumps?

✔ Massive Revenue Growth (161% YoY).

✔ High Order Visibility (₹20,700 Cr backlog).

✔ Expansion into Solar Rooftop & EV Motors.

✔ ROE of 24.2% & Strong EBITDA Margins (23.8%).

✔ Reasonable Valuation with ₹1,300-₹1,500 Price Target.

🚀 Shakti Pumps is a compelling growth stock, well-positioned to benefit from the renewable energy boom and EV revolution.

📢 What’s Your Take?

Do you think Shakti Pumps will continue its strong growth trajectory? Share your thoughts in the comments!

📩 Subscribe for More In-Depth Market Insights!

📌 Disclaimer: This article is for educational purposes only and is not investment advice. Always do your own research before making financial decisions.