SBC Exports Limited: Valuation Disconnect in a High-Growth, High-Debt Textile Play

INVESTMENT THESIS & SUMMARY

This stock’s had a crazy run, up 119% in the last year. But when you look under the hood, it’s trading at nearly 49 times earnings and 21 times book value. The business is growing fast, sure, but the valuation’s gotten way ahead of itself. Plus, promoters have been steadily selling down their stake, which never feels great.

BUSINESS MODEL & OPERATIONS

The company makes money through three main streams. First up is garment manufacturing and trading - they started out trading handmade carpets and handicrafts in Mirzapur back in 2011, but they’ve since built out their own manufacturing setup with dyeing, printing, stitching, and packaging facilities. They’re making hosiery garments, readymade apparel for men, women, and kids.

Second revenue stream is manpower supply services. They’ve been landing some solid government and institutional contracts lately - a ₹10.77 crore deal with IIT Jodhpur, ₹3 crore with MDI Gurgaon, and other smaller contracts with government bodies. This business is actually growing faster than the garment side.

Third, they’ve got a travel business through their subsidiary Mauji Trip Limited. It’s the smallest piece of the pie, but they’re positioning it as an online travel portal offering customizable packages across India.

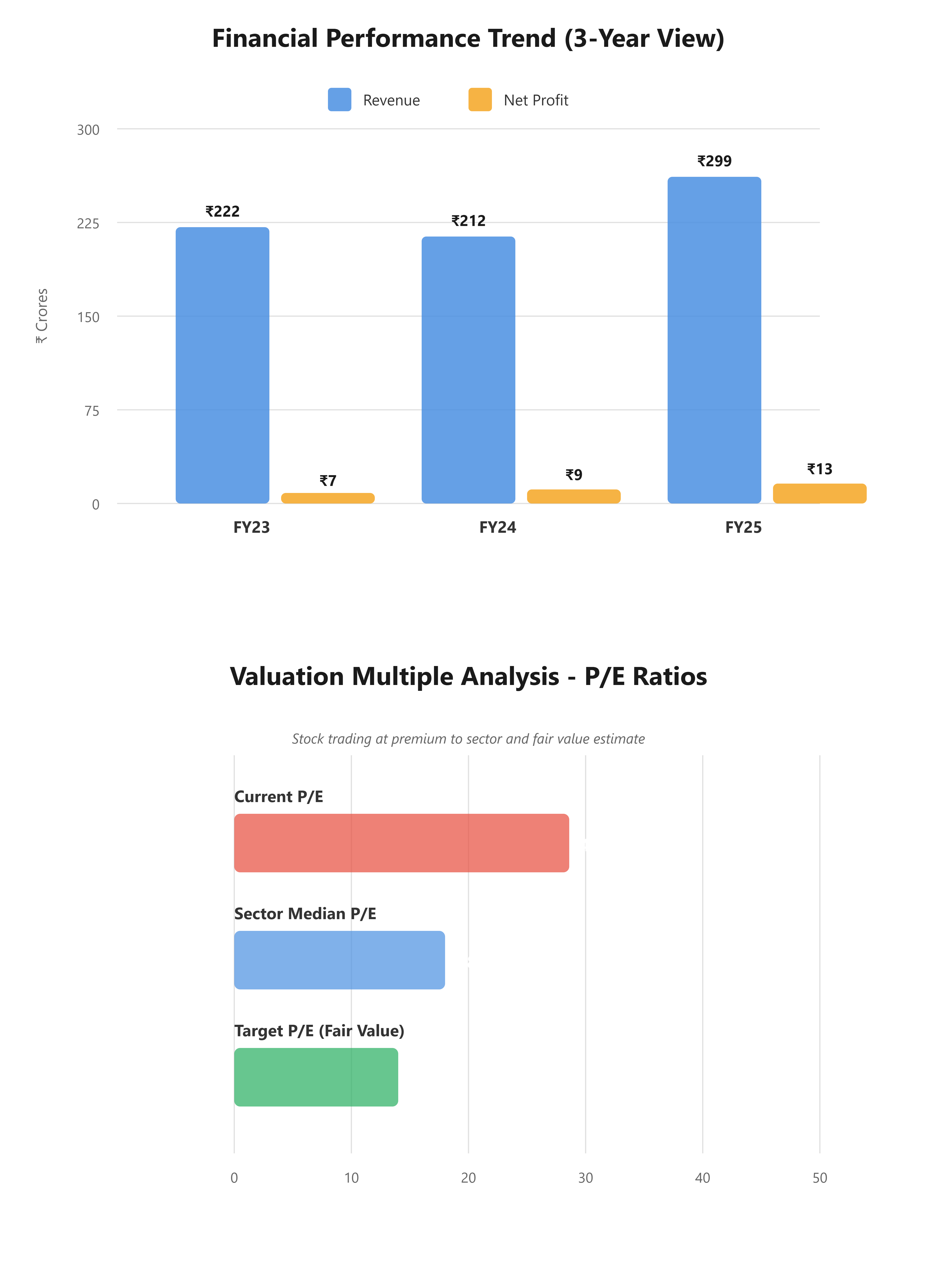

The latest quarter showed revenue of ₹70.5 crores, up 41% from last year. They also just bagged a ₹7 crore export order from Dubai for garments. The manpower services segment is really picking up steam with multiple government contracts coming through.

Youtube Link:

HISTORICAL FINANCIAL REVIEW

Over the last three years, revenue grew at 13% annually - decent but not spectacular. What’s more interesting is the profit growth, which clocked 52% per year. That’s a massive jump. Last twelve months, they made earnings of ₹0.63 per share.

But here’s where it gets messy. The company’s been burning cash from operations - negative ₹69 crores in FY25. They’re funding growth through debt. Total borrowings jumped from ₹53 crores in FY24 to ₹136 crores in FY25, and it’s now sitting at ₹199 crores. That’s a debt-to-equity ratio of 2.82 times - really high.

Interest costs are eating into profits. In the latest quarter, interest expense hit ₹3.7 crores, up 55% from the previous quarter. That’s the highest it’s ever been. The cash conversion cycle has stretched to 152 days, meaning money’s stuck in working capital for five months.

On the positive side, margins are improving. Operating margin in the latest quarter was 11.3%, and they’re showing they can scale without completely destroying profitability.

FUNDAMENTAL VALUATION METRICS & INVESTMENT CALL

Let’s talk numbers. The stock’s trading at a P/E of 48.6 - that’s expensive by any measure. The five-year average P/E would be lower, but this company’s only been listed since late 2021, so historical comparison is limited.

P/B ratio is 20.7. You’re paying ₹20 for every rupee of book value. That’s steep.

ROE is strong at 24.4% - they’re making good returns on shareholder money. ROCE is 17%, which is solid but not exceptional given the debt load.

EPS growth has been strong - up from ₹0.19 in FY24 to ₹0.63 in the trailing twelve months. That’s real earnings growth, though helped by a low base.

No dividend. They’re keeping all cash to fund operations and pay down debt.

The problem is simple - the stock’s priced for perfection. You’re paying 49 times earnings for a company that’s heavily indebted and burning operating cash. Even if they keep growing at 30-40% annually, you’d need the stock to stay expensive for years to justify today’s price. Any hiccup - slower growth, margin pressure, debt issues - and this could correct hard. Fair value is probably closer to ₹22-24, implying 25-30% downside from here.

LONG-TERM OUTLOOK & RISK ASSESSMENT

Looking out 5-15 years, if everything goes right, you might see 8-12% annual returns from current levels. That’s assuming the company can maintain 25-30% revenue growth for 3-4 years, gradually improve margins, and pay down debt without hitting any major roadblocks.

The opportunity is real. Government manpower services is a growing market, and they’re winning contracts. The export business is getting traction. If they can keep landing ₹5-10 crore orders regularly, revenue visibility improves.

But let’s talk risks, because there are plenty. First, promoters sold their stake from 64% to 50% in just one year. They’ve also pledged 30% of their remaining holding. That’s not confidence-inspiring. When founders are selling, you’ve got to ask why.

Second, the debt situation is concerning. With interest costs jumping 55% quarter-on-quarter and debt at 2.8 times equity, there’s limited room for error. If revenue growth slows or margins compress, servicing this debt becomes a problem fast.

Third, the garment industry is ultra-competitive. Margins are thin, working capital requirements are high, and you’re competing with everyone from big players to small unorganized units. There’s no moat here.

Fourth, they’re not generating operating cash despite growing revenues. That’s a red flag. It means growth is capital-intensive and needs continuous debt or equity funding.

On the positive side, the India story helps. Government spending on services, growing export opportunities, and formalization of the textile sector are tailwinds. If they can crack consistent profitability in their travel business, that’s another potential growth driver.

The sector itself is okay but not great. Textiles and apparel has been struggling, with the sector down 5.5% over the past year while this stock rallied 123%. That divergence can’t last forever.

Bottom line - this is a high-risk, high-debt, richly-valued small-cap. If you own it and you’re sitting on profits, consider booking some gains. If you don’t own it, wait for a better entry point. The business has potential, but the stock’s gotten way ahead of reality.

---COMPANY NAME REVEALED---

SBC Exports Limited