68% Revenue Growth. Flat Profits. And the Market Still Misses the Real Story

+68%

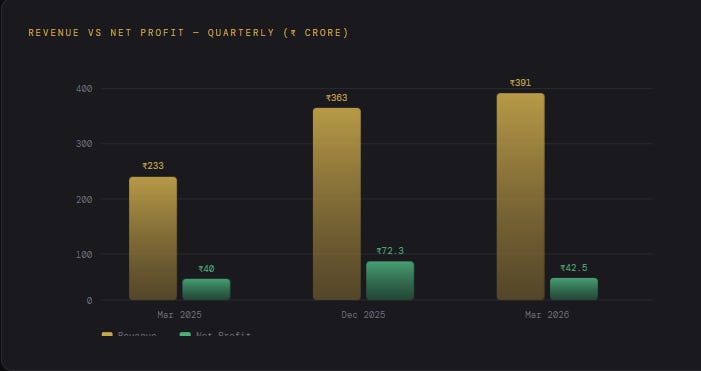

Revenue grew 68% year-on-year. Sales crossed ₹391 crore this quarter.

And yet — net profit grew just 6%. Most investors would scroll past. That’s exactly the mistake.

Because the margin squeeze isn’t a problem. It’s a setup. Here’s what’s really happening.

01 · Quick Snapshot

Numbers at a Glance

💡 One-Line Insight: A globally scarce specialty product, Forest-sourced raw material moat, Fortune 500 clientele — and the market still hasn't priced in West Africa + Brazil.

02 · What The Market Is Missing

The Market Is Ignoring This for the Wrong Reasons

Why it’s being ignored

On the surface — a small-cap company from Raipur, Chhattisgarh. Dealing in seeds and fats. No glamour. No buzzy sector label. The stock shed over 14% from its 52-week high. Retail investors walked away.

What’s actually misunderstood

This company extracts specialty fats and butters from Sal, Mango kernel, Kokum, Shea, and Mowrah seeds — forest-derived, naturally scarce, globally irreplaceable ingredients.

These fats are the primary substitute for cocoa butter — called Cocoa Butter Equivalents (CBE). When cocoa prices hit multi-decade highs (they did in 2024–25), every chocolate maker on earth scrambles for CBE. This company is one of just a handful of suppliers globally.

The margin compression you see in Q4 FY26? That’s the cost of adding 25,000 TPA fractionation capacity and setting up 8 new subsidiaries across West Africa, UAE, and Brazil. It’s not margin erosion. It’s infrastructure investment.

Youtube Link

03 · Business Simplified

What This Company Actually Does

What they do: They source seeds — Sal, Mango, Shea, Kokum — from forest tribals across Central India. They process these seeds into exotic butters, specialty fats, and oils. They then sell these to food, chocolate, confectionery, and cosmetics companies worldwide.

Who pays them: Fortune 500 companies in the chocolate and confectionery space. Premium cosmetics brands. Industrial food manufacturers. The customer base is premium, global, and sticky — because these ingredients are formulation-critical. You can’t just switch supplier midway through a chocolate recipe.

Why it’s sticky: The raw material is forest-sourced — supply is naturally capped. The processing is specialized — not easily replicated. And the customer relationships are long-term supply contracts. Once you’re embedded in a Nestlé or Mondelēz supply chain as a CBE supplier, you don’t get replaced easily.

The West Africa angle — the one nobody’s pricing in

Shea trees grow only in a specific belt across West Africa. By setting up subsidiaries in West Africa, this company is moving closer to the raw material source — controlling supply, not just processing. That’s vertical integration at a global scale. From a company headquartered in Chhattisgarh.

04 · Financial Momentum

The Numbers Behind the Story

Revenue trend: Sequential growth every quarter. ₹233 Cr → ₹363 Cr → ₹391 Cr. The 68% YOY jump is not a blip — it reflects a structural shift in scale as new capacity came online.

Profit trend: Net profit was flat QOQ (₹42.5 Cr vs ₹40.0 Cr YOY), but dropped sharply from ₹72.3 Cr in Dec 2025. That Dec quarter was exceptional — high volume + high realizations. The Mar 2026 quarter absorbed higher operating costs from the new plant ramp-up.

Margins: EBITDA margins compressed from ~28.6% (Dec 2025) to ~21.6% (Mar 2026) Compressing. This is the critical watch point. If margins recover as the new capacity utilisation improves, the earnings power of this company is substantially higher than what the P&L currently shows.

📊 Growth Snapshot

This is not just a fats business.

It's a forest-to-Fortune 500 control business.

Whoever controls the seed-to-CBE pipeline

controls global chocolate economics.

05 · Key Triggers

What Could Move This Stock

Margin Recovery: If EBITDA margins return to 26–28% as new capacity utilisation improves, EPS could jump 40–60% without any revenue growth.

Cocoa Price Stay Elevated: Every ₹100/kg rise in cocoa prices makes CBE more attractive. This company is a direct beneficiary of sustained global cocoa disruption.

West Africa Subsidiaries Go Live: Moving procurement to source dramatically lowers raw material costs and creates first-mover advantage in shea supply.

QIP / Capital Raise Execution: Board recently approved fundraising via QIP. If deployed toward capacity expansion rather than debt, this is a multiplier event.

Entry into Brazil Market: Brazil is a growing confectionery hub. A subsidiary there opens Latin American distribution — an entirely new revenue stream.

Organic Certification Upsell: Organic castor, neem, moringa, rice bran oils carry 30–40% premium pricing. Growing portfolio share here expands margins structurally.

06 · Smart Money Signal

What the Quiet Money is Doing

52-Week Range

₹1,060 – ₹1,760

Current Price vs High

~9% below peak

Delivery % (Apr 2026)

~48% — Elevated

Board Action

QIP approved — watching

When delivery percentages stay elevated despite price correcting from highs, it typically signals that buyers are accumulating for the long haul — not trading. The QIP approval signals promoters see a higher valuation ahead. You don’t raise equity capital at low prices if you don’t believe in higher prices coming.

The stock pulled back nearly 27% from its 52-week high. That correction has been bought into — steadily, quietly, without noise.

07 · Risks

Don’t Ignore These

Margin compression is real — EBITDA margins fell from 28.6% to 21.6% in a single quarter. If capacity utilisation doesn’t recover fast, profits stagnate even as revenue grows.

Valuation is stretched — At ~₹1,597 and a P/E of ~87x, there is zero room for earnings disappointment. One bad quarter = sharp de-rating.

Raw material is monsoon-dependent — Sal and Mango kernel collection is seasonal and forest-dependent. A bad harvest season or tribal disruption directly hits supply.

Geopolitical risk in West Africa — Subsidiaries in West Africa face political instability, currency risk, and supply chain disruption beyond the company’s control.

Cocoa price normalisation — If cocoa prices correct sharply, demand for CBE substitutes may soften. The macro tailwind could reverse.

QIP dilution — If the QIP is priced below market or is large, short-term dilution could pressure EPS and the stock price.

08 · Final Verdict

Should You Track This?

Here is what this company actually is — a globally rare, forest-anchored specialty ingredient business supplying the global chocolate economy. Most Indian investors have never heard of it. Most global investors don’t know it exists in India.

The Revenue-Profit gap you saw at the start is not a warning. It’s an investment cycle. Companies don’t build fractionation plants and open subsidiaries in three continents for fun. They do it because they see demand coming that current capacity cannot serve.

If margins recover to even 24–25% in FY27, the earnings power of this business at current revenue run-rates crosses ₹300+ Cr annually. The market cap today prices in none of that upside.

This is a story worth tracking closely. Not blindly chasing — but watching for margin recovery as the entry signal.