Where Global Pharma Comes to Find Its Next Billion-Dollar Molecule

SECTION I — Investment Thesis & Summary

India is quietly becoming the world’s go-to lab for discovering and manufacturing new drugs. This company is right at the center of that story — and the market hasn’t fully caught up to how fast the profits are piling up.

They’ve more than doubled their profit in FY25. Margins are expanding meaningfully. They just cleared a major chunk of debt. And three quarters into FY26, the momentum is only accelerating. At the current price, you’re paying up — this isn’t a “screaming bargain” stock — but you’re paying up for a quality CRDMO business in a sector that’s genuinely at an inflection point.

The stock listed in December 2024 at ₹636. It’s already up 48% from IPO lows. The question is whether there’s more road ahead. The answer, based on how the business is actually running, is yes.

Youtube Link:

SECTION II — Business Model & Operations

Let’s talk about what this company actually does, because it’s not complicated once you understand it.

Global pharma companies — think the big multinationals spending billions on new drugs — don’t do all their chemistry themselves anymore. They outsource drug discovery, development, and manufacturing to specialists. That’s where this company comes in. It’s a CRDMO: a Contract Research, Development, and Manufacturing Organisation. Essentially, it’s a fully integrated science partner for pharma companies that want to find new drugs faster and cheaper.

The business runs in two clear lanes. First, the CRO side — early-stage discovery chemistry, biology services, pharmacokinetics. Companies bring their molecule ideas and this company’s scientists figure out if they work. Second, the CDMO side — once a molecule looks promising, it helps scale up production, from lab bench all the way to commercial manufacturing.

The reason this model is so powerful is the “stickiness.” A pharma client doesn’t switch their chemistry partner mid-program. Once you’re embedded in a molecule’s journey from discovery to commercialisation, you stay for 10–15 years. That’s recurring, high-value revenue with pricing power.

They serve 280+ global innovator pharma and biotech clients. The US and Europe are the dominant markets. Operations span four main manufacturing sites in India — including their flagship Unit IV API facility in Bidar, Karnataka, which just had a major capacity expansion — plus biology labs in Cambridge, Massachusetts and a UK presence.

Recently, they’ve been moving aggressively into high-value niches. A dedicated Peptide Research Centre launched in FY25. The Boston lab was opened as the US hub for their “Eyra” platform, a specialised discovery biology offering. Phase II of Production Block 11 in Bidar was commissioned in Q1 FY26, taking total installed reactor capacity at the site to ~700 KL — the single largest block in their network. These aren’t just press releases; they’re meaningful capacity additions that will drive revenue through FY27 and beyond.

SECTION III — Historical Financial Review

The numbers tell a clean story here — a business that was profitable but barely so, now operating at a different level entirely.

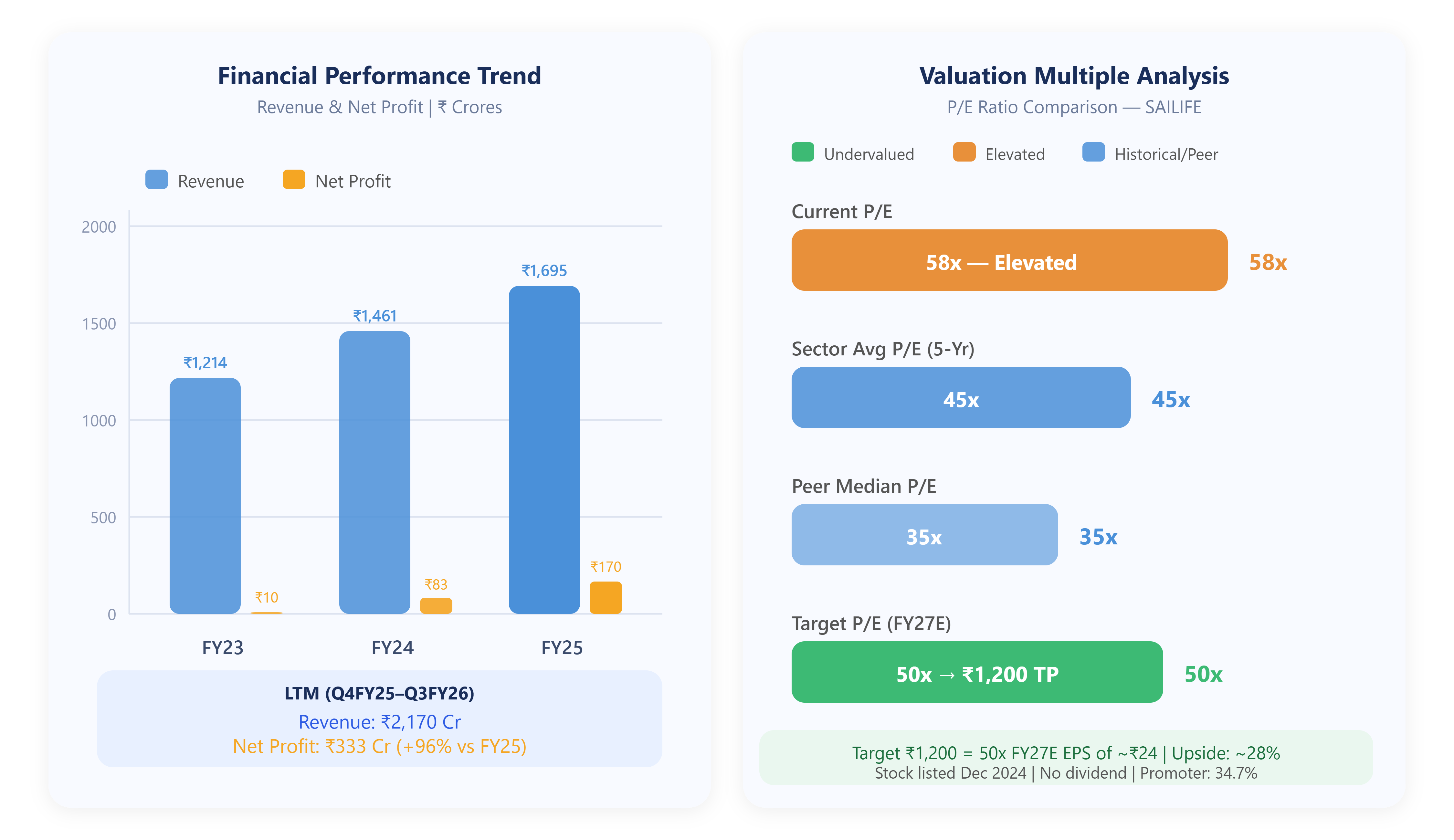

This is a company that went from near-zero profitability to a ₹333 Crore profit machine in three years. The reason? Two things working simultaneously: EBITDA margins expanding from ~14% in FY23 to 25% in FY25, and a ₹720 Crore debt repayment that significantly cut interest costs. That debt clearance, management confirmed in Q4 FY25, means FY26 onwards the full benefit of lower finance charges flows straight to the bottom line.

Operating cash flows have been consistently positive and strengthening. The FY24 CFO was ~₹300 Crores, and FY25 capex came in at ₹408 Crores — fully funded from operations and IPO proceeds — meaning no equity dilution stress.

Q3 FY26 (December 2025 quarter) was the cleanest print yet: Revenue ₹556 Crores, PAT ₹100 Crores — an 86% jump in profit versus the same quarter last year. At the current LTM run rate, FY26 full-year PAT is tracking toward ₹340–360 Crores.

SECTION IV — Fundamental Valuation Metrics & Investment Call

Let me give you the honest valuation picture.

P/E Ratio: ~58x (LTM) This is not cheap. Let’s just say it plainly. You’re paying 58 times last year’s earnings. For context, most established Indian pharma companies trade at 25–35x. But this is a growth CRDMO, not a generics business. The global CRDMO comps — including the best Indian listed peers like Divi’s, Suven, or Laurus in their high-growth phases — have historically commanded 55–80x in bull cycles. On FY26E earnings of ~₹350 Crores, the forward P/E drops to approximately 58x. On FY27E, assuming 30% earnings growth (a conservative estimate given current momentum), you’re looking at a forward P/E of ~45x, which is closer to fair for this category.

P/B Ratio: ~8.8x High, but consistent with asset-light, high-IP businesses in contract pharma. Not a concern at this stage of the growth cycle.

ROE: ~15% (FY25), improving toward 20%+ as debt costs fall For context, this was 8.6% in FY24 and 1.1% in FY23. The direction matters more than the current number here.

ROCE: ~16% (FY25), climbing fast With debt cleared and new capacity now generating revenue, ROCE should comfortably cross 20% in FY27. That’s when the stock typically re-rates sharply.

EPS (LTM Diluted): ~₹15.7 per share — but growing fast. FY27E EPS could realistically be ₹21–24.

Dividend: Nil. The company pays no dividend and doesn’t intend to in the near term. All cash is being reinvested in growth. That’s actually the right call at this stage.

Target Price Rationale: At ₹1,200 — approximately 50x FY27E EPS of ₹24 — there’s ~28% upside from current levels. That’s a conservative 50x multiple for a business growing earnings at 30%+ with expanding margins and a strengthening balance sheet. The risk to this target is a broader market de-rating or a slowdown in global pharma outsourcing. The case for ₹1,350+ exists if FY27 earnings beat or if the sector re-rates upward on a global China+1 CRDMO supercycle narrative.

SECTION V — Long-Term Outlook & Risk Assessment

5-Year Return Estimate: 18–25% CAGR | 10-Year: 15–20% CAGR

Here’s why those numbers aren’t wishful thinking.

The global pharma outsourcing market is structurally shifting toward India. The China+1 supply chain strategy — where Western pharma companies deliberately diversify away from China-only sourcing — is creating a multi-year demand wave for Indian CRDMOs with the quality systems to handle complex molecules. This company is directly positioned to capture that wave, with 280+ global clients already embedded in its programs.

Management has been clear about the strategy: keep expanding manufacturing capacity in high-value areas (peptides, HPAPIs), deepen early-discovery relationships so the company gets CDMO work as molecules progress, and grow the biologics-adjacent services through partnerships like the Mabtech collaboration. The Boston presence gives them sales and delivery credibility with US biotech clients.

Capex through FY26-27 is projected to continue at ₹400–500 Crores annually — funded from operations, not equity issuance. That’s important. Dilution risk is low.

On promoters: Holding is 34.7%, which is on the lower side. Private equity firm TPG recently exited its ~15% stake through a block deal at ₹874. While the exit was orderly, it does mean future overhang risk from institutional sellers is now substantially reduced. The founding promoter group’s stake is stable. Watch for ESOP-related dilution; the company has been issuing shares under its ESOP program, adding ~10 lakh shares quarterly — manageable, but worth tracking.

What could go wrong? Don’t ignore these:

Client concentration. A handful of large innovator clients likely drive a significant portion of CDMO revenue. If a key molecule fails in Phase III trials or a large client consolidates, revenue can dip sharply.

Currency risk. Almost all revenue is in USD/EUR while costs are in INR. A strong rupee hurts margins. There’s natural hedging, but it’s imperfect.

Regulatory risk. Any USFDA Form 483 observation or import alert at their manufacturing sites would be catastrophic for the stock, as has been seen with peers. Quality systems are paramount and non-negotiable.

Valuation risk. The stock is priced for growth. If earnings growth disappoints even by a quarter or two, the re-rating could be severe given the 58x P/E.

Competition. Global CRDMOs (Lonza, Thermo Fisher, Samsung Biologics) have deep pockets and are expanding in Asia. Indian peers like Divi’s Laboratories, Syngene, and Jubilant are also competing for the same clients.

What’s going right: India’s CRDMO industry is forecast to grow from ~$3B today to $10–15B by 2035. Government incentives under PLI schemes, a large pool of skilled chemists, significantly lower cost structures than Western peers, and improving quality track records are all tailwinds. This company is well-positioned to compound on top of that industry growth.

Simply put: the next 10 years belong to Indian CRDMOs. This is one of the better-positioned businesses to ride that wave. It won’t be a smooth ride — the stock will test your conviction — but the fundamentals are pointing in the right direction.