Riding India’s Structural Demand Wave in a Rapidly Urbanizing Economy

I — Investment Thesis & Summary

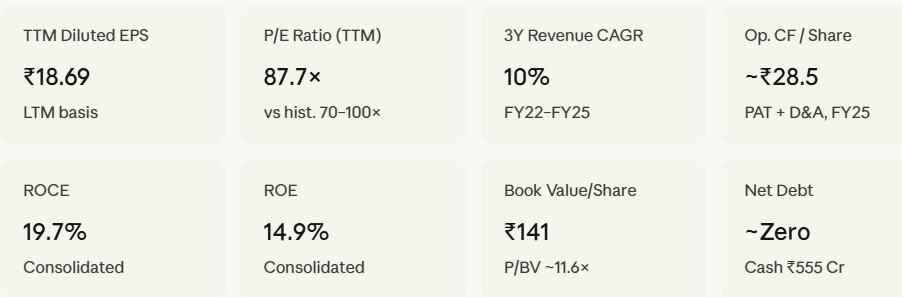

You’re looking at one of India’s finest building-materials businesses — lean balance sheet, strong brand, genuine pricing power in its core category. The stock, though, is priced for perfection at roughly 87 times trailing earnings. And right now, the near-term earnings story is anything but perfect.

The company makes the pipes, fittings, water tanks, adhesives, and increasingly the paints inside Indian homes and infrastructure. India’s construction cycle is its tailwind — and that tailwind is real and durable. But PVC and CPVC resin prices dropped sharply this year, creating inventory losses and squeezing margins just as heavy capex investments are pushing up depreciation.

Simply put: the business is fine, the volume growth is actually strong, but the earnings are getting squeezed by raw-material dynamics and rising fixed costs. Until those headwinds clear — probably by Q4 FY26 or early FY27 — the stock’s expensive valuation leaves limited room for upside. Hold what you have. Don’t aggressively add at current levels.

The call in one line: A quality compounder that deserves to sit in a long-term portfolio — but the entry point today demands patience, not urgency.

II — Business Model & Operations

The core of the business is pipes — specifically CPVC (chlorinated polyvinyl chloride) pipes and fittings, where this company was the pioneer in India and still commands premium positioning. CPVC is the go-to material for hot-and-cold plumbing inside homes because it handles pressure and temperature far better than regular PVC. The plumbing segment contributes roughly 72% of consolidated revenue.

But the company has been quietly building a second act. Adhesives and sealants — brands that construction workers across India reach for daily — account for a meaningful slice. The paints business is the newest leg, acquired through strategic acquisitions in 2021–22, and is still scaling. Water tanks, bathware (faucets, sanitaryware), valves, and construction chemicals round out a portfolio that now touches almost every surface of an Indian building project.

The distribution network is genuinely impressive — tens of thousands of touchpoints across India, plus exports to over 31 countries. New capacity is coming online too: the Kanpur plant is now operational, and the company has signed a deal to acquire an 80% stake in Nexelon Chem to produce 40,000 metric tonnes of CPVC resin annually — a backward integration move that should reduce raw-material dependency over time, with commercial production targeted for Q2 FY27.

The competitive moat here is brand + distribution. Plumbers and contractors specify this brand by name. That stickiness is hard to replicate and allows the company to pass through price increases when the cycle turns.

Youtube Link:

III — Historical Financial Review

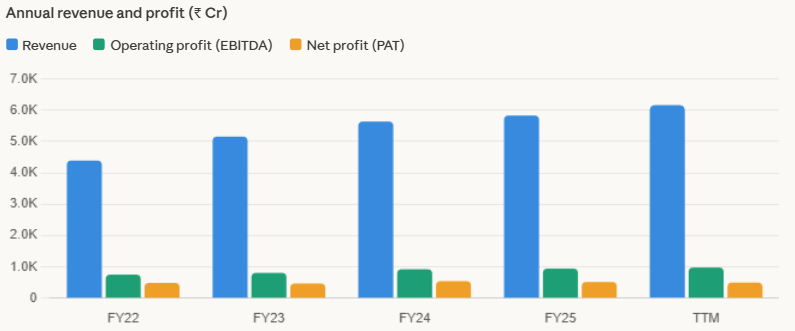

The revenue story has been consistent but not explosive. From ₹4,394 Cr in FY22 to ₹5,832 Cr in FY25, that’s a 3-year CAGR of roughly 10%. The trailing twelve-month run-rate is now pushing ₹6,162 Cr. Respectable — but the pace has clearly decelerated from the 17–20% growth years of the early 2020s.

Where it gets interesting — and a bit uncomfortable — is on the profit side. EBITDA has grown well, from ₹754 Cr in FY22 to ₹946 Cr in FY25, reflecting genuine operating leverage. But PAT has been lumpy: ₹490 Cr in FY22, dropped to ₹472 Cr in FY23 (commodity price volatility), recovered to ₹546 Cr in FY24, and then dipped again to ₹519 Cr in FY25. That’s essentially flat profit over four years on growing revenues — not the compounding story the valuation implies.

The main culprit for earnings softness has been raw material pricing — PVC and CPVC resin prices are set globally, and when they fall sharply (as they did in FY26), companies that bought inventory at higher prices book losses on that stock. It’s a timing issue, not a structural problem. But it’s real, and it’s hurting the current year.

IV — FY26 Quarterly Performance

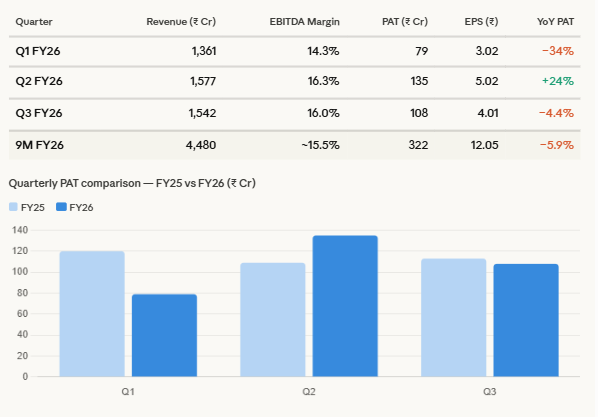

This is the most important thing to understand about this stock right now. The quarterly picture for FY26 has been a rollercoaster:

Q1 FY26 was genuinely alarming — PAT crashed 34% year-on-year as falling PVC/CPVC prices created inventory write-downs. Q2 bounced back strongly (+24% YoY) as volumes picked up — plumbing volumes grew 20.6% in Q2 FY26, which is excellent. Q3 then dipped again, with EBITDA margins compressing to 16.0% from 16.5% due to another round of PVC and CPVC price drops.

The nine-month PAT of ₹322 Cr is running about 6% below last year’s ₹342 Cr for the same period. Volume growth is healthy — plumbing volumes up 17% in 9M FY26, adhesives up 21%, paints up 15%. The problem is purely on realizations. When raw material prices fall faster than selling prices, margins get compressed in the short run.

V — Valuation, Target Price & Return Outlook

Let’s be direct: 87 times trailing earnings for a company whose profits haven’t grown in four years is a lot to pay. The justification historically has been: (a) India’s construction boom is structural and multi-decade, (b) the CPVC pipe category is still underpenetrated, and (c) this company is the quality operator in its space, commanding pricing power that commoditized competitors can’t match.

Those justifications remain valid. But the stock has already de-rated from over 100× at its peak. A further de-rating toward the 65–75× range is possible if earnings recovery takes longer than expected.

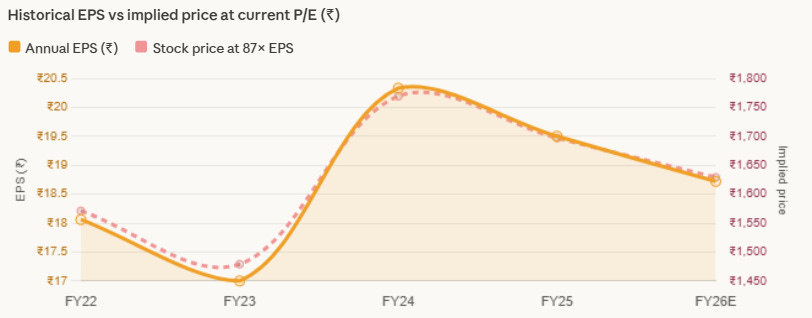

The numbers tell the story clearly. EPS has been essentially flat at ₹18–20 for three years, while the stock has maintained a premium multiple. That gap needs to close — either through earnings growing into the price, or the price retreating to meet earnings.

The base case target of ₹2,050 over three years assumes: PAT normalizes to ₹650–700 Cr by FY28 (roughly 10–12% EPS CAGR from current levels), and the P/E gently de-rates to around 65–70×. That implies about 7.5% annual price appreciation from today — modest for an equity investment, but this is the cost of buying quality at a premium multiple.

Add a dividend yield of 0.25% and the total return barely clears 8% annualized. Over 10–15 years, if EPS compounds at 12–15% (a reasonable long-term assumption given India’s infrastructure trajectory), the stock could deliver ₹4,500–6,500 — implying 10–11% annualized returns from today. Not bad, but not exciting either for someone deploying fresh capital.

VI — Bull Case & Bear Case

Bull case — ₹2,400+PVC/CPVC resin prices stabilize and inventory losses reverse. Plumbing volumes sustain 15–20% growth driven by Jal Jeevan Mission rollout and urban housing. Paints business reaches scale, adding a third profitable growth engine. Backward integration via CPVC resin plant reduces raw-material risk significantly from FY27. Market re-rates on earnings recovery.

Bear case — ₹1,200–1,300PVC prices continue declining, driven by Chinese export dumping. Government delays infrastructure spending. Housing demand cools in a higher-for-longer rate environment. Paints business bleeds cash competing against entrenched leaders. Heavy capex pushes up depreciation faster than revenue growth, keeping PAT suppressed. P/E de-rates to 55–60×.

The key risk to watch specifically is cheap PVC imports from China. The company has been lobbying for anti-dumping duties — if that protection comes through, it’s a meaningful near-term catalyst. If it doesn’t, margin pressure could persist longer than the market expects.

VII — Bottom Line

This is a business you want to own for the next decade — India’s housing and infrastructure story is real, and this company sits at the intersection of pipes, paints, and adhesives that go into every single construction project in the country. The brand moat is real. The near-debt-free balance sheet is a genuine strength. The backward integration into CPVC resin is a smart long-term move.

The problem today is simple: you’re paying 87× for a business whose earnings are going sideways right now. Volume growth is healthy, but it’s not translating into profit growth because of raw-material price swings and rising depreciation from capacity investments. A patient investor who already owns this stock should hold — the thesis is intact. Fresh buyers should wait for either a correction toward ₹1,400–1,450, or a clear signal that PAT is recovering strongly in Q4 FY26/Q1 FY27 results.