Revenue Grew 18%. Operating Profit Grew 47%. This Services Company.

A company grows revenue by 18%. Sounds ordinary. Nothing to write home about.

But its operating profit grew 47% in the same period. That’s not a rounding error. That’s operating leverage — the rarest, most powerful force in a services business.

And almost nobody is watching.

Section 01

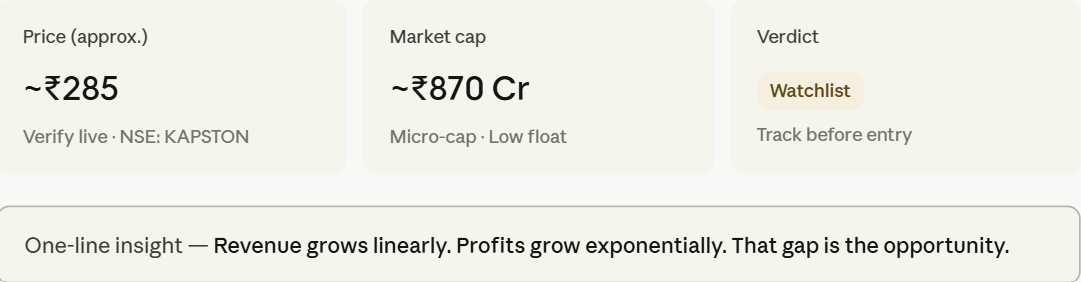

Quick snapshot

Section 02

What the market is missing

Facility management. Security guards. Housekeeping crews. The market hears these words and moves on.

That’s the mistake.

Investors slot this into the “manpower arbitrage” bucket — a low-margin, high-churn business with no moat. They expect 3–4% EBITDA margins forever. They stop looking.

Here’s what they’re missing: this company’s EBITDA margin just went from 5.06% to 6.33% in one year. A 127 basis point expansion in a single year is not noise. It’s a structural shift.

When a services company starts to scale, fixed overheads get amortized across more contracts. Every new client added becomes more profitable than the last. The business is at an inflection point — and the market hasn’t priced it in yet.

Youtube link:

Section 03

Business simplified

This is an integrated facility management company based in Hyderabad. It was started in 2009 and operates across 8 states in India.

What they do: They manage physical infrastructure for other businesses — security personnel, housekeeping teams, staffing support, and related facility services. They are ISO-certified, with training centres and branch offices.

Who pays them: Corporate offices. IT parks. Hospitals. Educational institutions. Companies that don’t want to manage a 500-person housekeeping workforce themselves. They outsource it. Completely.

Why it’s sticky: Switching costs are real. Onboarding a new facility management vendor means retraining hundreds of staff, renegotiating SLAs, and managing disruption. Most clients renew. That creates annuity-like revenue — predictable, recurring, and compounding quietly in the background.

Section 04

Financial momentum

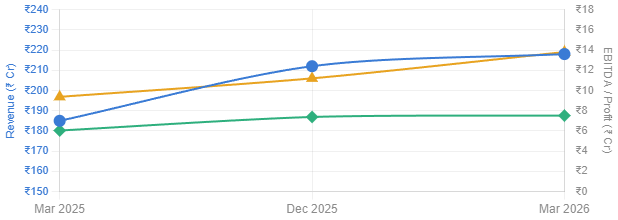

Three quarters. Three data points. One clear direction.

Revenue is growing steadily — ₹185 Cr → ₹212 Cr → ₹218 Cr. Nothing dramatic. But operating profit tells the real story: ₹9.37 Cr → ₹11.2 Cr → ₹13.8 Cr. Nearly 47% year-on-year.

Net profit grew 24% to ₹7.52 Cr. EPS moved from ₹1.99 to ₹2.47. Quietly and consistently.

This is not a manpower business.

It’s a recurring contract business.

The guards and housekeepers are inputs. The 5-year client contract is the asset.

Section 05

Key triggers to watch

Geographic expansion: Currently in 8 states. India has 28. Every new state is incremental revenue with near-zero fixed cost addition — pure margin expansion.

Government contracts: Central and state government facilities are massive, stable, and long-term. A single large tender could step-change revenue.

Margin compounding: If EBITDA margins reach 8–9% (achievable at scale), profit will grow 3–4x faster than revenue. The leverage is already showing.

Healthcare and education demand: Post-pandemic, hospitals and campuses are investing heavily in hygiene-led facility management. This company is positioned directly in that tailwind.

Quarterly EPS consistency: Three straight quarters of rising EPS. If Q1 FY27 continues the trend, institutional interest could accelerate rapidly.

Section 06

Smart money signals

The stock delivered 3x+ returns over three years before a meaningful correction. That’s the classic pattern: early compounding, then a reset as retail profit-booking hits the thin float.

Average daily volume is extremely low — typically under 20,000 shares per session. A stock like this doesn’t need a large investor to move. It needs the right one to notice.

Delivery percentages have held firm even through the correction. That signals holders who believe in the story, not traders chasing momentum.

The stock is now trading at a significant discount to its 52-week high — while the business is printing its best margins ever. That divergence doesn’t last long.

Section 07

Risks — unfiltered

Extreme illiquidity: With barely ~20,000 shares traded daily, getting in or out at a fair price is genuinely hard. This is not a trading stock.

Wage inflation: The entire business model runs on human labour. A minimum wage hike or labour market tightening squeezes margins instantly.

Client concentration: Small companies often rely on a handful of large clients. If one large client renegotiates or exits, revenue takes a visible hit.

Larger players circling: This market is attracting giants — Quess, TeamLease, SIS, and multinationals. A well-funded competitor can undercut on price aggressively.

Margin ceiling: Facility management structurally caps at 8–10% EBITDA. There’s no software-like scalability. Growth will always require adding people.

Section 08

Final verdict

Why this deserves a spot on your watchlist

Most investors will never look at this company. It’s too small. Too boring. Too illiquid. And that’s precisely the point.

The businesses that create real wealth are often the ones that look completely unexciting from the outside — and completely compelling from the inside.

Revenue growing 18% is fine. EBITDA growing 47% is extraordinary. That gap — the 29 percentage points between them — is a business becoming more efficient without trying to look flashy. That’s the kind of compounding that makes portfolios.

It won’t double overnight. But three years from now, if they expand to 15 states, hold their margins, and land even one large government contract — the EPS story could look very different.

Track it. Understand it. Wait for the right price. That’s the discipline that separates investors from speculators.