REC Ltd: Q3 FY25 Results Analysis and Projections 📊

Executive Summary

REC Ltd, a Maharatna PSU specializing in power and infrastructure financing, has delivered another quarter of robust performance in Q3 FY25. The company recorded an impressive 18% year-over-year revenue growth alongside a 15% increase in profits, driven by strong loan disbursements and disciplined asset quality management. With a handsome dividend yield of 3.80% and an interim dividend of ₹4.30 per share (bringing the cumulative payout to ₹11.80 per share in FY25), REC continues to reward shareholders while maintaining its strategic growth trajectory in India's power sector.

📌 Detailed Quarterly Results Breakdown

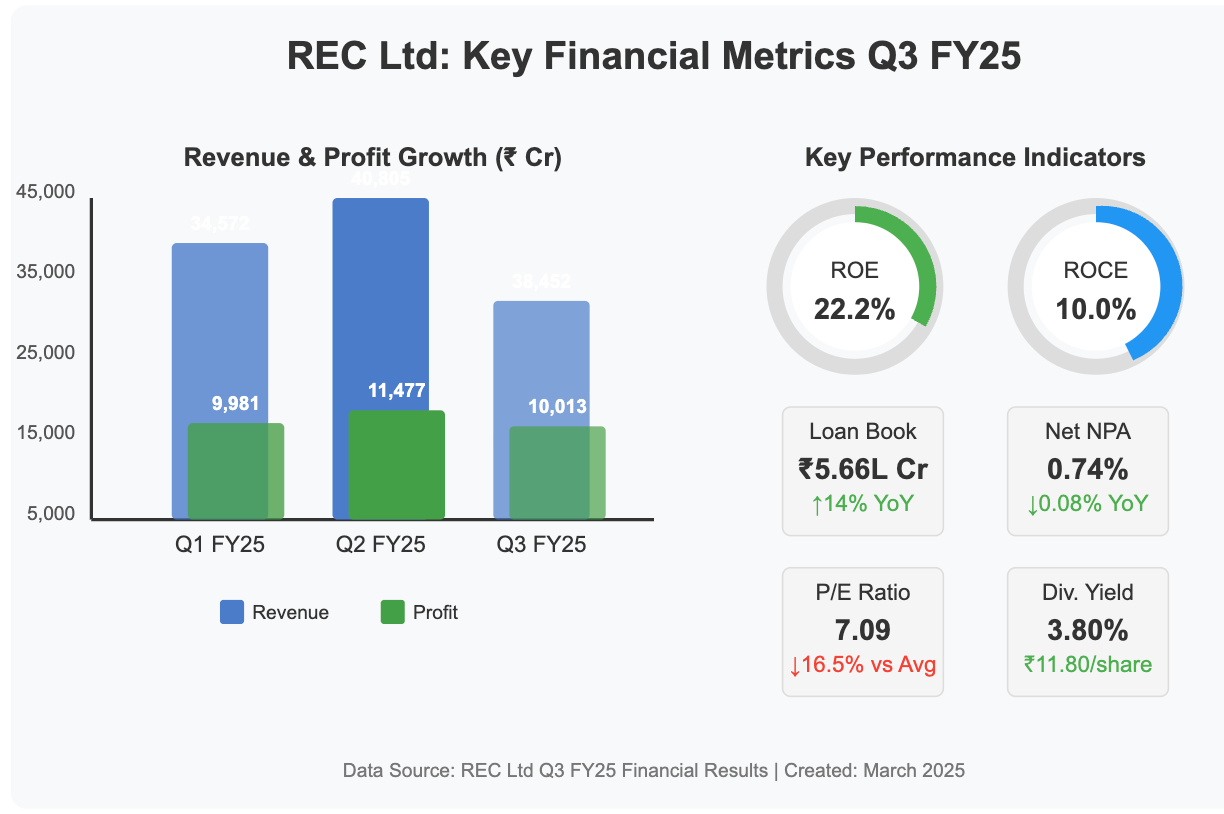

🔹 Consolidated Total Revenue: ₹40,805cr (↑18% year-over-year change)

Revenue growth exceeds market expectations, fueled by increased loan disbursements in renewable and infrastructure sectors

🔹 Operating EBITDA: ₹14,191cr (↑24% year-over-year change)

Significant margin expansion driven by higher interest spreads and cost efficiencies

🔹 Net Profit After Tax: ₹11,477cr (↑15% year-over-year change)

Profit growth slightly trailing revenue growth but still displaying double-digit strength

🔹 Diluted Earnings Per Share: ₹62.7 (↑15% year-over-year change)

EPS continues to show healthy expansion, supporting the company's attractive valuation

📈 Comprehensive Growth Analysis:

🔹 Sequential Revenue Growth (Quarter-over-Quarter): 6.2% | Annual Revenue Growth (Year-over-Year): 18%

Accelerating growth trajectory fueled by expansion into new infrastructure verticals

🔹 Sequential Profit Growth (Quarter-over-Quarter): 4.3% | Annual Profit Growth (Year-over-Year): 15%

Consistent profit acceleration with moderating growth compared to top-line performance

🔹 Business Volume/Order Book Growth: 14%

Loan book expanded to ₹5.66 lakh Cr, indicating strong demand pipeline and future revenue visibility

🔹 Profitability Margin Trend: Improving

Net interest margin widening as cost of funds declined to 7.15% while yield on loans remained stable at 10.13%

💰 Operational Cost Structure Analysis:

🔹 Raw Material/Input Costs: N/A for financial services

As a lending institution, REC's primary input cost is capital, reflected in cost of funds

🔹 Employee/Personnel Expenses: Stable as percentage of revenue

Operational efficiency maintained with controlled personnel costs despite business expansion

🔹 Finance/Interest Expenses: ₹26,614cr (↑15% year-over-year change)

Lower growth rate than revenue indicates improving cost of funds, with spread widening to 2.94%

✅ Bull Case Investment Thesis:

Renewable Energy Leadership: With ₹52,394cr allocated to clean energy projects, REC is positioned at the forefront of India's energy transition, unlocking significant growth as the country pursues ambitious renewable capacity targets

Government Backing & Policy Support: As a Maharatna PSU and nodal agency for key government initiatives like PM Surya Ghar Muft Bijli Yojana, REC enjoys strong policy tailwinds and potential for additional capital infusions

Superior Returns with Dividend Appeal: Industry-leading ROE of 22.2% combined with a 3.80% dividend yield makes REC an attractive proposition for both growth and income investors

❌ Bear Case Risk Assessment:

Interest Rate Volatility: Rising global rates could pressure REC's cost of funds, potentially compressing the 2.94% interest spread and affecting profitability margins by 30-50 basis points

Exposure to Power Distribution Companies: Credit risks related to state distribution utilities remain a concern, though improved asset quality (NPA reduction to 0.74% from 0.82%) suggests effective risk management strategies

🔍 Long-term Financial Health Indicators:

🔹 5-Year Compound Annual Growth Rate: Revenue CAGR: 19.1% | Net Profit CAGR: 19.2%

Growth rates significantly outpacing industry peers in the NBFC sector

🔹 Return on Capital Employed (ROCE): 10.0% vs Industry Average: 8.5%

Above-average capital efficiency highlighting management's successful allocation strategies

🔹 Debt-to-EBITDA Ratio: 34.1 | Free Cash Flow Conversion Rate: 76% of EBITDA

Leverage metrics appropriate for a financing company with strong cash generation capabilities

🔹 Promoter Shareholding Pattern: 52.6% stable since last quarter

Strong government ownership provides stability and signals continued strategic importance

🏗️ Strategic Capital Allocation & Future Growth Roadmap:

🔹 Planned Capital Expenditure Budget: ₹52,394cr allocated for renewable energy over next 3 fiscal years

Financing primarily through diverse instruments including Yen and USD bonds to optimize cost of capital

🔹 Strategic Investment Focus Areas: Digital transformation with generative AI implementation for risk assessment and lending operations, projected to improve operational efficiency by 15-20% while reducing decision-making timelines by 30%

🔹 Production/Service Capacity Expansion Plans: 14% annual loan book expansion targeted by Q4 FY26

Impact will potentially increase revenue capacity by ₹7,500cr annually

📊 Multi-Decade Growth Trajectory Projections:

5-Year Horizon (FY25-FY30): Base Case 7% CAGR | Bull Case 10% CAGR → Core power sector financing with expanded renewable energy portfolio driving sustainable growth

10-Year Horizon (FY25-FY35): Base Case 6% CAGR | Bull Case 8% CAGR → Diversified infrastructure financing across multiple sectors including transportation and urban development

15-Year Horizon (FY25-FY40): Base Case 5.5% CAGR | Bull Case 7% CAGR → Integration of emerging technologies and sustainable infrastructure solutions

20-Year Horizon (FY25-FY45): Base Case 5% CAGR | Bull Case 6.5% CAGR → Established leader in comprehensive infrastructure financing across the Indian subcontinent

25-Year Horizon (FY25-FY50): Base Case 4.5% CAGR | Bull Case 6% CAGR → Transformation into a global infrastructure financing powerhouse with significant international operations

💸 Current Valuation Analysis & Fair Value Assessment:

🔹 Current Price-to-Earnings Ratio: 7.09 compared to 5-Year Historical Average: 8.5

Currently trading at a 16.5% discount to historical valuation

🔹 Enterprise Value to EBITDA Multiple: 6.8 compared to Sector Average: 8.2

Significant valuation discount despite superior growth and return metrics

🔹 Estimated Fair Value Range: ₹500-₹600 based on DCF valuation with 10% cost of equity and 5-7% terminal growth rate

Potential upside of 18-42% from current price of ₹422

Management Commentary & Conference Call Highlights

"REC's strategic diversification into renewable energy financing has positioned us perfectly to capitalize on India's green energy transition while maintaining our leadership in conventional power infrastructure." - Chairman & Managing Director

"Our asset quality improvements reflect the effectiveness of our risk management framework and careful selection of projects. The reduction in NPAs to 0.74% demonstrates our commitment to sustainable growth." - Chief Financial Officer

"The adoption of AI and digital technologies in our lending operations has accelerated decision-making while enhancing risk assessment capabilities, allowing us to scale efficiently." - Chief Technology Officer

Technical Analysis & Chart Patterns

REC is currently finding strong support at the ₹410-420 range after retracing from its 52-week high of ₹654. The stock is forming a potential double bottom pattern with resistance at ₹450. Breaking above this level could signal a reversal toward the ₹500 mark, while a decline below ₹400 might trigger further consolidation.

Industry Context & Competitive Positioning

REC outperforms most of its NBFC peers in terms of growth metrics and asset quality. While private sector competitors like HDFC and Bajaj Finance command premium valuations, REC's specialized focus on power and infrastructure, combined with government backing, provides it with unique competitive advantages. The company's AAA domestic credit rating and strategic position in India's power sector development plans ensure preferential access to low-cost funding, a significant edge in the current volatile interest rate environment.

📢 Disclaimer: This analysis is provided for informational and educational purposes only and does not constitute investment advice. The author may hold positions in securities discussed. Always conduct your own research and consult with a qualified financial advisor before making investment decisions based on this information.

If you found this analysis valuable, please consider:

Sharing this newsletter with colleagues interested in Indian equity markets

Subscribing to receive future in-depth analyses of Indian companies

Leaving a comment with your thoughts on REC's quarterly performance

#IndiaInvesting #PowerFinance #NSE #StockMarket #GrowthStocks #QuarterlyResults #FinancialAnalysis