When Profits Grow 3× Faster Than Revenue — Something Powerful Is at Work

Profits are up 188% year-on-year.

No product launch. No government contract. No hype cycle.

Just a quiet, unglamorous business doing what it has always done — only now, doing it far more profitably.

The market hasn’t caught up. It rarely does — until it suddenly does.

1 — Quick Snapshot

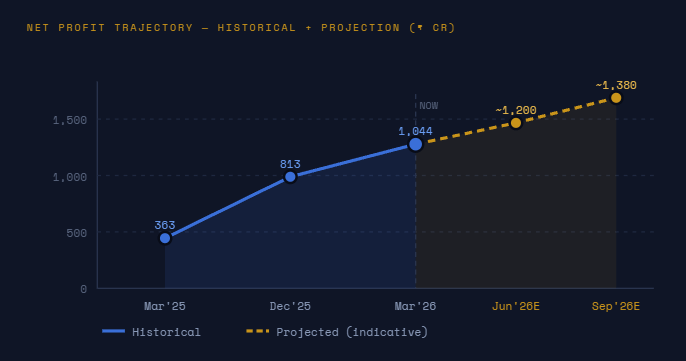

Operating leverage has quietly turned violent — and in asset-heavy businesses, profit cycles can overshoot for far longer than skeptics expect.

2 — What the Market Is Missing

The Misread. The Mispricing.

Here’s the problem: most investors hear the word “shipping” and immediately think cyclical, volatile, avoid. They’re not wrong about the cycle. They’re wrong about the timing.

This business is dismissed as too global, too macro-dependent, too opaque. Rates go up, rates go down — nobody wants to model that. So they ignore it entirely.

That’s the mispricing.

What the market keeps missing is the asset value story hiding underneath. This isn’t just a freight business. It’s a fleet of owned, hard assets sitting on the water — assets that appreciate precisely when rates rise, and that can be monetized at will.

The company’s Net Asset Value is often higher than its market cap. The stock trades at a discount to what you’d pay to replace its fleet. That’s not a value trap — that’s a margin of safety most sectors never offer.

And right now? The cycle isn’t turning. It has already turned.

3 — Business Simplified

What It Actually Does

Imagine the ocean as a highway. Oil, petroleum products, and dry commodities need to travel that highway — from producers to refiners, from refiners to consumers. Someone has to own the trucks.

This company owns those trucks. Except the trucks are supertankers and dry bulk carriers.

Who pays them? Global oil majors. Commodity traders. Refiners across Asia, Europe, and the Americas. These aren’t small counterparties — these are some of the most creditworthy names in the world.

Why is it sticky? Three reasons:

① Long-term time charters lock in predictable revenue — no scramble every quarter.

② They own the fleet outright — no leases, no per-trip exposure. Fixed costs are largely covered before the first dollar of spot revenue arrives.

③ The global fleet orderbook is tight. New vessels take 2–3 years to deliver. You can’t conjure supply overnight.

It’s a business that looks dull — until rates move. And when rates move, it’s the most leveraged bet in the market.

4 — Financial Momentum

The Numbers Are Screaming

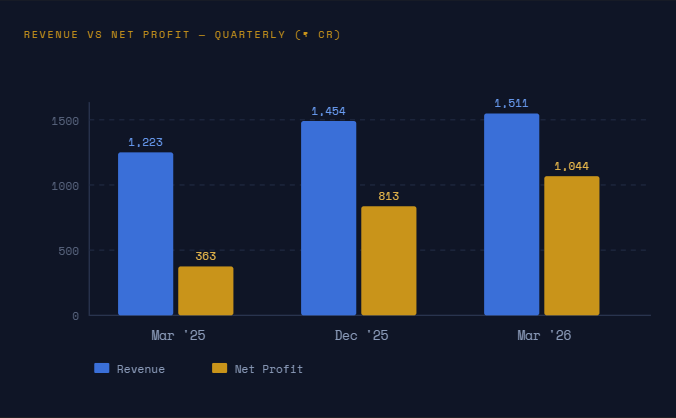

Let’s start with revenue. It grew 24% year-on-year. That’s solid. But revenue is not where the story lives.

EBIDT jumped 88%. Net profit? Up 188%. That’s not a rounding error — that’s operating leverage doing exactly what it’s supposed to do in an asset-heavy business when rates turn in your favour.

The net margin this quarter? Over 69%. Read that again. Nearly 70 paise of every rupee in revenue fell to the bottom line. That’s not a margin profile — that’s a money-printing machine running at full capacity.

📊 Growth Snapshot

This is not just a shipping company.

It's a leveraged bet on global trade —

backed by hard assets that appreciate

exactly when you need them to.

5 — Key Triggers

What Can Move the Stock

Red Sea disruptions persist. Every extra mile a tanker travels is extra revenue. Rerouting around the Cape of Good Hope has effectively added 20–25% to voyage distance. That’s not a blip — it’s structural demand.

India’s refinery expansion. India is building and expanding refineries. More refinery capacity means more crude imports, more product movements — and more demand for exactly what this company operates.

Global fleet renewal cycle. Old vessels are being scrapped. New builds take 2–3 years to deliver. In the gap between scrapping and supply, existing fleet owners enjoy pricing power.

Asset monetization optionality. The company can sell vessels at peak valuations, book large one-time gains, and redeploy capital. It has done this before. The fleet’s current replacement cost is well above book value.

Dividend re-rating. With earnings jumping sharply and a history of rewarding shareholders, a dividend surprise could trigger institutional re-rating and fresh buying.

6 — Smart Money Signal

The Quiet Accumulation

You rarely see this stock trending on finance forums. It doesn’t have a colourful founder narrative. There’s no viral product. No influencer coverage.

And yet — the volumes tell a different story on certain days. Steady, below-the-radar buying on dips. Minimal panic during sector corrections. Promoter holding that hasn’t moved — which means no one is exiting from the top.

The dividend history is another tell. Businesses that consistently return cash to shareholders aren’t gambling on their own futures. They know something about earnings sustainability that the stock price hasn’t priced in yet.

Low float. High institutional underownership. Improving fundamentals. That combination doesn’t stay quiet forever.

7 — Risks

The Honest Warning

Cyclical ReversalShipping rates can collapse fast. A global recession, a supply surge from newbuilds, or a resolution of geopolitical disruptions could hit revenues hard and quickly. The same operating leverage that drives 188% profit growth on the way up can destroy profits on the way down.

USD Currency RiskRevenue is in dollars. Costs are partially in rupees. A strengthening rupee compresses margins without the business doing anything differently. This is a constant, invisible headwind.

Fleet Oversupply RiskIf the global orderbook delivers en masse, supply floods the market. Rate negotiations shift from the shipowner to the charterer. Margins compress. Timing this is nearly impossible.

Capex and DebtRunning and renewing a fleet is expensive. Asset-heavy businesses require constant reinvestment. A downturn during a capex cycle is particularly painful — you’re spending while earnings shrink.

8 — Final Verdict

Why You Should Be Tracking This

Most investors wait for the headline. The front-page story. The analyst upgrade. The price breakout.

This one hasn’t had its headline yet.

Profits just tripled. Margins are at decade-high levels. The asset base is worth more than the market is paying for it. And the cycle — by most estimates — is nowhere near its peak.

The gap between what a business is doing and what the market is pricing — that gap is where serious returns are made.

Right now, that gap is unusually wide.

Track it. Understand the cycle. Size accordingly.