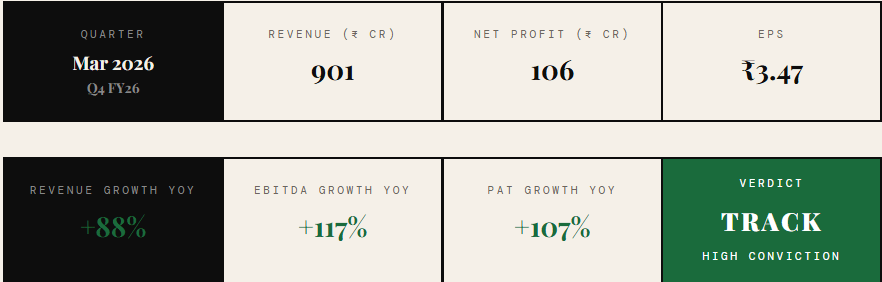

Profits Just Doubled. No One's Talking About It.

Net profit just more than doubled — in a single year. Revenue is up 88%. EBITDA grew 117%.

And almost nobody in the market is discussing it.

This company operates in one of the most critical sectors in India right now. It is not glamorous. It doesn’t have a viral founder. The CNBC anchors aren’t chasing this story.

But the numbers are screaming something the market hasn’t priced in yet. That gap — between what the numbers say and what the market believes — is exactly where great investments are born.

Section 1

The Numbers at a Glance

💡 ONE-LINE INSIGHT: When profits double and the street stays quiet, that's not a red flag — that's a runway.

2 . What the Market is Missing

The Invisible Opportunity

Power companies in India have a reputation problem. They are seen as government-dependent, cyclical, and slow. One bad monsoon, one policy change, one payment delay from a state DISCOM — and investors run.

That narrative is old. And it’s wrong for this company.

Here is what the market is missing: this is not a utility playing at the mercy of regulators. It has carved out a position in a niche of the power value chain where execution matters far more than policy. Where clients cannot easily switch vendors. Where orders are not one-time — they repeat.

The market sees a power company. It should see a precision services and infrastructure business that happens to operate in the power sector.

The sector discount that the market applies is actually this company’s greatest gift. It keeps the stock off radar screens just long enough for patient capital to accumulate.

— The Power Signal, July 2026

Most institutional analysts don’t cover it. Most retail investors have never heard the name. That’s not a warning sign. In a country adding megawatts every quarter, that’s a misallocation of attention.

3 Business Simplified

What Does This Company Actually Do?

Strip away the sector noise and the business is simple.

It operates in the power infrastructure space — serving utilities, large industrial customers, and government-backed energy projects. Think of the invisible plumbing of India’s electricity system: the transformers, cabling infrastructure, switchgear, and service contracts that keep the grid alive.

Who pays them? State electricity boards. Industrial conglomerates. Renewable energy developers. Infrastructure project developers. These are not fly-by-night clients. They sign multi-year contracts. They pay because their plants and grids literally cannot operate without this company’s services.

Why is it sticky? Switching costs are real. Once you’ve integrated a vendor into critical power infrastructure, you don’t swap them out for a 5% cost saving. The relationship deepens over time. Repeat orders come not out of loyalty — but out of operational necessity.

This is infrastructure dependency dressed up as a small-cap stock. The market hasn’t noticed the difference yet.

4 Financial Momentum

The Numbers Don’t Lie

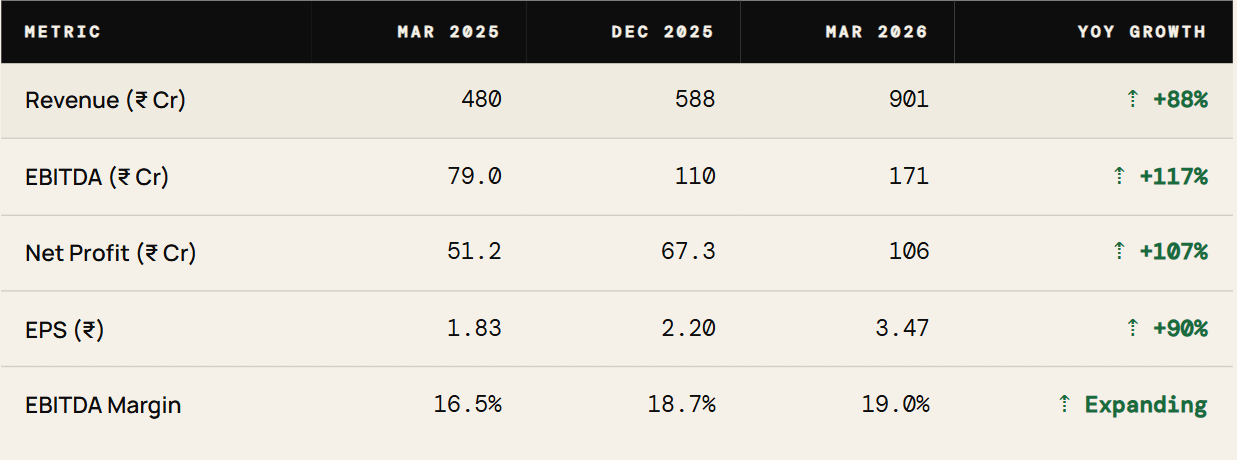

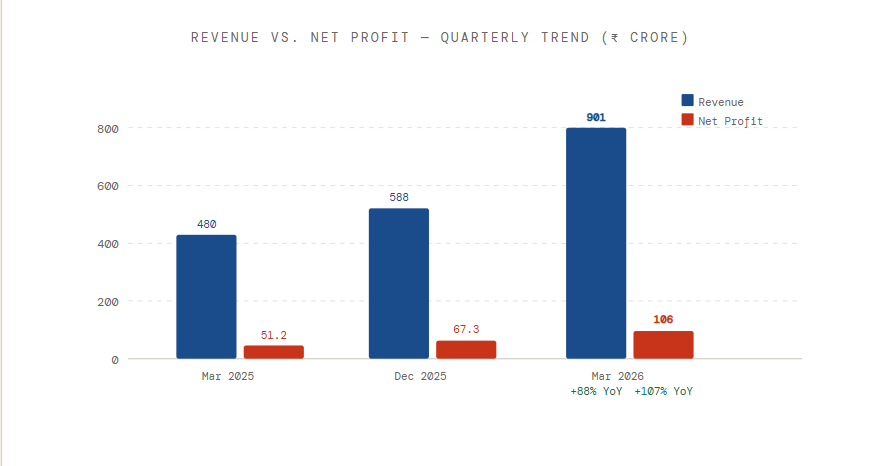

Revenue went from ₹480 crore to ₹901 crore in one year. That is not a rounding error. That’s a business that nearly doubled its top line.

But here’s what’s more important: profits grew faster than revenue.

EBITDA jumped 117%. Net profit jumped 107%. When profits outpace revenue growth, that’s operating leverage in action. Margins are expanding. Fixed costs are getting absorbed. The business is maturing without losing its growth velocity.

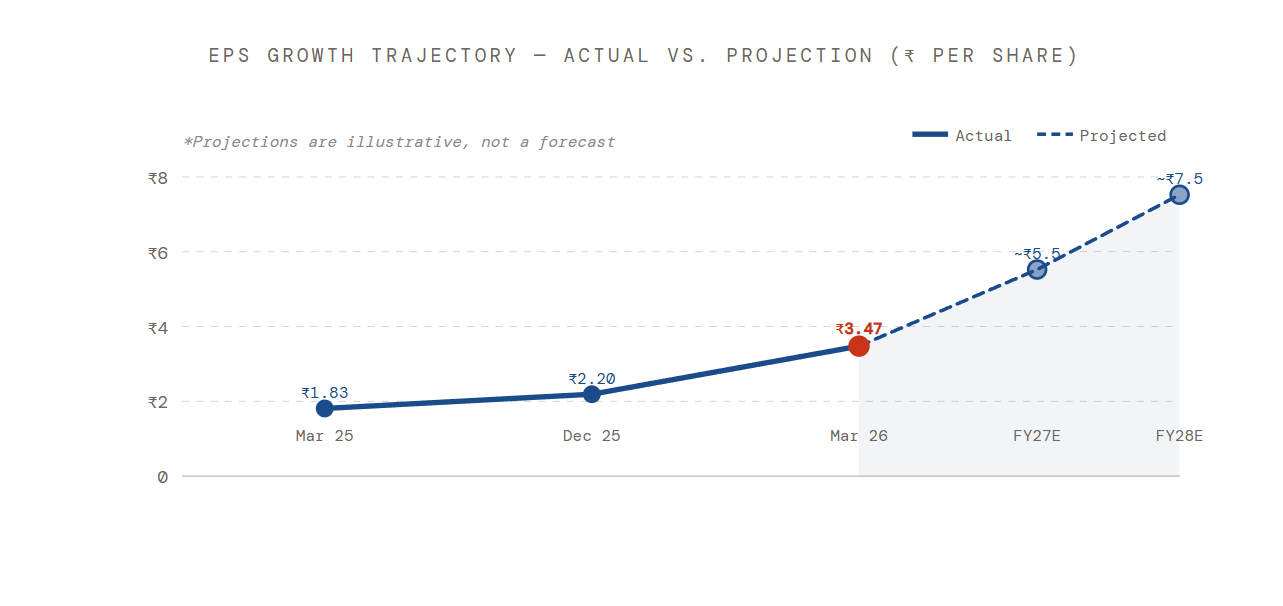

EPS has gone from ₹1.83 to ₹3.47 in just one year. The earning power of each share is compounding rapidly. If this trajectory holds for even two more years, the current price will look like a gift.

📊 Growth Snapshot

This is not just a power business.

It is an inevitability business.

India will add hundreds of gigawatts in the next decade. Every megawatt needs infrastructure. This company is in the critical path. You don’t skip the plumber when you’re building a city.

5 Key Triggers

What Could Move This Stock

⚡

Order Book ExpansionIndia’s accelerating energy transition means more tenders, more contracts. A single large order announcement can rerate the stock overnight.

📈

Margin Consolidation Above 20%EBITDA margins are at 19% and climbing. A sustained cross above 20% will trigger institutional interest in a big way.

🔎

Analyst Coverage InitiationCurrently underfollowed. The moment one credible research house publishes a note, the discovery cycle begins. Price discovery accelerates sharply.

🌏

Export or Cross-Border Energy ProjectsIndia’s energy diplomacy is expanding. Any news of international project participation would be a significant re-rating catalyst.

💰

Dividend or Bonus AnnouncementRising EPS (₹3.47 and climbing) creates room for capital returns. Any such signal boosts retail sentiment sharply.

6 Smart Money Signal

Who Is Already Watching?

You won’t see this in a press release. But patterns don’t lie.

📦Consistent Volume AccumulationOn quiet market days, this stock often sees above-average volumes with minimal price movement. That’s not retail — retail chases price. That’s accumulation.

🏛️Promoter ConfidenceNo significant promoter selling in recent quarters. When insiders hold steady despite sharp profit booking by others, it signals they expect more upside.

📉Low Float, High Resistance to SellingLow free float creates a coiled spring. When institutional conviction builds, supply dries up. Price moves can be non-linear and fast.

🧭Sector Tailwind AlignmentGovernment capex in energy continues to rise. Every infrastructure project in the power space is a potential order. The pipeline is structural, not cyclical.

Smart money moves before the story is obvious. By the time analysts publish, prices have already moved. The signal is in the numbers today — not the headlines tomorrow.

7 Risks — No Sugarcoating

Where This Can Go Wrong

01

DISCOM Payment Delays

State electricity boards in India have a history of slow payments. Any spike in receivables will dent cash flow and strain working capital — fast.

02

Margin Reversal from Raw Material Pressure

Copper, aluminium, and other input costs are volatile. If margins peaked at 19% and fall back to 14–15%, the growth story narrative takes a serious hit.

03

Order Concentration Risk

If revenue growth is driven by one or two large clients, the P&L is more fragile than it looks. Client attrition or project delays can crater a full year’s earnings.

04

Governance and Disclosure Quality

Small-cap power companies in India have mixed governance track records. Thin disclosure, related-party transactions, or promoter pledge increases are red flags to watch.

05

Valuation Re-rating Risk

If the market starts pricing in the growth — and then growth slows even slightly — the multiple compression can be brutal. Entry price matters enormously here.

8 Final Verdict

Why You Should Care About This Right Now

Here’s the honest truth: this company may never make the front page of a business paper. The promoters don’t attend conferences. The stock doesn’t trend on social media.

And that is precisely the point.

In Indian small-cap investing, the best returns almost always come from companies that are boring until they’re not. Where you buy silence and sell headlines. This company has just reported a year where profits doubled, EBITDA margins expanded, and EPS grew 90%. And yet — most investors are unaware it exists.

If margin expansion continues toward 22–23% over the next two years, if order books swell as India’s energy infrastructure build-out accelerates, if even one institutional fund starts building a position — the discovery cycle becomes self-reinforcing.

The biggest risk with this stock is not owning it when the market finally pays attention.

— Track it. Understand it. Then decide.

India’s power demand is structural. It doesn’t care about interest rates. It doesn’t care about global sentiment. It cares about whether the lights stay on and the factories keep running. This company is part of that infrastructure.

You don’t have to bet big right now. But not having it on your watchlist in July 2026 — given these numbers — would be a mistake you’d remember.