Everyone Is Chasing EV Brands. This Company Is Actually Building the Buses.

Everyone is chasing the flashy EV brands. The ones with the best commercials. The ones on the front page.

Meanwhile, a company that physically builds the electric buses rolling through Indian cities is sitting right there — unloved, under-covered, underpriced relative to what it’s becoming.

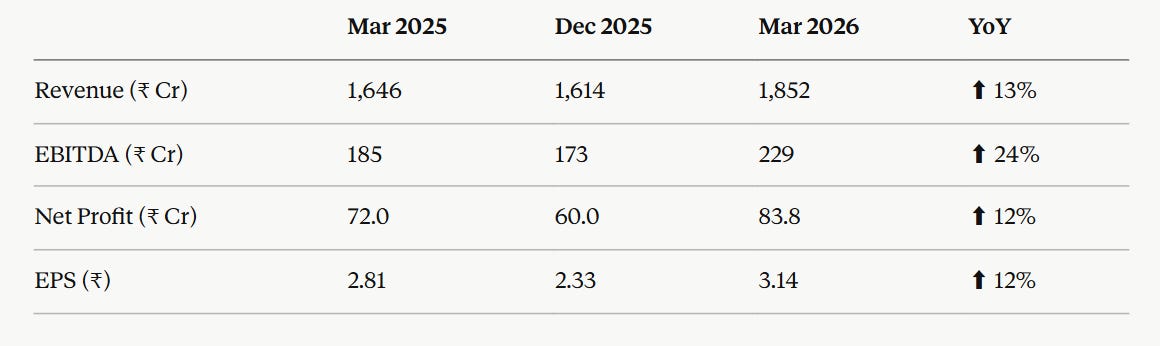

EBITDA grew 24% year-on-year. Revenue crossed ₹1,852 crore in a single quarter. The margin expanded quietly, without announcement.

The market has not caught on. Yet.

SECTION 1

One-line insight: This is a two-engine business — a cash-generating auto components arm funding an EV bus arm with government tailwinds. The market is pricing only the first engine.

Youtube link:

SECTION 2 — WHAT THE MARKET IS MISSING

Here’s the problem. When people hear “auto components,” their eyes glaze over.

Sheet metal. Dies. Moulds. It sounds like a 1990s Bharat Forge cousin. Low margin, cyclical, boring.

So they don’t dig deeper. And that’s the mistake.

Inside this company is a second business — electric buses. Built from scratch. Now being deployed at scale across state transport undertakings, municipal corporations, and defense contracts. India’s EV bus market is not a future story. It’s a present story. Orders are coming in. Fleet deployments are happening.

The legacy auto components business is not a liability. It is the cash engine that funds the EV capex without diluting shareholders. Most pure-play EV bets need constant fundraising. This one doesn’t.

That structural advantage is invisible if you just scan the headline numbers.

SECTION 3 — BUSINESS SIMPLIFIED

What it does: Makes two things.

Business 1 — Auto Components. Sheet metal parts, tools, dies, and moulds. Supplied to OEMs — passenger car makers, commercial vehicle manufacturers, tractor companies. Long-term contracts. Sticky relationships. Hard to displace once you’re embedded in a supply chain.

Business 2 — Electric Buses. Designs, manufactures, and sells full electric buses. Customers include state transport undertakings, municipal bodies, and government procurement agencies. Also earns from spare parts and maintenance contracts — recurring revenue on top of the upfront sale.

Why it’s sticky: OEM supply chain relationships take years to build. Once you’re a tier-1 supplier to a large automaker, you’re in for the lifecycle of that model. Switching costs are enormous. And on the bus side, government contracts come with long-term service agreements. Revenue doesn’t just appear once — it repeats.

This is not a commodity business dressed up as a growth stock. It’s a platform with defensible moats on both sides.

SECTION 4 — FINANCIAL MOMENTUM

Three numbers tell the real story.

Revenue grew 13% YoY — solid, but not the headline here.

EBITDA grew 24% YoY — faster than revenue. That means margins are expanding. The business is getting more efficient even as it scales.

Net profit grew 12% YoY — slightly below EBITDA growth, reflecting higher depreciation as EV bus capacity comes online. This is expected. It’s not a red flag; it’s capex maturing.

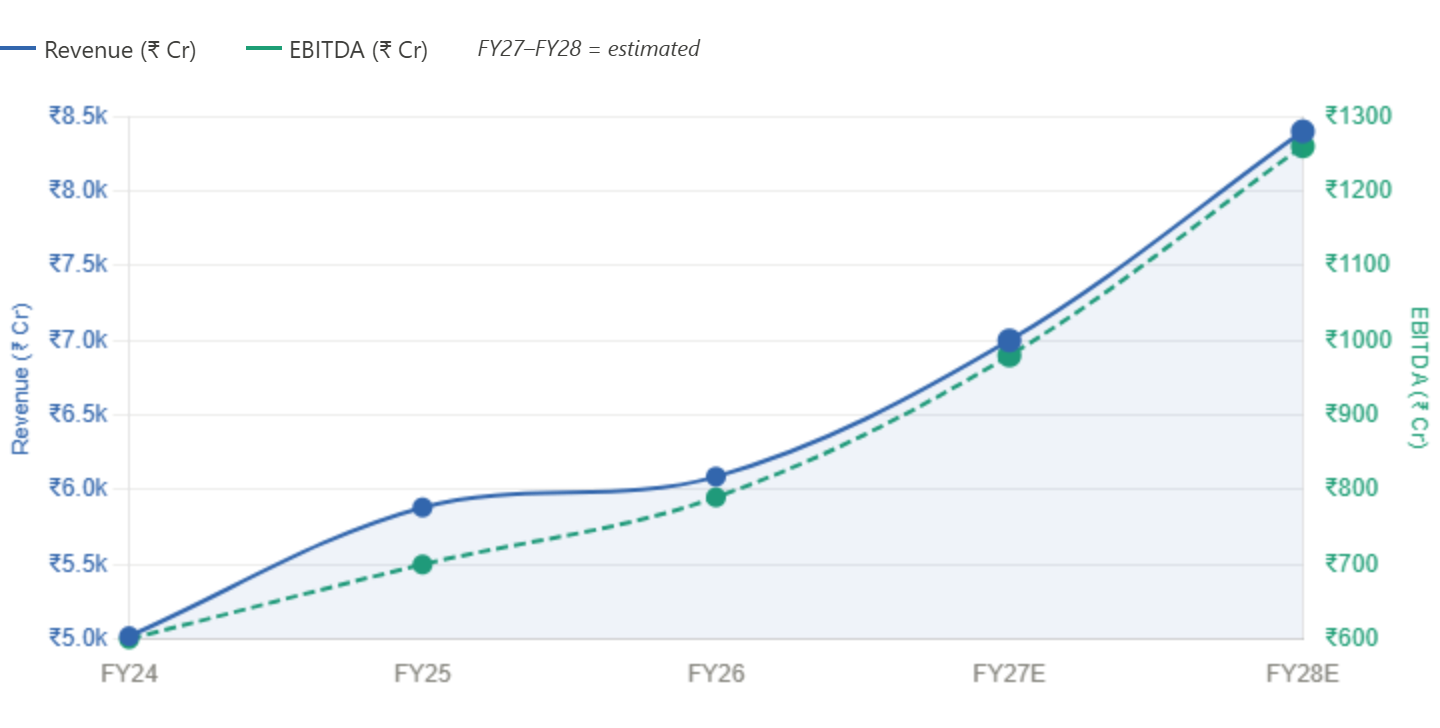

EBITDA margin moved from 11.2% to 12.4% in one year. Small number, large implication. Every percentage point of margin on ₹7,000+ crore annual revenue is meaningful at the bottom line.

EPS at ₹3.14 for the March 2026 quarter — annualised, that’s a business generating real per-share earnings growth.

📊 Growth Snapshot

SECTION 4.5 — PATTERN INTERRUPT

This is not just an auto company. It’s an infrastructure company.

Every electric bus it sells becomes a node in India’s public transport grid. And for the next decade, that grid is being built with government money.

You’re not buying a manufacturer. You’re buying a pick-and-shovel play on India’s EV transition — with an existing profitable business as the safety net.

SECTION 5 — KEY TRIGGERS

What can move this stock significantly:

1. EV Bus Order Flow. Every large government tender win is a direct earnings catalyst. Watch CESL, state transport tenders, and Defence procurement announcements.

2. EBITDA Margin Crossing 14%. The trajectory is set. If margins reach 14%, the earnings upgrade cycle begins. Analysts will be forced to revise targets upward.

3. Export Push. JBM Group operates in 10+ countries. If the EV bus business starts shipping internationally, the revenue TAM multiplies.

4. Maintenance Contract Stack. As the deployed bus fleet grows, so does the recurring maintenance revenue. This is a flywheel — the older the fleet, the higher the annuity income.

5. Index Inclusion. Part of Nifty EV & New Age Automotive. Any broader index inclusion event triggers mandatory fund buying.

SECTION 6 — SMART MONEY SIGNAL

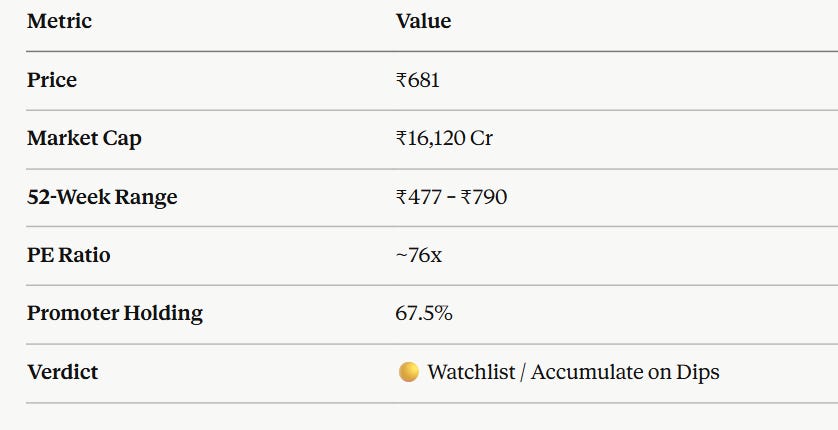

Promoters hold 67.5% of the company. That’s not just confidence — it’s ownership density. When a founding family holds two-thirds of a business, they’re not distracted by quarterly noise.

The stock has bounced 43% from its 52-week low of ₹477 — that kind of recovery from a bottom, while operating numbers are accelerating, rarely happens without institutional interest building quietly.

EBITDA growing faster than revenue is a classic signal that someone, somewhere, has started to fix the cost structure — or that operating leverage is kicking in. Either way, it’s a signal worth tracking.

The stock is part of the Nifty EV & New Age Automotive index — a relatively new thematic construct that fund managers are beginning to benchmark against. Passive flows will follow as AUM grows.

SECTION 7 — RISKS

Be clear-eyed about these.

1. Valuation is not cheap. At ~76x PE, you’re paying for growth that must deliver. Any earnings miss, any order delay, and the stock can reprice fast. This is not a value buy. It’s a growth bet.

2. Debtor Days Have Ballooned. Debtor days reportedly jumped from 82 to 131 days. That’s a working capital warning sign. Government clients are slow payers. If this stretches further, cash flow deteriorates even as profits grow.

3. EV Bus Execution Risk. Building EVs at scale is operationally complex. Supply chain, battery sourcing, charging infrastructure — any disruption flows through to margin and delivery timelines.

4. Cyclicality in Components. The auto components business is tied to OEM production cycles. A slowdown in passenger vehicle or commercial vehicle volumes hits the legacy business.

5. Competition Intensifying. Tata Motors, Olectra, and new entrants are all fighting for the same government EV bus pie. Market share is not guaranteed.

SECTION 8 — FINAL VERDICT

Here’s the honest case.

This is not a company to blindly buy today. The valuation reflects some of the optimism already.

But this IS a company to track with intensity. Because the setup — a profitable legacy cash engine + an EV infrastructure play with government tailwinds + promoter-controlled capital allocation — is rare.

When a company expands EBITDA margins from 11% to 12.4% while simultaneously scaling a capex-heavy new business, it means the core is getting stronger, not weaker.

If margin expansion continues to 14–15% over the next two years, and if EV bus order intake accelerates — this is a fundamentally different earnings story by FY28.

The window to build a position before the story becomes consensus is not infinite.

Miss it, and you’ll be reading about it when it’s already priced in.