Overcoming Investment Fears: How to Beat the "I'm Not Rich Enough" Myth

Last week, I was reviewing portfolio allocations for a client who started investing with just ₹2,000 monthly back in 2015. Today, that systematic approach has grown into a corpus worth ₹12 lakhs. What struck me wasn't the absolute number—it was how she almost didn't start at all because she thought her salary of ₹35,000 was "too small" for serious investing.

Sound familiar?

The ₹500 Fallacy

Here's something Wall Street won't tell you: Most wealth isn't built by the ultra-rich throwing crores around. It's built by regular people consistently investing modest amounts over decades. I call this the "₹500 fallacy"—the belief that small amounts don't matter.

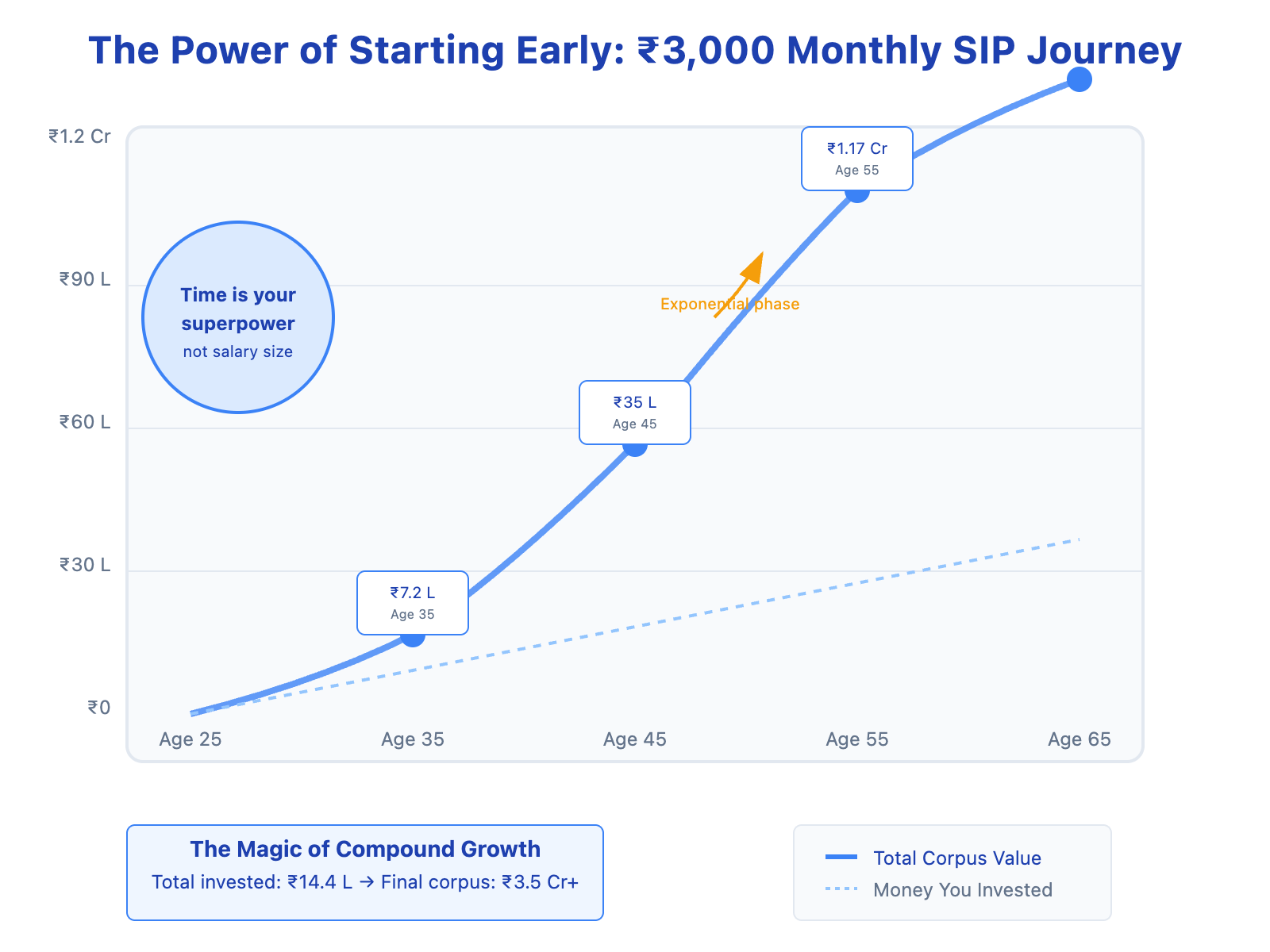

Consider this: A 25-year-old software engineer investing ₹3,000 monthly in equity mutual funds (assuming 12% annual returns) would accumulate approximately ₹1.17 crores by age 55. That's wealth-building territory, not pocket change.

But here's where it gets interesting—and where most people get it wrong.

The Compound Interest Blind Spot

Everyone talks about compound interest, but few understand its psychological dimension. When you start with small amounts, the first few years feel... underwhelming. Your ₹3,000 monthly SIP might grow to ₹40,000 after the first year. Not exactly life-changing, right?

Wrong. That's exactly when compound interest is doing its most important work—not in the returns, but in building the habit.

I once tracked a cohort of fresh engineering graduates from a major IT services company. Those who started investing within their first year of employment—regardless of amount—had 3x higher investment corpus after five years compared to those who waited for their "big salary hike."

The Perfectionism Trap

Here's a pattern I've observed across hundreds of portfolios: Engineers and developers are particularly susceptible to analysis paralysis. You research for months, comparing expense ratios, analyzing fund performance, waiting for the "perfect" entry point.

Meanwhile, your colleague who started a basic SIP in a decent large-cap fund six months ago is already ahead.

The market doesn't care about your salary bracket. It cares about your time in the market.

Breaking the Minimum Investment Myth

Let's address the elephant in the room: Most mutual funds in India have minimum SIP amounts of ₹500-1,000. That's less than what many of us spend on weekend food delivery. Yet somehow, this feels "too small" to matter.

Here's a reality check from my portfolio management days: I've seen ₹1,000 monthly SIPs outperform ₹50,000 lump-sum investments simply because of timing and consistency. The smaller investor stayed disciplined through market volatility while the lump-sum investor panicked during corrections.

The Fresh Graduate's Secret Weapon

You have something that even high-net-worth individuals can't buy: time. A 40-year-old director starting their investment journey with ₹50,000 monthly needs to take significantly more risk to achieve the same corpus as a 23-year-old starting with ₹5,000 monthly.

Time is your multiplier, not your salary.

The Real Investment Minimum

After analyzing thousands of investment journeys, I've identified the real minimum investment amount: whatever you can commit to for at least 5 years without touching it. For some, that's ₹1,000. For others, it's ₹10,000. The amount is irrelevant—the commitment isn't.

Start with what feels comfortable, even if it's embarrassingly small. You can always increase it later (and you will, as your income grows).

The Automation Advantage

Here's a tactical insight: Set up automatic transfers to your investment accounts on the same day you receive your salary. This isn't about budgeting—it's about removing the monthly decision fatigue of "should I invest this month?"

Your future self will thank you for making investment decisions on autopilot.

Moving Forward

Stop waiting for the perfect salary, perfect fund, or perfect market timing. The best investment strategy is the one you'll actually follow. Start small, start now, and let time do the heavy lifting.

Your journey from "I'm not rich enough to invest" to "I'm building wealth systematically" begins with your next paycheck. The question isn't whether you have enough money to invest—it's whether you have enough time to waste by not investing.

What's one investment decision you've been postponing because the amount feels too small? Sometimes the most profound wealth-building happens in the least dramatic moments.