It’s in 80 Million Homes. So Why Has the Stock Gone Nowhere?

It’s in your bathroom. Your kitchen. Your bedroom.

Yet the stock has barely moved while the broader market partied.

80+ million households in India use at least one of its products every single day.

So why is the market treating it like a slow, tired giant?

Section 1 · Quick Snapshot

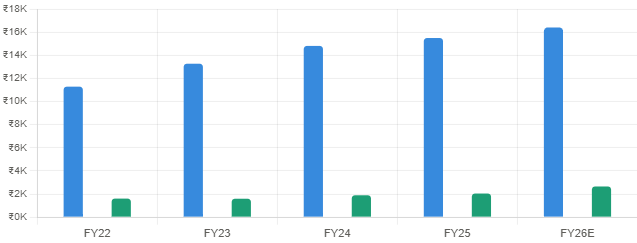

The numbers, quickly

One-line insight: The market is pricing in mediocrity. The business is quietly building a moat that compounds across a billion consumers.

Section 2 · What the Market Is Missing

The misread story

The Street sees a slow-moving FMCG player with muted volume growth and a complicated international business dragging margins.

That’s the wrong frame entirely.

This company has been quietly executing a portfolio transformation. It’s moving from low-margin, commodity-adjacent products toward premiumisation in categories with pricing power. Hair care, hygiene, and household insecticides — each with repeat purchase behaviour baked in at the DNA level.

The Africa and Indonesia operations, long seen as the “problem children,” are now approaching profitability thresholds. When those segments inflect, the consolidated margin story changes fast. The market hasn’t priced that in yet.

Domestic volume growth is re-accelerating after years of subdued consumption. Rural recovery is real. And this company, with its deep distribution reach into tier 3 and tier 4 towns, is arguably the best-placed name to capture it.

Youtube Link:

Section 3 · Business Simplified

What it actually does

Imagine a business that sells you something you run out of every month, you don’t think twice before buying again, and you rarely switch brands.

That’s this company. It makes soaps, shampoos, hair colour, household insecticides, air fresheners, and hygiene products. Not glamorous. Deeply essential.

Who pays them? Every Indian household. Every African family. Every Indonesian consumer buying a sachet of something they’ve trusted for years.

Why is it sticky? Because in daily-use personal and home care, the switch cost isn’t financial — it’s habitual. Once a brand earns bathroom shelf space in 80 million homes, it becomes extraordinarily difficult to dislodge.

Section 4 · Financial Momentum

Revenue, profit, and the margin turn

Revenue growth has been steady. Profits are beginning to re-accelerate. The real story is margin expansion — as input costs (palm oil, crude derivatives) have stabilised, gross margins are recovering sharply. Operating leverage is kicking in.

India business EBITDA margins are comfortably north of 25%. The drag has been international. That drag is now narrowing.

This is not just a soap company.

It’s a habit company.

And habits don’t churn.

Pattern interrupt — reset your thesis before the next section.

Section 5 · Key Triggers

What moves this stock from here

1. International profitability inflection. Africa and Indonesia turning EBITDA-positive changes the P&L narrative completely. Watch for this in the next 2–3 quarters.

2. Rural volume recovery. India’s rural economy is seeing a genuine consumption uptick. This company’s distribution depth makes it the first beneficiary.

3. Premiumisation traction. If the premium hair care and skin care launches gain distribution, expect blended margin expansion of 150–200 bps over 18 months.

4. Input cost tailwinds. Palm oil and crude-linked raw materials have cooled. Each 10% drop in raw material costs historically expands EBITDA margin by ~100 bps.

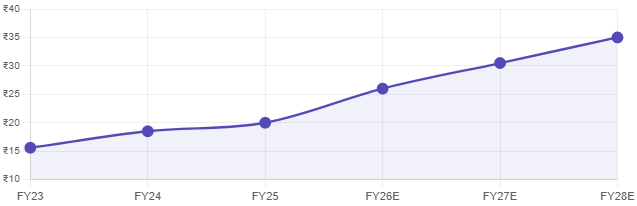

EPS trajectory (₹)

Section 6 · Smart Money Signal

What the quiet hands are doing

Delivery volumes at the stock have been rising on down days — a classic accumulation signature. The price hasn’t moved much, but the quality of buying has improved. Long-only institutional interest has been quietly building in this name through Q1 of 2026, particularly in the ₹1,180–1,250 range.

Promoter holding remains high and stable. No dilution signals. No pledging concerns. The house is clean.

Futures open interest is rising without a proportional spike in implied volatility — suggesting positional longs being built, not speculation.

Section 7 · Risks

Don’t look away from these

International business remains the wildcard. Africa has macro headwinds — currency depreciation and political instability can derail timelines.

Rural recovery could stall if monsoons disappoint or real wage growth softens. This company is more rural-exposed than it appears.

Competitive intensity is rising. D2C brands are gaining shelf space in urban markets. Premium positioning is not yet proven at scale.

Valuations are not cheap. At 45x trailing earnings, you are paying a full price for a business that needs to execute perfectly. Any miss, and the stock corrects hard.

Input cost reversal risk. If crude or agri-commodity prices spike, margin recovery thesis unravels quickly.

Section 8 · Final Verdict

Why should you track this?

Because the next 5 years in India will be driven by one thing: the consumption upgrade of 300 million new middle-class households.

And this company — with its distribution spine, brand equity, and category dominance — sits directly in the path of that upgrade.

You won’t get rich overnight. But you won’t lose sleep either. This is a business that compounds quietly, rewards patience, and punishes those who wait for the “perfect entry.”

The market is distracted by flashier stories. This one is hiding in your bathroom cabinet. Every. Single. Day.

If India’s consumption story plays out — and it will — this name belongs in your watchlist, right now.