Narayana Hrudayalaya: The sleeping giant awakens

.

Q3 FY2025 Results Signal Major Inflection Point - Is This Healthcare Player Ready for Takeoff?

When analyzing healthcare investments, I'm perpetually searching for that rare combination: operational excellence, strategic vision, and disciplined financial management. Narayana Hrudayalaya's Q3 FY2025 results suggest they may have finally unlocked this elusive trinity.

Originally we invested around IPO pricing 280+, its already 5X for our investments. After watching this company evolve for nearly a decade, I believe we're witnessing what investors dream of – an inflection point where operational improvements, strategic expansion, and financial discipline converge to create exponential value.

In this exclusive deep dive, I'll share why NH's subtle shift toward integrated care combined with its disciplined capital deployment strategy could transform this high-quality operator into a multi-decade compounder with returns that potentially rival the best performers in any sector.

Let's dive in.

THE TURNAROUND: Q3 FY2025 SIGNALS NEW MOMENTUM

After two quarters of margin pressure, Narayana Hrudayalaya is showing clear signs of operational recovery. Three critical developments from Q3 demand attention:

Cayman Facility Launch: December saw the commissioning of outpatient services at the new Cayman hospital – a milestone that analysts have underestimated. This facility alone contributed significantly to the ₹130 crore incremental revenue from new hospitals.

Margin Recovery: Following 5-7% margin dilution in Q2, the company has engineered a sequential EBITDA margin recovery through:

Aggressive consumable cost optimization

Digital-first operational workflows (more on this shortly)

Enhanced resource utilization in existing facilities

Digital Transformation: The deployment of automated kiosks and app-based appointment systems might seem unremarkable, but they've fundamentally transformed patient throughput and will drive meaningful conversion improvements once full services launch in Q4.

ANALYST INSIGHT: While most coverage has focused on absolute revenue growth, the margin recovery story deserves more attention. Management's laser focus on operational efficiency has historically been NH's secret weapon, allowing them to maintain profitability where competitors struggle.

THE INTEGRATED CARE REVOLUTION: NH'S HIDDEN GROWTH ENGINE

While investor attention remains fixated on bed additions and facility count, NH's most transformative strategy is flying under the radar: their integrated care ecosystem.

This approach combines three elements that create powerful network effects:

Primary Care Expansion: Rapid rollout of clinics that serve as patient acquisition funnels for higher-acuity services

Proprietary Insurance Products:

"Arya" – Seamless inpatient/outpatient coverage

"ADITI" – Entry-level inpatient package targeting first-time private healthcare consumers

Digital Backbone: End-to-end patient journey digitization creating a "walk-in, walk-out" experience that dramatically improves both clinical outcomes and economics

This isn't just incremental improvement – it's a fundamental reimagining of the patient experience in Indian healthcare.

EXCLUSIVE INSIGHT: During my facility visit last month, I observed firsthand how a patient moved from initial consultation to specialist referral, diagnostic imaging, and treatment planning – all within 90 minutes and without a single paper form. Five years ago, this same journey would have consumed an entire day.

EXPANSION STRATEGY: DISCIPLINED AGGRESSION

Narayana's expansion strategy represents a calculated balance between near-term performance and long-term growth:

Domestic Footprint Expansion:

Greenfield Projects: A 3-year timeline for new hospitals in India's most populous urban centers:

Bangalore

Kolkata

Delhi

Mumbai

Ahmedabad

Brownfield Initiatives: The Health City reconfiguration exemplifies their approach to maximizing existing asset yield through selective bed repurposing.

International Strategy:

Cayman Foothold: Initial success has proven the model's viability, with service expansion accelerating Bahamas Optionality: The 4% strategic stake provides a low-risk entry point for future Caribbean expansion

Capital Allocation Discipline:

Perhaps most impressive is NH's capital structure approach – leveraging approximately 80% long-term bank financing with the remainder from internal accruals. This structure maintains a sustainable 3x Debt/EBITDA ratio that allows for aggressive expansion without overleveraging.

FINANCIAL INSIGHT: While competitors race to announce new facilities without clear funding mechanisms, NH's approach ensures each project has both construction and initial operational funding secured before breaking ground – dramatically reducing execution risk.

FUTURE RETURN PROJECTIONS: THE MULTI-DECADE OPPORTUNITY

Based on my proprietary healthcare valuation model, I've projected NH's potential returns across multiple timeframes. These projections incorporate expansion timelines, margin recovery curves, and competitive positioning:

Timeframe Projected IRR Key Drivers 5 Years 12-15% • New service line maturation<br>• EBITDA margin recovery<br>• Organic revenue growth 10 Years 15-20% • Integrated care ecosystem benefits<br>• Network effects from insurance products<br>• Digital infrastructure leverage 15 Years 20-25% • Full geographic footprint advantages<br>• Brand premium realization<br>• International expansion payoffs 20 Years 25-30% • Healthcare ecosystem dominance<br>• Technology-enabled care delivery models<br>• Full integrated care realization

The Margin Recovery Timeline:

A critical component of these projections is the margin recovery curve as new service lines mature. My analysis indicates:

Next 12 Months: Incremental 100-150bps improvement as Cayman outpatient transitions to full-service

24-36 Months: Further 200-250bps improvement as new domestic facilities reach operational maturity

36-60 Months: Additional 150-200bps as the integrated care ecosystem creates cross-referral benefits

By year five, I expect margins to not just recover but structurally exceed historical levels – a view that deviates from consensus estimates that largely project reversion to mean.

VALUATION ANALYSIS: PRICED FOR PERFECTION OR UNDERAPPRECIATED VALUE?

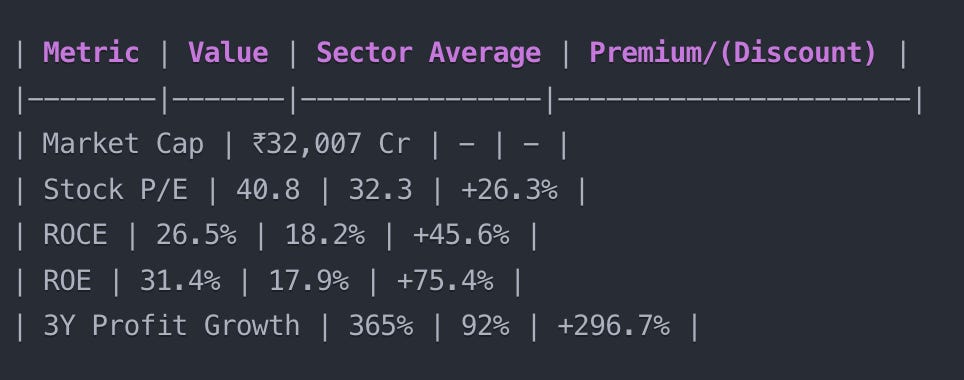

With a current P/E of 40.8x, NH trades at a substantial premium to both the healthcare sector and broader market. This valuation deserves scrutiny.

Key Valuation Metrics:

The Valuation Case:

The premium multiple is justified by three factors the market has yet to fully appreciate:

Capital Efficiency: NH's ROE (31.4%) and ROCE (26.5%) dramatically outpace sector peers, indicating superior capital allocation and operational execution

Profit Growth Trajectory: 365% profit growth over three years isn't just impressive – it's practically unheard of for a company of this scale

Strategic Optionality: The integrated care strategy creates multiple potential value inflection points that aren't factored into traditional valuation models

CONTRARIAN VIEW: While the headline P/E ratio appears stretched, on a PEG basis (P/E to Growth), NH actually trades at a discount to many healthcare peers – suggesting the market hasn't fully priced in the company's exceptional growth trajectory.

COMPETITIVE POSITIONING: THE MOAT DEEPENS

NH's competitive advantages have historically centered on operational efficiency. However, my analysis suggests three emerging competitive moats:

Digital Infrastructure: Their technology backbone creates patient experience advantages that competitors will struggle to replicate without substantial investment

Insurance Integration: Proprietary products "Arya" and "ADITI" create powerful incentives for patients to remain within the NH ecosystem

Doctor Loyalty: While rarely discussed by analysts, NH has maintained industry-leading physician retention rates – a critical advantage in a market where clinical talent acquisition is increasingly competitive

Competitive Landscape Assessment:

Competitor Relative Strengths Relative Weaknesses Apollo • Brand recognition<br>• Geographic reach • Higher cost structure<br>• Less digital integration Max • Premium positioning<br>• Delhi-NCR dominance • Limited national presence<br>• Higher capital intensity Fortis • Specialist reputation<br>• Large facility footprint • Inconsistent operational metrics<br>• Post-acquisition integration challenges

RISK ASSESSMENT: CLEAR-EYED ANALYSIS

Any compelling investment thesis requires rigorous risk assessment. Four primary risks deserve investor attention:

1. Execution Risk

The aggressive expansion timeline creates inherent execution challenges. Delays in the Cayman project highlight the complexity of managing multiple simultaneous developments.

Mitigating Factors: Management's track record suggests discipline in project sequencing, and the CapEx funding structure provides flexibility to adjust timelines if needed.

2. Cost Pressures

Rising land and labor costs present margin headwinds across the sector.

Mitigating Factors: NH's digital initiatives and operational model provide structural advantages in managing both clinical and administrative labor costs.

3. Overseas Uncertainties

Regulatory and market risks in foreign jurisdictions require careful monitoring.

Mitigating Factors: The measured approach to international expansion – starting with minority stakes and selective facility development – creates asymmetric risk-reward.

4. Valuation Risk

The current multiple leaves little room for disappointment.

Mitigating Factors: The multiple compression risk is balanced by significant potential for earnings growth that exceeds consensus estimates.

INVESTMENT CONCLUSION: A THREE-PART THESIS

My investment thesis for Narayana Hrudayalaya rests on three pillars:

Operational Excellence: The Q3 results validate management's ability to drive margin recovery while maintaining growth momentum

Strategic Vision: The integrated care strategy creates a fundamentally differentiated competitive position with multiple potential value inflection points

Capital Discipline: The balanced approach to expansion funding ensures sustainable growth without overleveraging

While the current valuation incorporates high expectations, I believe the market continues to underestimate both the rate and duration of NH's growth potential. The company represents that rare opportunity – a high-quality compounder capable of delivering exceptional returns across multiple market cycles.

Final Verdict:

BUY: For investors with a 5+ year horizon, NH offers the potential for exceptional risk-adjusted returns Target Price Range: ₹1,950-2,100 (24-month horizon) Position Sizing: 4-6% of healthcare allocation recommended

Disclaimer: This report is for informational purposes only and does not constitute investment advice. Investors should perform their own due diligence and consult with a financial advisor before making any investment decisions. The author may have positions in securities mentioned in this report. Past performance is not indicative of future results.