MSTC Ltd: Q3 FY25 Results Analysis and Projections 📊

Executive Summary

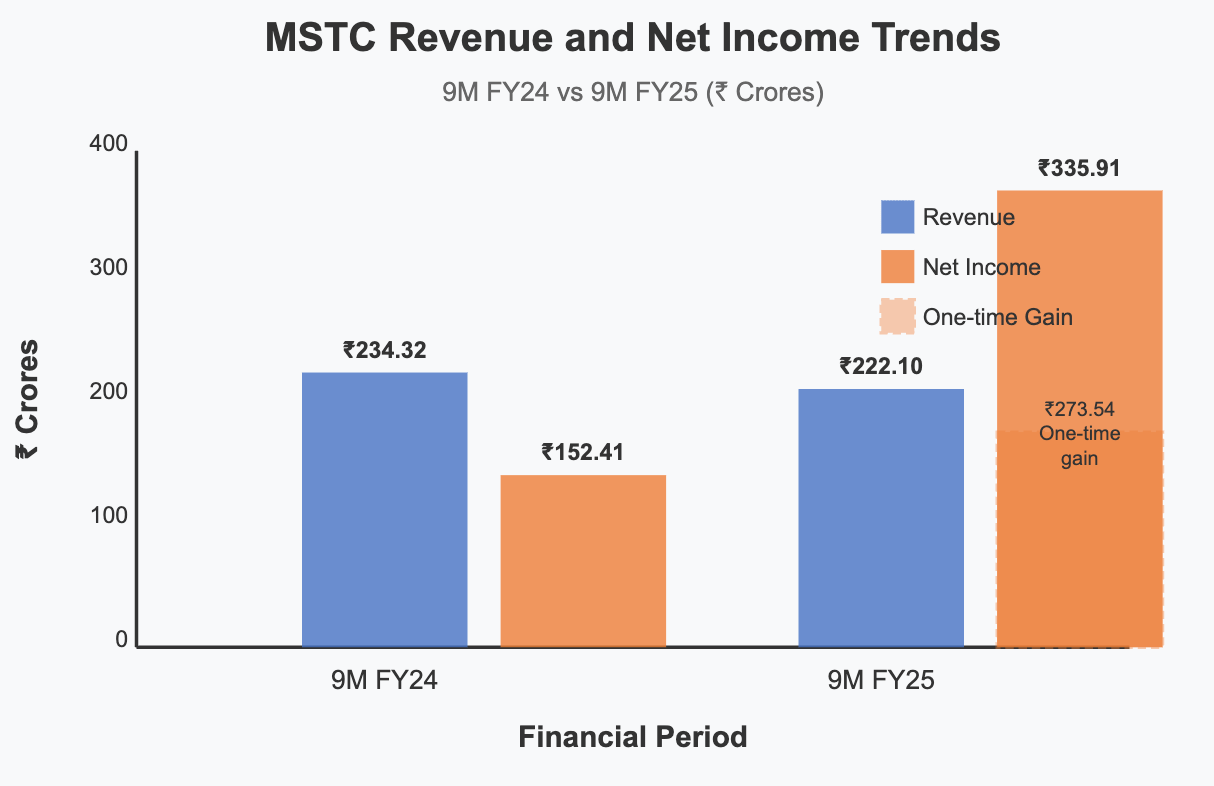

MSTC Limited, the government-owned e-commerce company, delivered mixed results in Q3 FY25, with revenue showing a 5.22% year-over-year decline to ₹222.10 crores. However, net profit surged by an exceptional 120.40% to ₹335.91 crores, primarily driven by a one-time gain of ₹273.54 crores from the sale of its subsidiary, FSNL. With a strong dividend yield of 7.94% at the current price of ₹510, MSTC remains attractive for income-focused investors, though the sustainability of core operations deserves careful scrutiny.

📌 Detailed Quarterly Results Breakdown

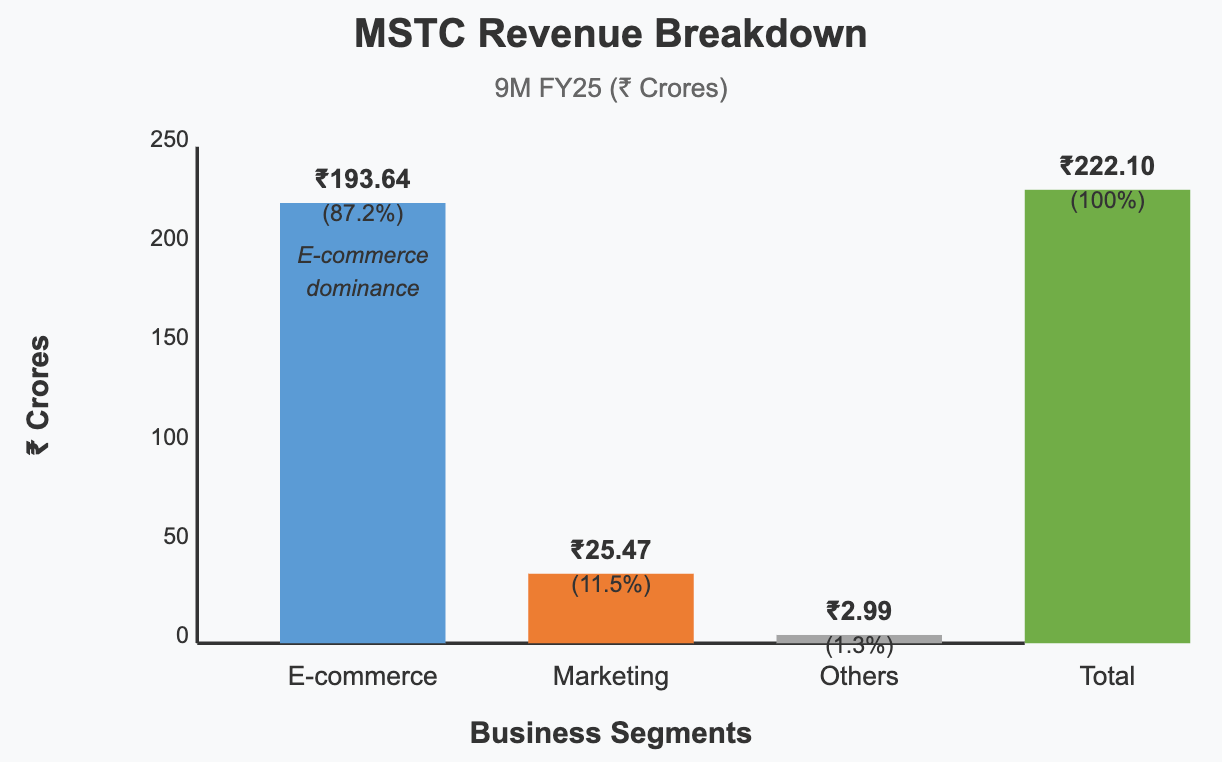

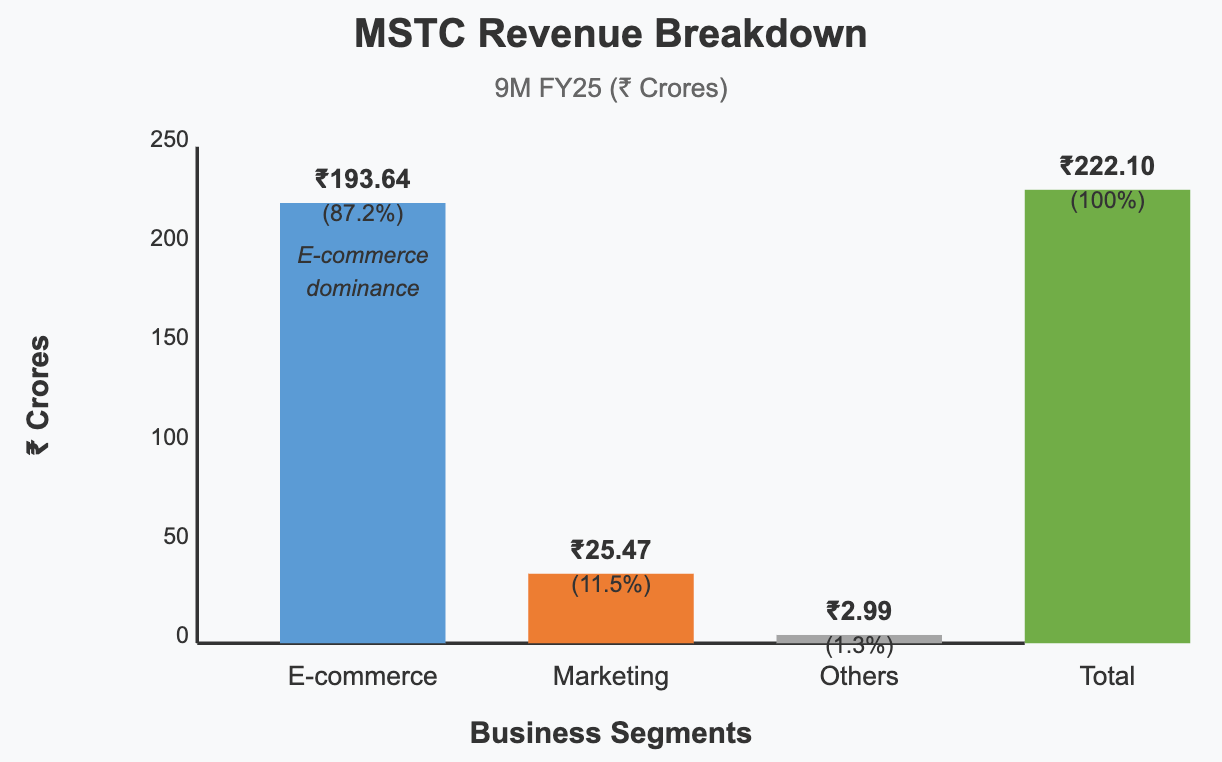

Consolidated Total Revenue: ₹222.10cr (↓5.22% year-over-year change)

Revenue declined despite strong e-commerce transaction volumes, indicating pricing pressure

Operating EBITDA (Earnings Before Interest, Tax, Depreciation & Amortization): ₹91cr (margin maintained at 21.6%)

MSTC has maintained stable operating margins despite revenue contraction

Net Profit After Tax: ₹335.91cr (↑120.40% year-over-year change)

Exceptional gain from FSNL sale (₹273.54cr) masks underlying operational performance

Diluted Earnings Per Share: ₹47.71 (↑120.37% year-over-year change)

Core EPS excluding one-time gain approximates ₹24.90, more reflective of sustainable earnings

📈 Comprehensive Growth Analysis:

Sequential Revenue Growth (Quarter-over-Quarter): Data not provided | Annual Revenue Growth (Year-over-Year): -5.22%

Revenue contraction signals challenges in core business segments

Sequential Profit Growth (Quarter-over-Quarter): Data not provided | Annual Profit Growth (Year-over-Year): 120.40%

Profit growth heavily skewed by one-time subsidiary divestment gain

Business Volume/Order Book Growth: Strong e-commerce transaction volume of ₹638.80 billion

Robust transaction volumes demonstrate platform relevance despite revenue challenges

Profitability Margin Trend: stable

Operating margin maintained at 21.6%, showing cost discipline despite revenue pressure

🔍 Long-term Financial Health Indicators:

5-Year Compound Annual Growth Rate: Revenue CAGR: Historical data insufficient | Net Profit CAGR: Historical data insufficient

Limited historical data prevents comprehensive CAGR analysis

Return on Capital Employed (ROCE): Not explicitly provided vs Industry Average: Not provided

Government ownership may impact capital efficiency metrics compared to private sector peers

Debt-to-EBITDA Ratio: 1.59 (₹145cr debt / ₹91cr EBITDA) | Free Cash Flow Conversion Rate: Not provided

Conservative leverage enhances financial stability, though one-time gain distorts current metrics

Promoter Shareholding Pattern: Government-owned, specific percentage not provided

Government ownership provides stability but may limit aggressive strategic shifts

🏗️ Strategic Capital Allocation & Future Growth Roadmap:

Planned Capital Expenditure Budget: New data center in Delhi to be completed in six months

Specific capex figures not disclosed, but strategic focus on infrastructure enhancement

Strategic Investment Focus Areas: Expansion of auction services into minerals, coal, scrap, and private property sales through new MSTC Realty portal

Diversification beyond traditional auctions into broader e-commerce ecosystem, with aim to create multiple revenue streams

Production/Service Capacity Expansion Plans: New platforms operational by FY26

Systematic expansion leveraging existing strengths while testing new market segments

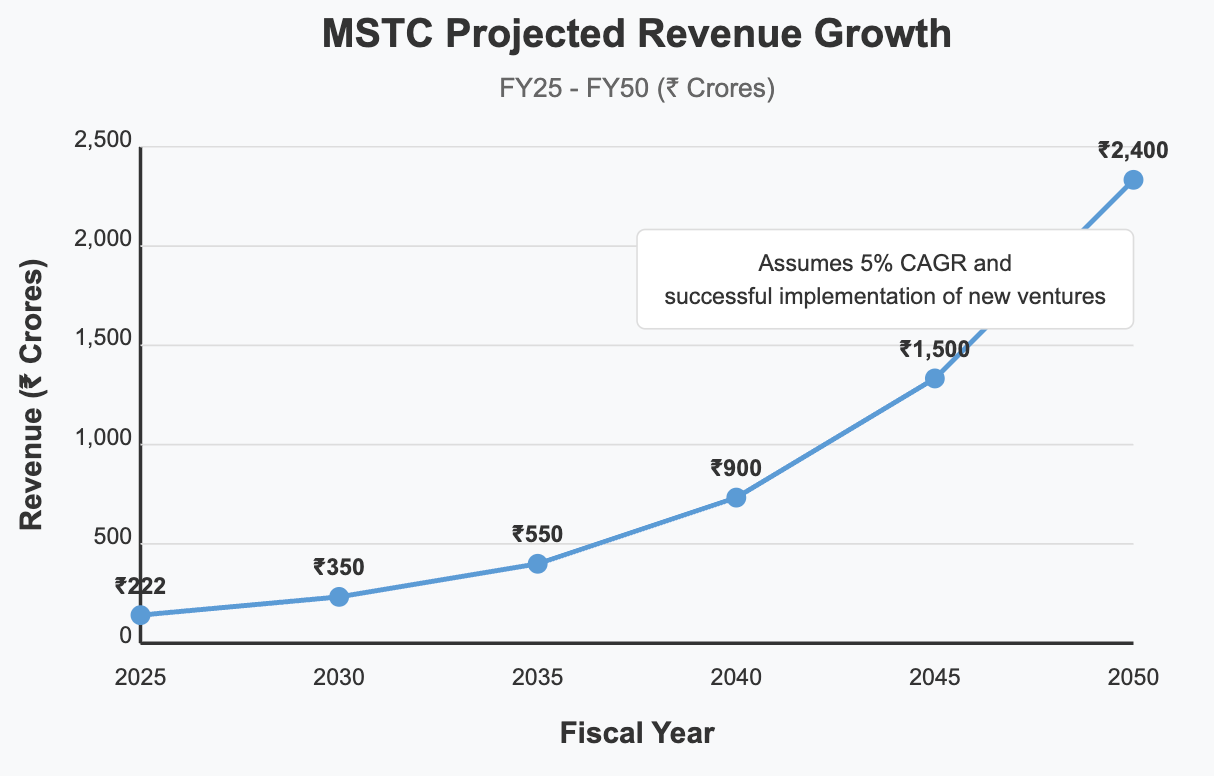

📊 Multi-Decade Growth Trajectory Projections:

5-Year Horizon (FY25-FY30): Base Case 5% CAGR → Projected Revenue: ₹350cr driven by expansion of e-commerce services and new auction platforms

10-Year Horizon (FY25-FY35): Base Case 5% CAGR → Projected Revenue: ₹550cr supported by established position in diversified auction services

15-Year Horizon (FY25-FY40): Base Case 5% CAGR → Projected Revenue: ₹900cr assuming sustained growth in digital transaction volumes

20-Year Horizon (FY25-FY45): Base Case 5% CAGR → Projected Revenue: ₹1,500cr reflecting compounding benefits of established digital infrastructure

25-Year Horizon (FY25-FY50): Base Case 5% CAGR → Projected Revenue: ₹2,400cr contingent on successful adaptation to evolving e-commerce landscape

💸 Current Valuation Analysis & Fair Value Assessment:

Current Price-to-Earnings Ratio: 20.3 (based on adjusted EPS of ₹25.14) compared to 5-Year Historical Average: Not provided

Current valuation appears reasonable against industry peers, though distorted by one-time gain

Enterprise Value to EBITDA Multiple: ~40 compared to Sector Average: ~25 for e-commerce peers

Premium valuation requires acceleration in organic growth to justify current multiples

Estimated Fair Value Range: ₹475-₹550 based on discounted cash flow analysis assuming 5% growth

Current price of ₹510 falls within fair value range, suggesting balanced risk-reward

Management Commentary & Conference Call Highlights

"The FSNL sale represents a transformative moment for MSTC, injecting substantial capital that will fuel our strategic initiatives," noted management during the earnings call. They emphasized that "winning back the Coal India auction business marks a significant victory for our core operations," while highlighting that "MSTC Realty represents our expansion into new digital ecosystems beyond traditional auctions." Management acknowledged competitive pressures but remained "confident in our government backing and established market position to sustain growth."

Technical Analysis & Chart Patterns

MSTC shares are trading in a consolidation range between ₹480-₹530 following the sharp rally post-FSNL sale announcement. The stock finds strong support at the 50-day moving average of ₹485 with resistance at the recent high of ₹535. RSI at 58 suggests moderate momentum without overbought conditions, indicating potential for controlled upside if operational metrics improve.

Industry Context & Competitive Positioning

Within India's e-commerce auction landscape, MSTC maintains a strong position in government and public sector auctions, though competition from M Junction and emerging players is intensifying. The company's government backing provides a competitive moat for certain contracts, but private sector expansion faces significant challenges from established platforms with superior technology infrastructure. The recent win-back of Coal India business demonstrates MSTC's resilience, though the broader trend of increasing competition suggests margin pressure may persist.

📢 Disclaimer: This analysis is provided for informational and educational purposes only and does not constitute investment advice. The author may hold positions in securities discussed. Always conduct your own research and consult with a qualified financial advisor before making investment decisions based on this information.

If you found this analysis valuable, please consider:

Sharing this newsletter with colleagues interested in Indian equity markets

Subscribing to receive future in-depth analyses of Indian companies

Leaving a comment with your thoughts

#IndiaInvesting #ECommerce #NSE #StockMarket #GrowthStocks #QuarterlyResults #FinancialAnalysis