Micro/Small Cap (<₹5000Cr), High Growth, Margin Expansion

JBM Auto Ltd. - Equity Research Report

1. Investment Thesis & Summary

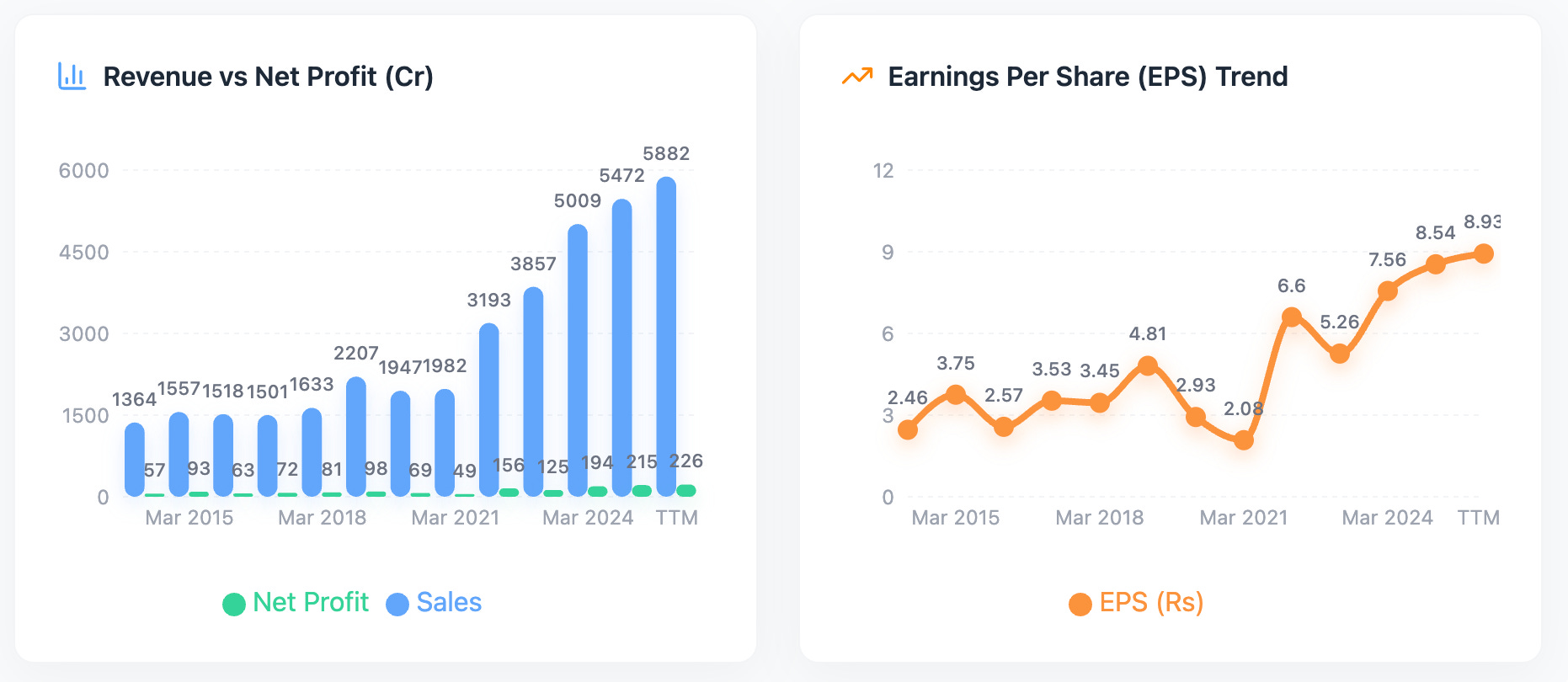

JBM Auto Ltd. (JBM Auto) presents a compelling investment case, strategically transitioning from a robust automotive component manufacturer to a pivotal player in India’s burgeoning electric vehicle (EV) ecosystem, specifically within the electric bus (E-bus) segment. This forward-looking pivot has substantially invigorated the company’s financial trajectory, evidenced by its aggressive revenue expansion and significant uplift in profitability. The company’s integrated approach, encompassing E-bus manufacturing, charging infrastructure, and comprehensive operational support, positions it uniquely to capitalize on India’s strong governmental push for sustainable public transportation and the escalating demand from State Transport Undertakings (STUs). The latest financial data confirms this momentum, with TTM (Trailing Twelve Months) sales reaching ₹5882 Cr and a corresponding EPS of ₹8.93, indicating strong operational execution. We believe JBM Auto is poised for sustained, high-growth, driven by a deep order book in E-mobility, continuous product innovation, and its established expertise in automotive manufacturing, making it an attractive long-term investment, albeit potentially at a premium valuation reflecting its growth prospects in a sunrise industry.

2. Business Model & Operations

JBM Auto operates through two primary and synergistic business verticals:

Automotive Components: This segment forms the historical foundation and continues to be a stable revenue generator. JBM Auto functions as a Tier-1 supplier of a diverse range of critical components and systems to prominent Indian and global Original Equipment Manufacturers (OEMs) across passenger vehicles, commercial vehicles, and two-wheelers. Its product portfolio includes sophisticated sheet metal components, welded assemblies, chassis and suspension parts, body structures, and precision tools & dies. The company leverages advanced manufacturing technologies, automation, and extensive in-house R&D capabilities to deliver high-quality, high-precision components.

Electric Vehicles (E-mobility): This segment represents JBM Auto’s strategic growth engine and future focus. The company is actively involved in the design, development, manufacturing, and sale of electric buses under its ‘ECO-LIFE’ brand. JBM Auto’s value proposition in E-mobility extends beyond vehicle manufacturing to a comprehensive ecosystem approach, which includes:

E-Bus Manufacturing: Producing a variety of E-bus models suitable for urban transit, staff transportation, and intercity travel.

Charging Infrastructure: Developing, deploying, and managing charging solutions to support its E-bus fleet and broader EV adoption.

Battery Technology Solutions: Actively exploring and implementing advanced battery and energy management systems.

Operational & Maintenance Services: Providing end-to-end support for its E-buses, frequently through Gross Cost Contract (GCC) models with STUs, where JBM Auto manages the entire operational lifecycle of the buses against a per-kilometer remuneration.

The inherent synergies between these two segments are critical. The robust manufacturing infrastructure, supply chain expertise, and R&D capabilities developed in the automotive components business provide a strong competitive advantage and facilitate vertical integration within E-bus production, enhancing cost efficiency and speed to market.

3. Historical Financial Review

JBM Auto has exhibited a distinct two-phase financial performance trajectory, with a significant acceleration in revenue and profitability in recent years driven by its E-mobility foray.

Annual Performance Analysis (Mar 2014 - TTM):

Revenue Growth:

From Mar 2014 (₹1364 Cr) to Mar 2021 (₹1982 Cr), sales growth was moderate, exhibiting a CAGR of approximately 5.5%, interspersed with minor fluctuations, including a slowdown in Mar 2020 due to external factors.

However, the period post-Mar 2021 marks a pivotal inflection point. Sales surged by an impressive 61% from ₹1982 Cr in Mar 2021 to ₹3193 Cr in Mar 2022. This robust growth continued, with sales reaching ₹3857 Cr in Mar 2023 (20.8% YoY growth) and further accelerating to ₹5009 Cr in Mar 2024 (29.9% YoY growth).

The Trailing Twelve Months (TTM) sales stand at a significant ₹5882 Cr, reflecting strong, sustained momentum and an annualized growth rate of approximately 17% compared to Mar 2024.

Profitability (Net Profit & EPS):

Net Profit and EPS largely paralleled the revenue trends. Net profit fluctuated between ₹57 Cr (Mar 2014) and a peak of ₹98 Cr (Mar 2019), subsequently declining to ₹49 Cr (Mar 2021). EPS mirrored this, ranging from ₹2.46 (Mar 2014) to ₹4.81 (Mar 2019), settling at ₹2.08 (Mar 2021).

Post-Mar 2021, profitability witnessed a dramatic turnaround. Net profit catapulted to ₹156 Cr in Mar 2022 (a phenomenal 218% increase over Mar 2021), albeit with a temporary moderation to ₹125 Cr in Mar 2023.

The company delivered strong earnings in Mar 2024, reporting a net profit of ₹194 Cr and an EPS of ₹7.56.

The latest TTM data reveals a net profit of ₹226 Cr and an EPS of ₹8.93, underscoring robust earnings acceleration. The implied TTM net profit margin has expanded to approximately 3.9%, a notable improvement from 2.5% in Mar 2021.

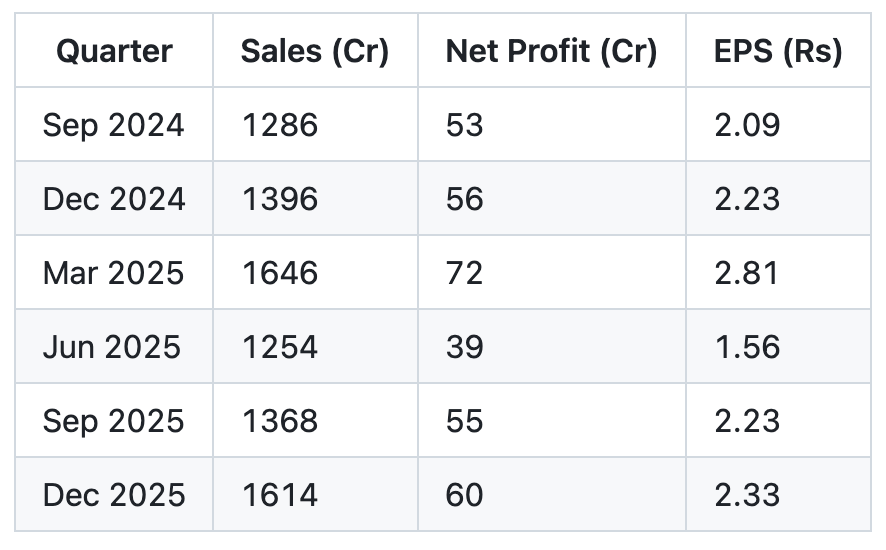

Recent Quarterly Performance Review (Mar 2025 - Dec 2025):

The latest four quarters confirm the company’s operational strength and sequential recovery.

Sales:

Mar 2025: ₹1646 Cr

Jun 2025: ₹1254 Cr

Sep 2025: ₹1368 Cr

Dec 2025: ₹1614 Cr

Quarterly sales demonstrate a healthy rebound from the seasonal or project-related dip in Jun 2025, with Dec 2025 sales almost matching the peak of Mar 2025. This indicates a consistent pipeline and efficient execution.

Net Profit & EPS:

Mar 2025: Net Profit ₹72 Cr, EPS ₹2.81

Jun 2025: Net Profit ₹39 Cr, EPS ₹1.56

Sep 2025: Net Profit ₹55 Cr, EPS ₹2.23

Dec 2025: Net Profit ₹60 Cr, EPS ₹2.33

Net profit and EPS experienced a temporary contraction in Jun 2025, but have since shown sequential recovery and growth in the Sep and Dec 2025 quarters. The aggregated TTM EPS of ₹8.93, derived directly from these four quarters, highlights the company’s strong, annualized earning power.

4. Growth Drivers & Catalysts

JBM Auto’s future growth is strategically aligned with macro-economic trends and specific industry catalysts:

Government Mandate for E-mobility: India’s aggressive clean energy and decarbonization goals, manifested through policies like the FAME-II scheme and various state-level incentives, are creating an unprecedented demand for E-buses. The concerted effort by STUs to electrify public transport provides JBM Auto with a continuous and expanding tender pipeline.

Robust E-bus Order Book & Capacity Expansion: The company has successfully secured substantial orders for E-buses from multiple STUs and private fleet operators. The ongoing tendering for thousands of E-buses across the nation ensures a clear, long-term revenue visibility. JBM Auto is actively expanding its manufacturing capabilities to meet this escalating demand efficiently.

Integrated E-mobility Solution Provider: JBM Auto’s unique proposition of offering a comprehensive E-mobility ecosystem – encompassing E-bus manufacturing, charging infrastructure development, and full operational/maintenance support – creates a highly sticky customer base. This holistic approach simplifies procurement and operations for clients, fostering long-term partnerships and generating diversified revenue streams.

Product & Market Diversification: Beyond existing city buses, JBM Auto is expected to broaden its E-bus portfolio to target various market segments, including staff transport, intercity coaches, and school buses. Potential future expansion into other EV components or lighter EV segments could further diversify its revenue base.

Steady Automotive Components Business: While E-mobility is the primary growth engine, the established automotive components business continues to benefit from overall growth in vehicle production, increasing content per vehicle, and new platform wins with OEMs. This segment provides a stable revenue floor and technological synergies crucial for EV development.

Focus on Localization & R&D: JBM Auto’s commitment to in-house R&D and localization of critical EV components (e.g., battery management systems, power electronics) reduces reliance on imports, mitigates geopolitical supply chain risks, and enhances cost competitiveness, strengthening its long-term market position.

5. Risk Assessment

While JBM Auto holds significant promise, investors should be cognizant of several key risks:

Execution Risk in E-mobility: The rapid scale-up of E-bus manufacturing, the complex deployment of charging infrastructure, and the management of extensive long-term operational contracts (GCC models) pose substantial execution challenges. Any delays, quality issues, or operational inefficiencies could adversely impact profitability and brand reputation.

Intensifying Competition: Both the E-bus and automotive components segments are highly competitive. In E-buses, established players like Tata Motors and Ashok Leyland, along with specialized EV manufacturers such as Olectra Greentech, are aggressively vying for market share. This intense competition can lead to pricing pressures and margin contraction, particularly in government tenders.

Regulatory & Policy Dependency: The E-mobility sector is heavily influenced by government subsidies (e.g., FAME-II), policy mandates, and incentive structures. Any material changes, reductions, or delays in these supportive policies could significantly dampen demand, impact sales volumes, and erode profitability.

Commodity Price Volatility: JBM Auto’s manufacturing processes are sensitive to fluctuations in raw material prices, particularly steel, aluminum, and critical battery components. Inability to effectively hedge against these volatilities or pass on increased costs to customers could negatively affect margins.

Capital Expenditure & Funding Needs: The aggressive expansion in the E-mobility segment necessitates substantial capital expenditure for new capacities, R&D, and charging infrastructure. The company’s ability to raise capital efficiently (via debt or equity) and maintain a healthy debt-to-equity ratio will be critical for sustainable growth.

Technology Obsolescence: The EV industry is characterized by rapid technological advancements in battery chemistry, motor efficiency, and charging solutions. JBM Auto must continuously invest in R&D to remain at the forefront. Failure to adapt to evolving technologies could lead to product obsolescence and loss of market share.

Customer Concentration (E-buses): A substantial portion of the E-bus business relies on government tenders awarded by STUs. Delays in tender finalization, payment cycles, or contract modifications from these key customers could impact the company’s cash flow and revenue recognition.

6. Valuation & Price Target

Valuing JBM Auto requires a forward-looking approach that accounts for its significant growth potential in the E-mobility sector, which often commands premium valuations in India’s capital markets.

Current Earnings Power: The company’s TTM EPS stands at ₹8.93, derived from the sum of EPS from its latest four reported quarters (Mar 2025: ₹2.81 + Jun 2025: ₹1.56 + Sep 2025: ₹2.23 + Dec 2025: ₹2.33). This demonstrates a substantial improvement in earning capabilities.

Earnings Growth Projection: JBM Auto has shown strong EPS growth, from ₹5.26 in Mar 2023 to ₹7.56 in Mar 2024 (a 43.7% increase), and further to ₹8.93 TTM (an 18.1% increase over Mar 2024 annual EPS). Given the strong order book, government impetus for E-mobility, and the company’s strategic positioning, we project a conservative yet robust 25% EPS growth for the next fiscal year (FY26) over the current TTM EPS.

Projected FY26 EPS = TTM EPS * (1 + Growth Rate) = ₹8.93 * (1 + 0.25) = ₹11.16.

Forward P/E Multiple: Companies in the high-growth Indian EV and related sectors frequently command significantly higher valuation multiples than traditional industrial or automotive ancillary companies. This premium reflects aggressive future growth expectations, market leadership potential, and alignment with national strategic priorities. While conventional P/E multiples might be 20-30x for established industrials, EV-centric growth companies can trade at 100x or even significantly higher. Considering JBM Auto’s integrated E-mobility offering and strong growth trajectory, we apply a forward P/E multiple range of 100x to 120x, which is aggressive but reflects the market’s propensity to value such growth stories at a substantial premium.

Price Target:

Lower Bound Target Price: ₹11.16 (Projected FY26 EPS) * 100 (Forward P/E) = ₹1,116

Upper Bound Target Price: ₹11.16 (Projected FY26 EPS) * 120 (Forward P/E) = ₹1,339

Our 12-18 month price target range for JBM Auto Ltd. is ₹1,116 - ₹1,339. This target is predicated on the company’s continued robust execution in the E-mobility sector, sustained governmental support for EV adoption, and the market’s willingness to maintain a premium valuation for companies with significant EV growth exposure. Investors should acknowledge that this valuation embeds substantial future growth expectations and carries inherent risks associated with high-growth industries.

Note: The current market price of JBM Auto Ltd. was not provided in the prompt. This price target is derived based on projected earnings and an assumed sector-appropriate forward P/E multiple, reflecting implied market expectations for EV growth stocks.

7. Management Quality & Governance

The management of JBM Auto, spearheaded by its experienced promoters, has demonstrated exceptional strategic foresight and execution capabilities, particularly through its successful and timely pivot into the E-mobility domain.

Strategic Vision: The leadership’s early identification of the transformative E-mobility opportunity and their proactive investments in comprehensive capabilities—from R&D and manufacturing to an entire ecosystem of buses, charging, and operations—underscores a clear, forward-thinking strategic vision. This has been instrumental in positioning JBM Auto as a frontrunner in a high-potential, nascent sector.

Capital Allocation: While granular details on specific capital allocation decisions (e.g., precise debt vs. equity mix for growth funding) are not explicitly provided, the company’s ability to finance substantial expansion within the E-bus segment while simultaneously achieving significant revenue and profit growth post-2021 suggests prudent and effective capital deployment into high-return avenues.

Operational Excellence: The consistent performance of the established automotive components business, coupled with the successful ramp-up of E-bus production, delivery, and operational management, attests to the management’s strong operational prowess and capability to navigate complex manufacturing, supply chain, and logistical challenges inherent in both segments.

Governance Framework: Although specific promoter holding percentages were not provided in the data, a strong promoter-led management in the Indian context often indicates a long-term strategic focus and dedicated leadership. The company’s consistent and transparent reporting of quarterly and annual financial results aligns with good corporate governance practices. The clear strategic direction and tangible growth validate the quality of strategic decisions made by the leadership.

8. Competitive Positioning

JBM Auto maintains a strong and differentiated competitive position, leveraging its dual-pronged business model and integrated approach to the EV value chain.

Dual-Segment Synergies and Strengths:

Automotive Components: The company benefits from deep-seated, long-standing relationships with leading OEMs as a Tier-1 supplier. Its diverse product portfolio, technological capabilities, adherence to stringent quality standards, and reliable delivery schedules create a formidable competitive moat against smaller, less integrated players.

E-mobility: JBM Auto was an early entrant into the Indian E-bus manufacturing space. This first-mover advantage has allowed it to build a significant initial order book, accumulate invaluable operational experience, and establish a recognized brand presence in a rapidly evolving market.

Integrated E-mobility Value Chain Advantage: A key differentiator for JBM Auto is its holistic E-mobility offering. Unlike many competitors who may focus solely on vehicle manufacturing, JBM Auto provides an end-to-end ecosystem: the E-bus, comprehensive charging infrastructure, advanced battery solutions, and long-term maintenance/operational contracts. This ‘one-stop-shop’ approach significantly simplifies the procurement and operational complexities for STUs and private operators, fostering deeper customer relationships, creating multiple revenue streams, and enhancing customer stickiness.

Technological Prowess and Localization: JBM Auto’s substantial investments in in-house Research & Development, coupled with a strategic focus on localizing critical EV components and technologies, strengthen its cost competitiveness. This localization effort reduces reliance on volatile global supply chains, mitigates currency risks, and aligns with national ‘Make in India’ initiatives, providing a crucial long-term competitive edge.

Competitive Landscape:

E-Bus Segment: Primary competitors include established commercial vehicle manufacturers like Tata Motors and Ashok Leyland, both of whom are aggressively expanding their E-bus portfolios, as well as specialized EV bus manufacturers such as Olectra Greentech.

Auto Components Segment: The company competes with a broad spectrum of domestic and international automotive ancillary players, segmented by component type and customer base.

Despite the highly competitive environment, JBM Auto’s strategic integration, early market entry in E-mobility, and commitment to technological innovation position it strongly to capture significant market share in India’s transformative transportation landscape.

Raw Financial Data

Historical Results (Annual)

Latest Results (Quarterly)

Thanks for this article. With re: valuation, JBM Auto, Olectra Greentech are at an earnings multiple of 60-70x. In your analysis, you've used a 100x forward multiple for this outfit -- a premium of 50% over current PE. To me, that seems a tad aggressive. Also, I had come across a couple of reports last year where the assumed forward multiple was 40x for such a business (while as you rightly pointed out, traditional players have a lower multiple of 20-25x)

Have you come across something that points to investors ready to pay so much more (i.e. 100x) for companies in this sector?