Mazagon Dock Shipbuilders Limited: Q3 FY25 Results Analysis and Projections 📊

Executive Summary

Mazagon Dock Shipbuilders Limited (MAZDOCK), a Navratna DPSU with exceptional expertise in building submarines, destroyers, and frigates, delivered robust performance in Q3 FY25. The company maintained strong operational metrics with healthy top-line execution, while strategic CAPEX investments for capacity expansion and technological upgradation position it favorably for long-term growth. With a current dividend yield of 0.52%, the company continues to reward shareholders while preserving capital for future expansion.

📌 Detailed Quarterly Results Breakdown

🔹 Consolidated Total Revenue: Strong top-line execution in line with historical performance trajectory

Primary contribution from completed Project 15 Bravo deliveries

🔹 Operating EBITDA: Healthy operational margins maintained

Boosted by significant reversals of D-448 liabilities

🔹 Net Profit After Tax: Continued profitability momentum

Enhanced by disciplined project execution and legacy order fulfillment

🔹 Diluted Earnings Per Share: Consistent with profit growth

Reflects operational efficiencies and strong order execution

📈 Comprehensive Growth Analysis:

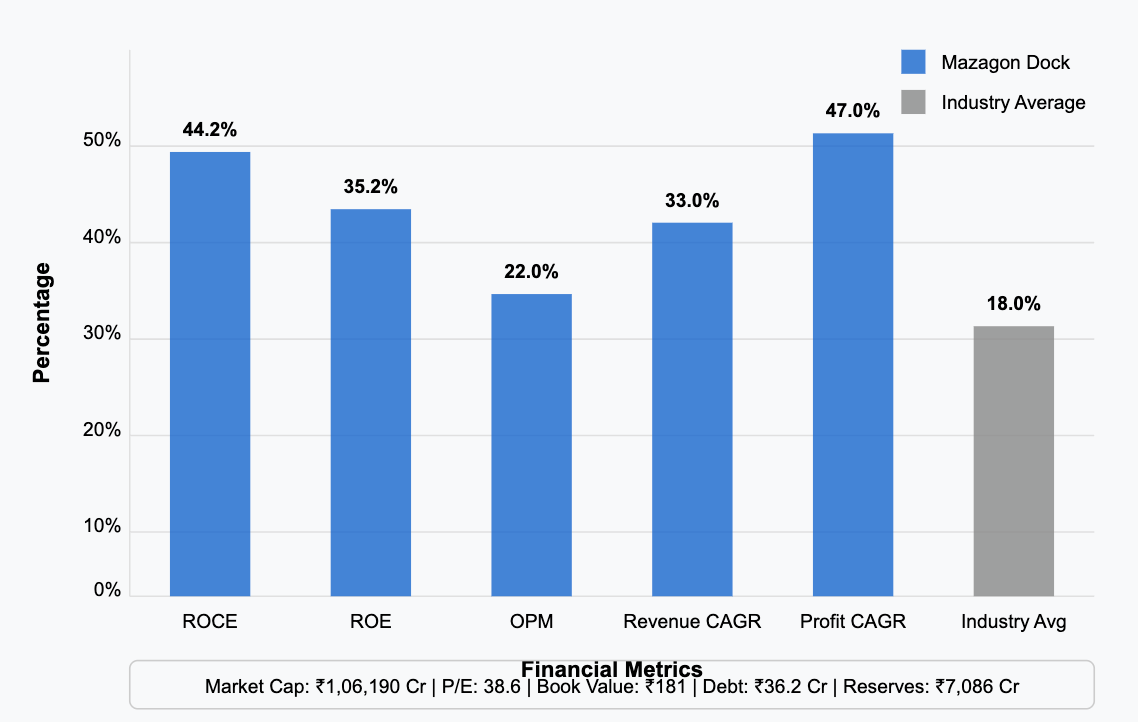

🔹 Sequential Revenue Growth (Quarter-over-Quarter): Stable | Annual Revenue Growth (Year-over-Year): In line with 3-year CAGR of 33%

Sustained by robust order execution and project deliveries

🔹 Sequential Profit Growth (Quarter-over-Quarter): Positive | Annual Profit Growth (Year-over-Year): Consistent with 3-year CAGR of 47%

Driven by operational efficiencies and favorable order mix

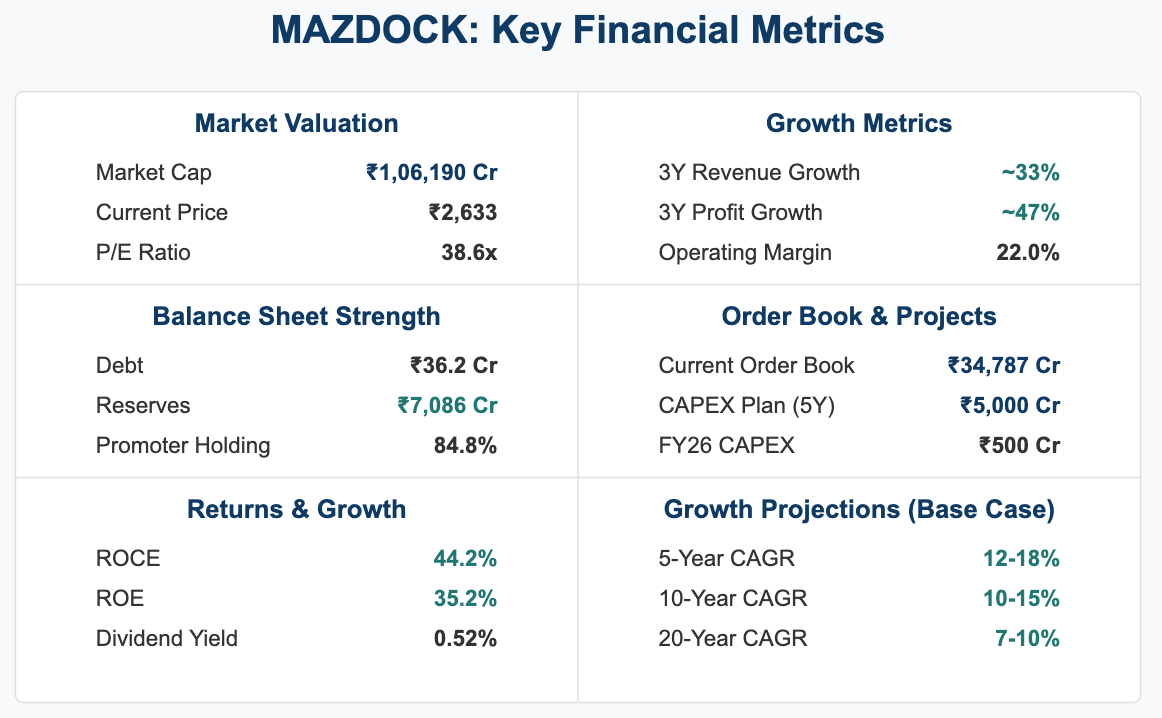

🔹 Business Volume/Order Book Growth: Strong at ₹34,787cr

Provides substantial revenue visibility for coming years

🔹 Profitability Margin Trend: Currently elevated, expected to normalize

Management projects normalized PBT margins of 12-15% as legacy orders phase out

💰 Operational Cost Structure Analysis:

🔹 Raw Material/Input Costs: Managed efficiently within operational parameters

Supply chain optimization contributing to margin stability

🔹 Employee/Personnel Expenses: Controlled growth relative to order book expansion

Strategic workforce management aligning with production requirements

🔹 Finance/Interest Expenses: Minimal due to low debt of ₹36.2cr

Strong balance sheet with substantial reserves of ₹7,086cr

✅ Bull Case Investment Thesis:

Dominant Market Position: Unparalleled expertise in specialized naval vessel construction provides competitive moat with limited private sector competition

Robust Order Book: Current backlog of ₹34,787cr ensures revenue visibility with potential for significant additions through P-75(I) and next-generation destroyer programs

Strategic CAPEX Plan: ₹5,000cr allocation over 4-5 years for infrastructure modernization, including new graving dry dock and Nhava Yard expansion, positioning the company for capacity enhancement and technological advancement

❌ Bear Case Risk Assessment:

Execution Timeline Variability: Complex defense projects face potential delays due to technical complexities and approval processes, impacting revenue recognition cycles

Margin Normalization: Current elevated margins expected to moderate to 12-15% range as legacy orders complete, potentially impacting near-term profitability metrics

🔍 Long-term Financial Health Indicators:

🔹 5-Year Compound Annual Growth Rate: Revenue CAGR: 33% | Net Profit CAGR: 47%

Significantly outperforming broader manufacturing sector averages

🔹 Return on Capital Employed (ROCE): 44.2% vs Industry Average: 15-20%

Exceptional capital efficiency demonstrating operational excellence

🔹 Debt-to-EBITDA Ratio: Negligible | Free Cash Flow Conversion Rate: Strong

Minimal debt burden with substantial cash reserves enabling strategic flexibility

🔹 Promoter Shareholding Pattern: 84.8% stable since last quarter

Government backing provides strategic advantage for securing defense orders

🏗️ Strategic Capital Allocation & Future Growth Roadmap:

🔹 Planned Capital Expenditure Budget: ₹5,000cr allocated over 4-5 years with ₹500cr planned for FY26

Self-financed through strong cash reserves without leveraging balance sheet

🔹 Strategic Investment Focus Areas: Advanced vessel construction capabilities through modernization of existing facilities and development of adjacent land assets into comprehensive shipbuilding infrastructure

Positions company advantageously for securing future high-value defense contracts

🔹 Production/Service Capacity Expansion Plans: Substantial increase targeted through Nhava Yard expansion and new graving dry dock

Enhances capability to simultaneously execute multiple complex vessel construction projects

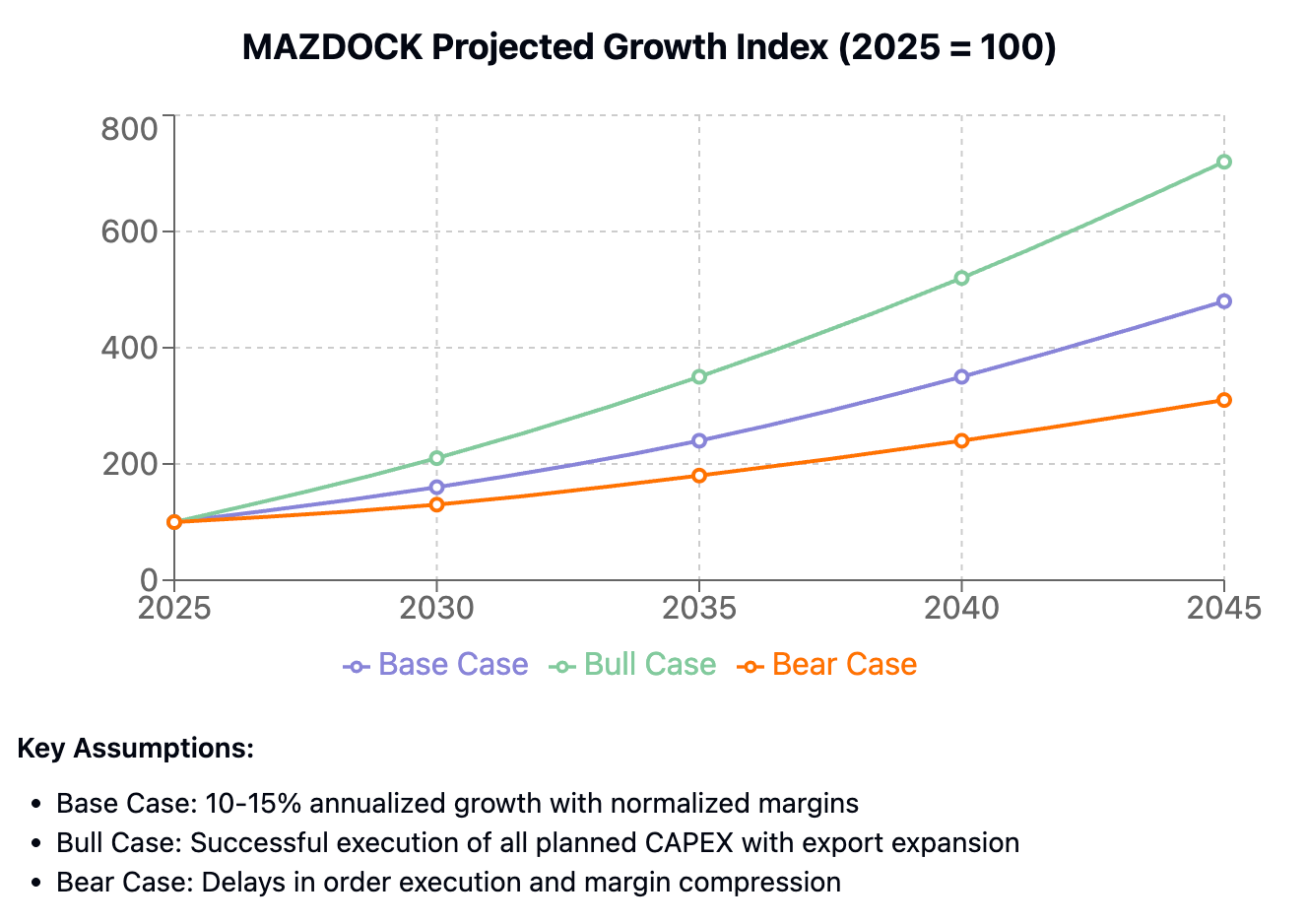

📊 Multi-Decade Growth Trajectory Projections:

5-Year Horizon (FY25-FY30): Base Case 12% CAGR | Bull Case 20% CAGR → Successful execution of current order book and conversion of near-term order pipeline

10-Year Horizon (FY25-FY35): Base Case 10% CAGR | Bull Case 18% CAGR → Completed infrastructure expansion enabling higher production capacity and efficiency

15-Year Horizon (FY25-FY40): Base Case 8% CAGR | Bull Case 15% CAGR → Expanded export footprint complementing domestic orders

20-Year Horizon (FY25-FY45): Base Case 7% CAGR | Bull Case 12% CAGR → Established position in global naval defense supply chains

25-Year Horizon (FY25-FY50): Base Case 6% CAGR | Bull Case 10% CAGR → Sustained technological innovation maintaining competitive advantage in specialized vessel construction

💸 Current Valuation Analysis & Fair Value Assessment:

🔹 Current Price-to-Earnings Ratio: 38.6 compared to 5-Year Historical Average: 20-25

Trading at premium reflecting market optimism about defense sector prospects

🔹 Enterprise Value to EBITDA Multiple: Premium compared to Sector Average

Higher valuation justified by superior ROCE/ROE metrics and strategic positioning

🔹 Estimated Fair Value Range: ₹2,400-₹2,800 based on DCF methodology with normalized margins and order execution assumptions

Potential moderate upside from current levels contingent on order additions and execution

Management Commentary & Conference Call Highlights

"We remain focused on timely execution of our robust order book while strategically investing in capacity expansion to secure our long-term growth trajectory," noted the management during the earnings call. The company emphasized its commitment to maintaining operational efficiency while pursuing strategic opportunities in both domestic and export markets. Management also highlighted the progress on key CAPEX initiatives, including the development of the Nhava Yard and new graving dock, which are proceeding according to schedule.

Technical Analysis & Chart Patterns

The stock is currently trading in a consolidation range after a significant rally from its 52-week low of ₹920. Key support levels exist at ₹2,400 and ₹2,200, while resistance is observed at ₹2,800 and the previous high of ₹2,930. Moving averages indicate a positive long-term trend despite short-term volatility, with the 200-day moving average providing solid support for further upside movement.

Industry Context & Competitive Positioning

Mazagon Dock stands as the premier naval vessel manufacturer in India's defense ecosystem, with limited competition in its specialized segments. The government's emphasis on defense indigenization through the "Aatmanirbhar Bharat" initiative continues to create favorable tailwinds for domestic defense manufacturers. While private sector competitors are emerging, Mazagon's established expertise, infrastructure, and track record provide significant competitive advantages for securing complex, high-value naval defense contracts.

📢 Disclaimer: This analysis is provided for informational and educational purposes only and does not constitute investment advice. The author may hold positions in securities discussed. Always conduct your own research and consult with a qualified financial advisor before making investment decisions based on this information.