May Value Pick : A Stealth Opportunity for the Patient Investor

In today's market landscape of inflated valuations and stretched multiples, we've uncovered what might be the most overlooked compounding machine hiding in plain sight. This report details our findings on a remarkable business trading significantly below its intrinsic value, with fundamentals that suggest substantial mispricing by market participants.

Our investigation reveals a company with rare characteristics in today's environment: established market presence, consistent profitability, and a valuation that defies conventional wisdom. This isn't a speculative growth story built on promises—but rather a proven business model generating substantial cash flows while maintaining a fortress balance sheet.

What makes this opportunity particularly intriguing is the disconnect between the company's operational excellence and its market perception. While peers trade at premium multiples, this enterprise has been overlooked, creating an asymmetric risk-reward scenario for investors willing to look beyond headline narratives.

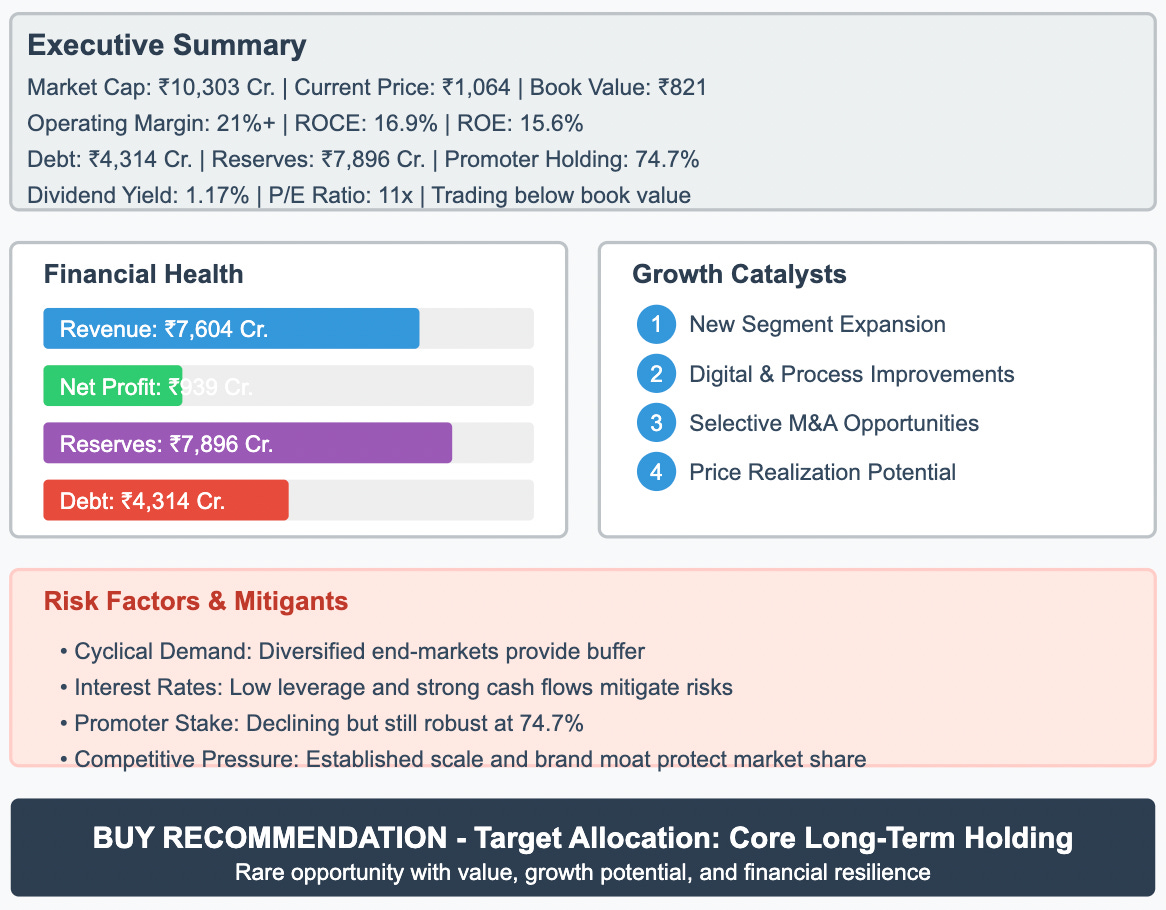

The numbers tell a compelling story: trading at ₹1,064 per share—below its book value of ₹821—this ₹10,303 crore market-cap business maintains impressive operating margins exceeding 21%. With ROCE of 16.9% and ROE of 15.6%, the company demonstrates exceptional capital efficiency across economic cycles.

What truly distinguishes this opportunity is its financial resilience. The conservative balance sheet shows ₹4,314 crore of debt against ₹7,896 crore in reserves—providing both defensive protection and offensive optionality. High insider ownership (74.7% promoter holding) aligns management interests with shareholders, despite modest selling over three years.

While recent growth has been steady rather than spectacular (4-5% over three years), the combination of pricing power, operational leverage, and strategic growth initiatives provides multiple pathways to accelerated earnings expansion. The company's consistent free cash flow generation and shareholder-friendly dividend policy (1.17% yield) further enhance total return potential.

Market participants have overlooked several critical inflection points that could catalyze a significant revaluation:

Expansion into adjacent high-margin segments

Operational improvements through digital transformation

Strategic deployment of excess capital reserves

Industry consolidation advantages for dominant players

At 11x earnings—a substantial discount to both peers and historical valuation—this opportunity offers both significant upside potential and downside protection. For investors with patience and conviction, this hidden gem represents that increasingly rare combination of value, quality, and growth potential.

Our recommendation: Establish a core position at current levels with plans to accumulate at current price and on any weakness below ₹900. This is not merely a trade, but potentially a cornerstone holding capable of delivering exceptional risk-adjusted returns over a 5-15 year investment horizon.

The identity of this company remains confidential in this report. Qualified investors seeking complete details should contact our research department directly.