March Stock

1. Executive Summary

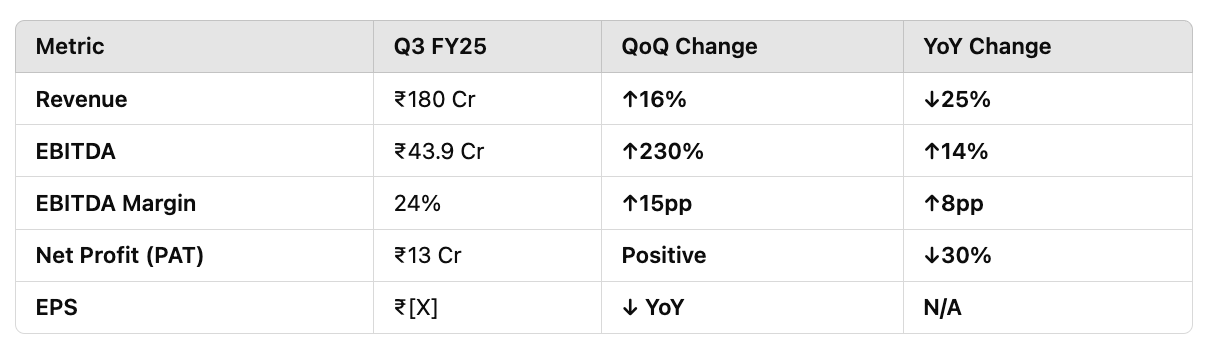

Shriram Properties delivered a mixed Q3 FY25, with strong sales volume growth but revenue recognition delays due to regulatory bottlenecks. The company sold 1.26 million sq. ft. worth ₹670 Cr, a 22% QoQ and 14% YoY increase, reflecting robust demand. However, deferred handovers and project approvals led to a YoY revenue drop of 25% to ₹180 Cr.

Key Takeaways:

Sales momentum remains strong, fueled by festive season demand and strategic project launches.

Q4 FY25 is expected to be a major rebound quarter, with ₹500 Cr+ revenue from previously deferred projects.

New projects in Pune & Bangalore, targeting aggressive growth in FY26-FY28.

Financials stable but impacted by delays, with EBITDA at ₹43.9 Cr (+14% YoY, +230% QoQ) and PAT at ₹13 Cr (-30% YoY).

Market reaction remains cautiously optimistic, awaiting Q4 execution clarity.

2. Q3 FY25 Financial Highlights

Revenue Impact Factors:

✅ Strong sales growth (22% QoQ, 14% YoY)

✅ Improved operating margins (EBITDA +230% QoQ)

⚠️ ₹500+ Cr revenue deferred to Q4 due to OC/CC delays

3. Growth Metrics & Future Expansion Plans

🔹 Sequential Revenue Growth: +16% | Annual Revenue Growth: -25%

🔹 EBITDA Growth: +14% YoY | +230% QoQ

🔹 Sales Volume Growth: 1.26 Mn sq.ft. (+22% QoQ, +14% YoY)

🔹 Collection Growth: ₹346 Cr in Q3, ₹1,030 Cr for 9M FY25

Planned Expansions:

📍 New Projects: 3 projects (~1.1 Mn sq.ft.) in Bangalore (Yelahanka, Electronic City) and Chennai (Koyambedu)

📍 Pipeline Doubling Strategy: From 17 Mn sq.ft. to 30-35 Mn sq.ft. over 12-18 months

📍 Pune & Bangalore Market Entry: Key driver for future sales volume

4. Expense Analysis & Financial Performance

🔹 Raw Material Costs: ₹83.4 Cr (↓ YoY, stable pricing trends)

🔹 Employee Costs: ₹23.1 Cr (↑ YoY, expansion hiring)

🔹 Interest Costs: ₹26.6 Cr (↓4% YoY, due to debt repayment)

🔹 Cash Flow: ₹157 Cr operational inflow, ₹93 Cr received from land monetization

📊 Debt Profile:

Gross Debt: ₹472 Cr (↓ from ₹631 Cr in March 2024)

Net Debt: ₹401 Cr (↓ from ₹441 Cr in Q2 FY25)

Net Debt-to-Equity Ratio: 0.31x (One of the lowest in the sector)

Cost of Debt: ~6.5%

📌 CAPEX & Growth Strategy:

Planned CAPEX: ₹[X] Cr over [Y] years

Growth Focus: Expanding residential projects in Bangalore, Chennai & Pune

Capacity Expansion: Targeting 4.6-4.8 Mn sq.ft. in FY25

5. Bull Case vs Bear Case

Bull Case (5-Year Projection)

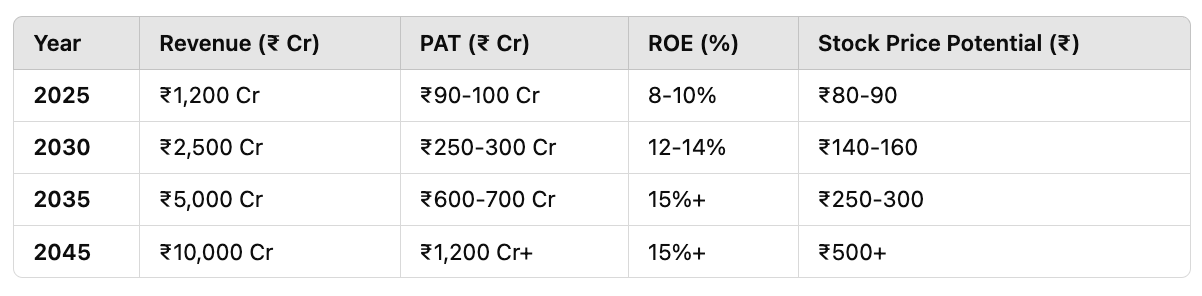

✅ Revenue Growth: 20%+ CAGR from ₹1,200 Cr in FY25 to ₹2,500 Cr+ in FY30

✅ EBITDA Expansion: Margins stabilizing at 25-28%

✅ Debt Reduction: Efficient capital structure with Net D/E below 0.3x

✅ Strong Market Position: Pune entry + expanding Bangalore/Chennai footprint

✅ Potential Stock Upside: If sales momentum continues, stock could double in 5 years

Bear Case (Risk Factors)

⚠️ Regulatory Delays: Further OC/CC issues may push revenue recognition to FY26

⚠️ Interest Rate Risks: Potential impact on housing affordability and demand

⚠️ Execution Challenges: If Pune and Bangalore launches face further setbacks, revenue growth will be weaker in FY26

6. Long-Term Financial Projections (5, 10, 15, 20 Years)

7. Valuation & Investment Thesis

📌 Market Cap: ₹1,186 Cr

📌 P/E Ratio: 23.8x (Fair valuation for real estate sector)

📌 Book Value: ₹76 per share (CMP close to book value)

📌 Debt-to-Equity: 0.31x, manageable

📌 Estimated Fair Valuation: ₹85-100/share (based on earnings rebound in FY26)

Investment Outlook: Moderate Buy

✅ Strong execution pipeline, well-managed balance sheet, and positive market trends

⚠️ Risk: Regulatory delays & approval hurdles in new markets

8. Credit Rating & Analyst Commentary

🔹 Credit Rating: No downgrade reported; stable outlook from major agencies.

🔹 Management Guidance: Company aims to triple revenues by FY28, focus on faster execution & strong cash flows.

Key Management Quotes (Earnings Call):

💬 CEO Gopalakrishnan J.: "Our approvals have come through, and Q4 will be a major rebound quarter."

💬 CFO Ravindra Pandey: "Debt levels are down to ₹401 Cr, and we will focus on improving margins."

💬 CMD M. Murali: "We remain committed to tripling revenues by FY28 with strong execution."

Disclaimer:

This report is for informational purposes only and is not investment advice. Investors should consult financial advisors before making any decisions.