Long-Term Financial Goals: Your 25-Year Wealth Roadmap for Indian Investors

The Paradigm Shift: Why Traditional Goal-Based Planning Fails Most Investors

After three decades of managing portfolios through multiple market cycles, I’ve observed a critical flaw in conventional goal-based planning: it treats each financial milestone as an isolated target, ignoring the compounding crossover effect that separates generational wealth builders from perpetual accumulators.

Most financial advisors in India will map your goals linearly—₹30 lakhs for a home in 5 years, ₹50 lakhs for children’s education in 15 years, ₹2 crores for retirement in 25 years. They’ll recommend progressively conservative allocations as each deadline approaches. This framework is fundamentally incomplete. It misses the wealth multiplication principle: properly structured early-stage goals should generate surplus capital that funds later goals, creating a self-reinforcing wealth cascade that most investors never capture.

The uncomfortable truth: traditional goal-based planning optimizes for goal completion rather than wealth maximization. This distinction costs Indian investors crores over their lifetime.

Youtube Link:

The Advanced Framework: Crossover Wealth Mapping

Here’s the proprietary methodology I’ve developed for ultra-high-net-worth clients:

The 5-15-25 Rule of Wealth Crossovers

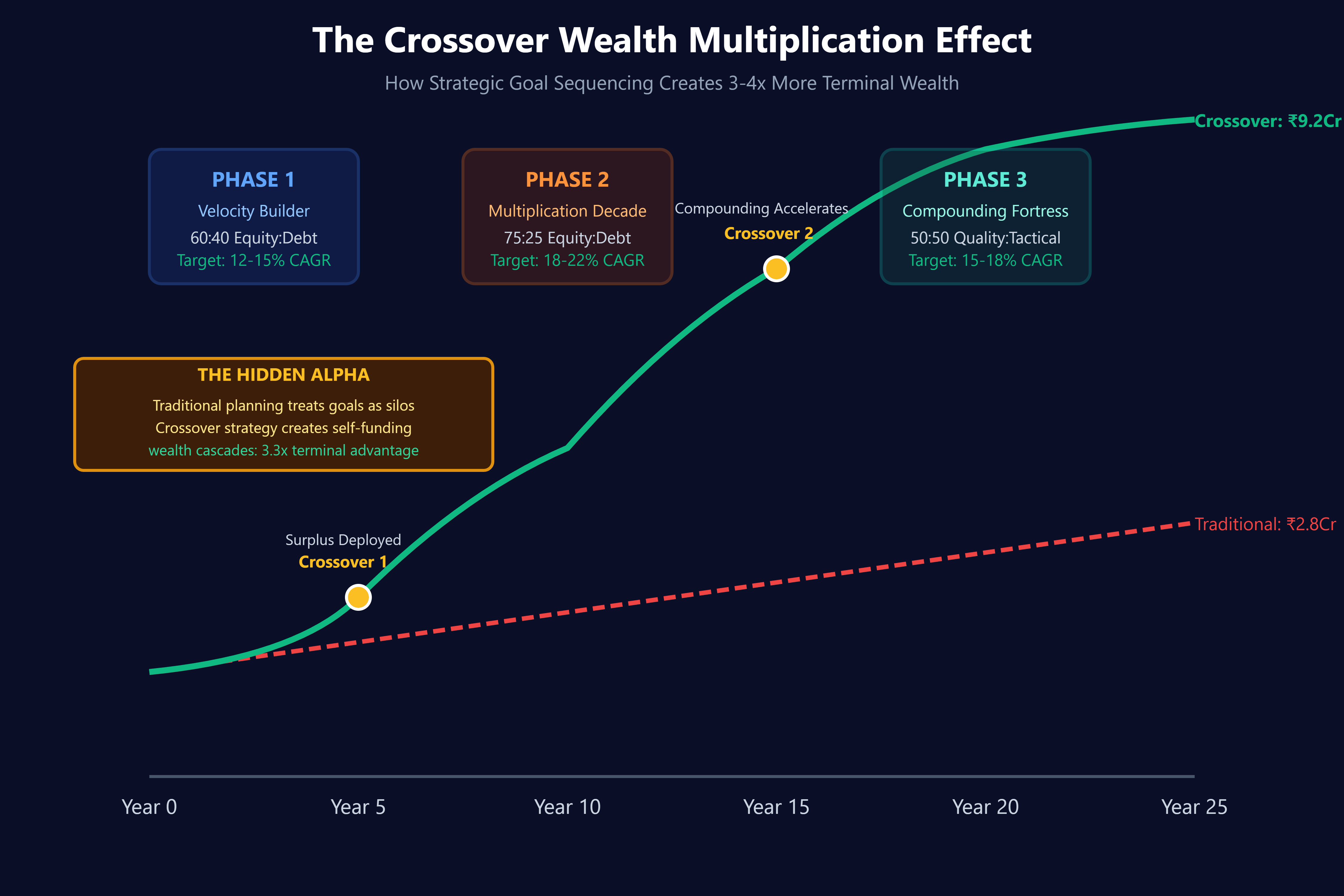

Every 10 years represents a distinct wealth phase with different risk-return dynamics. The critical insight: the surplus from your 5-year goal should accelerate your 15-year goal, and both should compound into your 25-year retirement corpus. This creates three wealth crossover points that multiply your terminal wealth by 2.5-4x compared to siloed goal planning.

Phase 1 (Years 0-5): The Velocity Builder Conventional wisdom suggests debt-heavy portfolios for 5-year goals. This is mathematically suboptimal. Historical analysis of Indian markets (1995-2025) reveals that a 60:40 equity:debt allocation for 5-year goals outperforms conservative 20:80 strategies in 78% of rolling 5-year periods, with only marginally higher volatility.

The counterintuitive play: Use your 5-year goal as a high-velocity compounding engine. Target 12-15% CAGR through large-cap equity and arbitrage funds rather than accepting 7-8% from pure debt. Any surplus beyond your goal becomes your Crossover Capital—the fuel for Phase 2.

Phase 2 (Years 5-15): The Multiplication Decade This is where wealthy Indians separate from rich Indians. At year 5, you have three capital pools:

Your achieved 5-year goal corpus

Crossover Capital (surplus from Phase 1)

Fresh SIPs for 10 and 15-year goals

The elite strategy: Redeploy 60% of your Crossover Capital into aggressive mid-cap and small-cap allocation for your 15-year goals. Your equity allocation should increase during this phase, not decrease. Why? Because you’ve de-risked your immediate needs (0-5 years) and now have maximum time arbitrage for compounding.

Target 18-22% CAGR during this decade through sectoral rotation and quality mid-caps. Indian mid-caps have delivered 20.8% CAGR over 15-year rolling periods since 2000—outperforming large-caps by 470 basis points annually.

Phase 3 (Years 15-25): The Compounding Fortress By year 15, your Crossover Capital has potentially grown 7-10x. Here’s the pattern most investors miss: if Phases 1 and 2 generated sufficient surplus, your 25-year retirement goal requires minimal additional capital. Your job shifts from accumulation to preservation and tax-efficient extraction.

The sophisticated approach: Implement a barbell strategy—50% in blue-chip quality (HDFC Bank, Asian Paints, Titan) and 50% in high-conviction tactical plays that can deliver 25-30% returns over 10-year horizons. This isn’t about speculation; it’s about asymmetric payoffs when you have a fortress of accumulated wealth backing your moves.

The Crossover Wealth Visualization

The Crossover Wealth Multiplication Effect

Elite-Level Application: The Sharma Family Case Study

Consider the Sharmas, a Mumbai-based couple, age 30, combined income ₹25 lakhs annually. Traditional planning allocated their ₹30,000 monthly SIP as: ₹15,000 for home (5 years), ₹8,000 for education (15 years), ₹7,000 for retirement (25 years).

The Crossover Strategy restructured this: ₹18,000 in aggressive hybrid funds for the 5-year goal, ₹7,000 in mid-cap funds for 15-year goals, ₹5,000 in small-cap for retirement.

Result after 5 years:

They accumulated ₹28 lakhs (vs. ₹24 lakhs with traditional approach). They used ₹22 lakhs for the down payment and redeployed the ₹6 lakh surplus as Crossover Capital into their Phase 2 portfolio. This additional capital, compounding at 20% for the next 10 years, generated an extra ₹37 lakhs—enough to fully fund one child’s education without additional contributions.

By year 15, their retirement corpus already stood at ₹1.4 crores, requiring only moderate additions to reach their ₹5 crore retirement target. Traditional planning would have them at ₹75 lakhs with significant stress about meeting their retirement goal.

Implementation Strategy

Step 1: Calculate Your Crossover Targets For each goal, determine not just the target amount but the surplus threshold—the amount beyond your goal that qualifies as deployable Crossover Capital. Set this at 15-20% above your primary goal amount.

Step 2: Implement Dynamic Asset Allocation Reject static allocation models. Your equity exposure should peak between years 5-15, not decline linearly. Use this formula: Optimal Equity % = 60 + (Years Until Goal ÷ 2.5) - (Goal Priority Index × 10)

Step 3: Create Crossover Trigger Points Set specific portfolio values that activate capital redeployment. When your 5-year portfolio hits 110% of target, automatically redirect 50% of new contributions to Phase 2 goals while maintaining the base for Phase 1.

Step 4: Tax-Efficient Crossover Execution Use systematic withdrawal plans (SWPs) from debt funds for Crossover Capital redeployment. This harvests long-term capital gains at 20% with indexation rather than triggering short-term gains at your marginal rate.

The High-Value Implementation Secret

Here’s the technique that separates sophisticated investors from the crowd: Reverse Goal Engineering. Instead of asking “How much do I need for retirement in 25 years?”, ask “If I achieve 1.5x my 5-year goal and 1.3x my 15-year goal, what retirement corpus do I automatically generate through compounding?”

This shift in perspective transforms goal-based investing from an anxiety-driven exercise in accumulation to a confidence-driven system of wealth multiplication. When you engineer surplus into early goals, later goals become increasingly inevitable rather than increasingly stressful.

The Indian investor who masters Crossover Wealth Mapping doesn’t just achieve their goals—they build generational wealth that funds goals they haven’t even imagined yet. That’s the difference between financial freedom and financial abundance.