KRN Heat Exchanger and Refrigeration Limited: Q3 FY25 Results Analysis

Q3 FY25 Results

Welcome to this in-depth analysis of KRN Heat Exchanger and Refrigeration Limited's (KRN) Q3 FY25 results. This newsletter dives into the company's performance metrics, future projections, strategic initiatives, and its position in the competitive landscape, all derived from the latest investor presentation.

Financial Performance Highlights

Revenue Growth

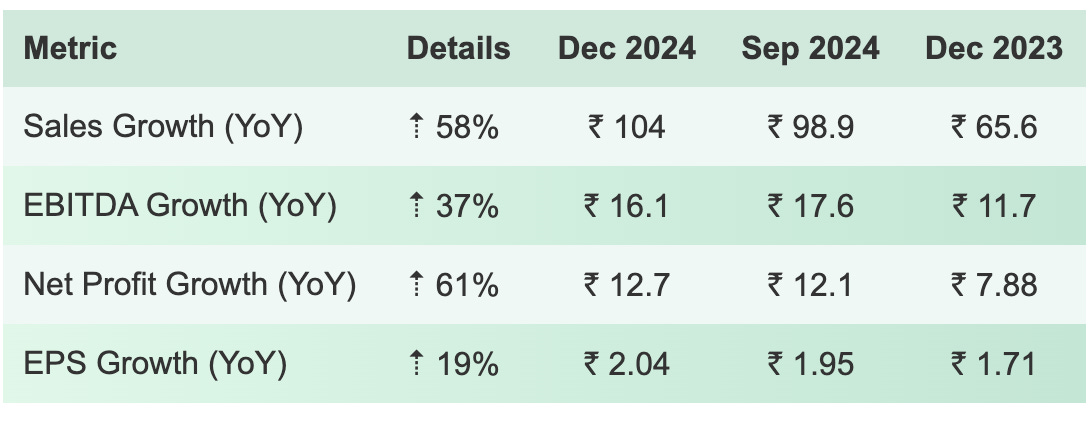

Q3 FY25 Revenue: ₹9,109.59 Lakhs (YoY growth of 28.41%).H1

FY25 Revenue: ₹18,688.04 Lakhs, up 16.24% YoY.Growth was driven by robust demand in the HVAC&R sector, with

domestic sales contributing 85% and exports seeing a significant rise of 30% YoY.

Profitability Metrics

EBITDA: ₹1,955.27 Lakhs (YoY growth of 36.38%) with an

EBITDA margin of 21.17%, compared to 19.93% in Q3 FY24. The margin expansion is attributed to cost control measures and operational efficiencies.

Net Profit: ₹1,231.08 Lakhs (YoY growth of 42.98%), with a net profit margin of 13.35% (up from 12% in Q3 FY24).

Operational Metrics

Capacity Utilization: Averaged ~85% across key products:

Evaporator Coils: 84.09%

Condenser Coils: 85.24%

Sheet Metal Parts: 85.77%

Total production capacity stands at 1.5+ million units annually, showcasing scalability.

Segment-Wise Revenue Contribution

Product-Wise Contribution (FY25):

Evaporator Coils: ₹11,558.70 Lakhs (37.49%)

Condenser Coils: ₹17,029.57 Lakhs (55.24%)

Other Segments (Headers, Sheet Metal, etc.): ₹2,240.04 Lakhs (7.27%)

Geographical Revenue Breakdown (FY24):

Domestic Sales: ₹26,285.23 Lakhs (85.26% of total revenue)

Exports: ₹4,526.64 Lakhs (14.68% of total revenue), with key markets in Asia (58.97%), North America (23.55%), and Europe (17.48%).

Strategic Growth Drivers

Capacity Expansion Plans

KRN has announced the establishment of a new manufacturing facility under its subsidiary, KRN HVAC Products Private Limited.New products include Bar & Plate Heat Exchangers, Oil Cooling Units, and Roll Bond Evaporators to cater to niche industrial applications.The company targets an increase in annual production capacity to 2 million units by FY27.

Focus on R&D and Innovation

Investment in product design and development has consistently increased, with the design team emphasizing:Nano and powder coatings for corrosion resistance.Enhanced durability and thermal efficiency.FY25 R&D expenditure: ₹11.88 Lakhs.

Export Market Penetration

Aiming to increase export revenue from 14.68% to 25% by FY26, focusing on North America and Europe.Strengthening relationships with global clients like Daikin, Schneider Electric, and Blue Star.

Operational Efficiency

Integration of advanced testing facilities:Helium Leak Tests, Salt Spray Tests, and Burst Pressure Tests ensure product quality.In-house precision engineering reduces production costs and improves delivery timelines.

Future Projections and Outlook

Revenue and Profit Projections

FY25 Revenue Estimate: ₹35,000 Lakhs (+18% YoY).EBITDA Margin: Expected to stabilize at ~20% due to economies of scale.Net Profit: Projected growth of 25% YoY, driven by improved operational efficiencies and product mix.

Industry Growth Tailwinds

The global heat exchanger market is projected to grow at a CAGR of 6.2%, reaching $20 billion by 2030.The Indian HVAC market, valued at $7.8 billion in 2021, is expected to grow to $27.4 billion by 2030, boosting demand for KRN’s products.

Risks and Challenges

High Valuation: With a P/E of 115, KRN’s stock is priced for perfection. Any deviation from projected growth could lead to sharp corrections.Customer Concentration: Top 10 customers contribute 75.94% of revenue, exposing KRN to revenue concentration risks.Export Risks: Exposure to forex fluctuations and geopolitical uncertainties in key markets.Rising Competition: Competitors like Blue Star and Voltas could erode market share with aggressive pricing strategies.

Competitive Positioning

Key Strengths:

In-house R&D and precision manufacturing capabilities.Long-standing partnerships with global giants in HVAC&R.Strong brand reputation for quality and innovation.

Peers:

Blue Star Limited: Strong in commercial HVAC systems.Voltas: Market leader in residential air-conditioning with robust distribution.Kirloskar: Focused on industrial cooling solutions.

Valuation and Investment Thesis

Using a DCF valuation with a terminal growth rate of 6% and a discount rate of 10%, the intrinsic value of KRN’s stock is estimated at ₹850/share, indicating a 15% upside potential from the current price of ₹738.

Why Invest?

Growth Potential: High demand for HVAC&R systems in domestic and export markets.Margin Expansion: Strong operational efficiencies and cost control measures.Strategic Expansion: New facilities and products to drive revenue diversification.

Why Stay Cautious?

Valuation Risk: Current multiples leave limited room for error.Customer Dependency: Heavily reliant on a concentrated client base.

Conclusion

KRN Heat Exchanger is well-positioned to capitalize on the robust growth in the HVAC&R sector. With strong financials, innovative products, and strategic expansions, the company is set for sustained growth. However, its high valuation and customer concentration risks require close monitoring.

Disclaimer

This article is for informational purposes only and does not constitute investment advice. Readers should conduct their own research and consult financial advisors before making investment decisions.