Revenue guidance: ₹4100 Crores, order book: ₹9072 Crores — a 67% jump from a year ago

SECTION I — Investment Thesis & Summary

Here’s the honest truth about this stock right now — it’s fallen nearly 50% from its peak of ₹7,822 and most people have written it off. But that’s exactly when the interesting conversations start.

This company sits at the center of India’s electronics manufacturing push. Semiconductors, aerospace components, IoT modules, automotive electronics — they make it all. The stock’s down because of a one-time miss on railway order execution and a slightly softer Q3. The fundamentals, however, haven’t cracked.

Simply put: the business is growing fast, the order book is at record levels at ₹9,072 Crores, and the market is panicking over a quarterly blip. That kind of mismatch is where patient investors tend to make money.

SECTION II — Business Model & Operations

The company is India’s most integrated electronics manufacturer — and that word “integrated” matters more than people realize.

Most companies in this space are assemblers. This one designs, engineers, manufactures, and supports the entire lifecycle of electronic systems. Their customers span nearly every high-growth sector you can think of: automotive companies embedding more electronics into vehicles, defense contractors needing indigenous components, space programs, medical device makers, railways, and industrial automation firms.

Revenue flows in from two primary streams — Electronic Manufacturing Services (EMS), which is the bulk of the business, and a rapidly growing new vertical in OSAT (semiconductor assembly and testing) plus High-Density Interconnect PCBs (HDI PCBs). These newer segments are where the next decade of value is being built.

Lately, the company has been executing on a massive capacity expansion. A new facility focused on OSAT, which is essentially the finishing stage for semiconductor chips, is being set up with support under India’s PLI scheme. They also raised ₹1,374 Crores through a QIP (basically, selling new shares to institutions) to fund this expansion, of which around ₹367 Crores was still unutilized as of December 2025 — a solid liquidity buffer.

The revised FY26 revenue guidance is ₹4,100 Crores. That’s ambitious but not unreasonable given the order book standing at ₹9,072 Crores — a 67% jump from ₹5,422 Crores a year ago.

Youtube Link:

SECTION III — Historical Financial Review

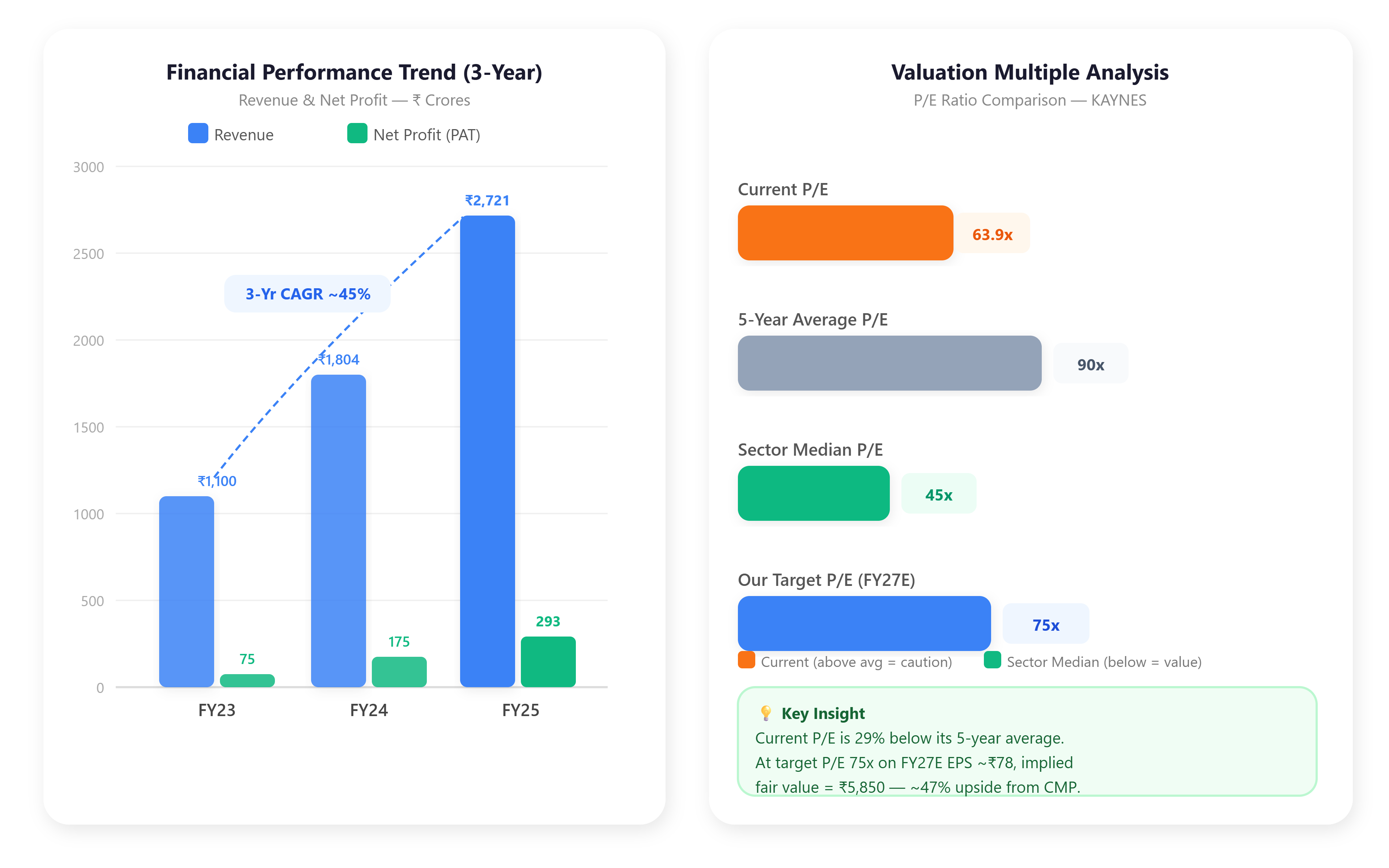

The revenue growth story here is genuinely impressive. Over the last three fiscal years, the company went from roughly ₹1,100 Crores in revenue (FY23) to ₹1,804 Crores (FY24) to ₹2,721 Crores (FY25). That’s a 3-year revenue CAGR north of 45%. Not many mid-caps grow like that.

Net profit followed a similar trajectory — roughly ₹75 Crores in FY23, climbing to ~₹175 Crores in FY24, and ₹293 Crores in FY25. The last 12-month diluted EPS works out to approximately ₹58-65 — and earnings are still growing.

Here’s the thing though — Q3 FY26 (October–December 2025) was softer than expected. Revenue came in at ₹849 Crores, net profit dropped to ₹76.6 Crores from ₹121 Crores the previous quarter. Management pointed to delayed railway order dispatches as the primary culprit. This is a timing issue, not a structural one. Railway orders don’t disappear — they just shift quarters.

Operating margins have held in the 14-17% range consistently, which signals a business that has pricing discipline. Interest costs have risen alongside debt taken for expansion, which is expected and manageable given the revenue trajectory. The balance sheet expanded to ₹4,641 Crores in total assets by FY25, up 42% from the prior year — all being deployed into productive capacity.

Cash generation is solid, with operating cash flows tracking the profit growth. The company pays no dividend — not a red flag here, because every rupee is going back into building capacity for a wave of orders that the order book clearly signals is coming.

Do you want to know this great investment :