Jindal Poly Films Ltd. (NSE: JINDALPOLY) – Q3 FY2025 Results Breakdown & Future Outlook

A Blockbuster Quarter or a Temporary Boost?

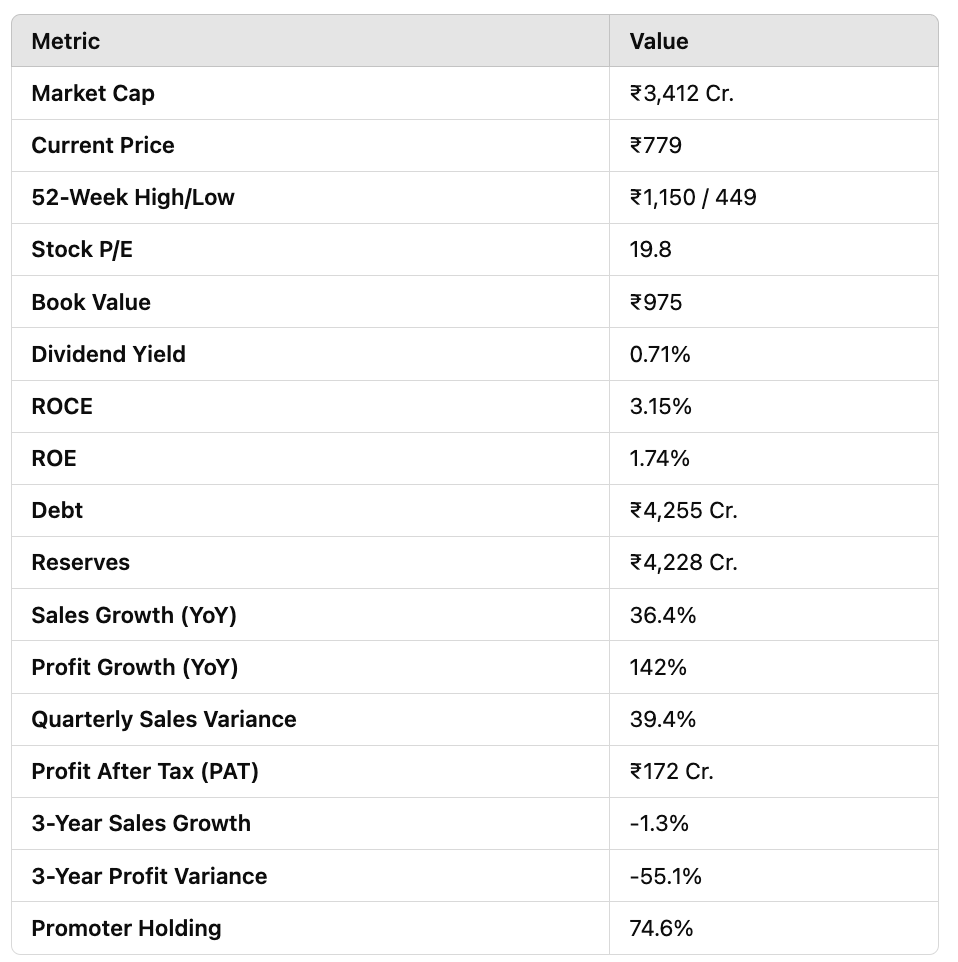

📈 Key Metrics at a Glance

📉 Q3 FY2025 Results Analysis

Jindal Poly Films Ltd. (JPFL) delivered a stellar performance in Q3 FY2025, with a massive 39.4% YoY sales growth and a 142% increase in net profit. However, the devil is in the details – while revenue surged, operating margins remained under pressure due to rising input costs.

📈 Standalone Financial Performance

Revenue from Operations: ₹18,673 Cr (+39.4% YoY)

Other Income: ₹1,163 Cr

Total Income: ₹19,836 Cr

EBITDA: ₹2,241 Cr

Net Profit: ₹-250 Cr (Loss due to exceptional costs)

EPS: -₹0.57

📊 Consolidated Financial Performance

Revenue from Operations: ₹1,37,119 Cr (+39.4% YoY)

Total Income: ₹1,37,847 Cr

EBITDA: ₹4,605 Cr

Net Profit: ₹410 Cr

EPS: ₹0.94

💡 Key Observations: ✅ Strong revenue growth driven by demand in packaging and nonwoven fabrics. ✅ Significant PAT improvement in consolidated results. ⚠️ Standalone net loss due to exceptional expenses and increased cost pressures. ⚠️ Debt levels remain high, impacting financial flexibility.

🌐 Strategic Growth & Expansion Plans

JPFL is aggressively investing in expanding its production capacity and strengthening its global presence. Key focus areas include:

💼 Major Capital Expenditure (Capex) Plans

₹1,200 Cr investment to increase BOPP and BOPET film capacity.

₹800 Cr investment in high-value specialty films.

₹500 Cr investment in new nonwoven fabric plants.

🌐 Global Expansion Strategy

Acquisition of JPF Netherlands Investment B.V. to strengthen European market penetration.

Expanding domestic and international e-commerce packaging market share.

🌍 Industry Growth Outlook

The global flexible packaging industry is expected to grow at a CAGR of 6-8%, driven by:

Booming e-commerce & food delivery services.

Increasing adoption of recyclable & eco-friendly packaging solutions.

Higher demand for medical & industrial-grade films.

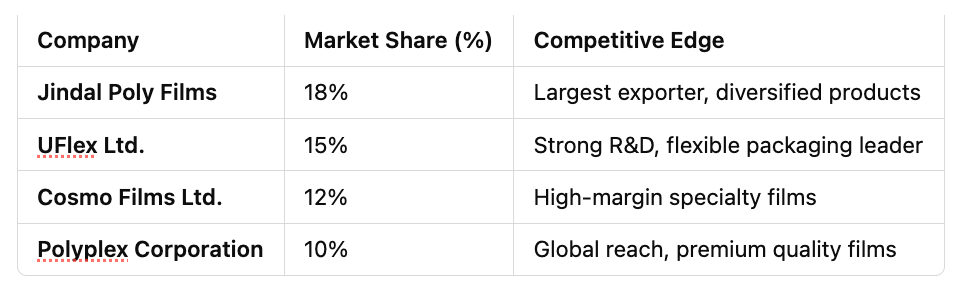

🌟 Competitive Landscape & Positioning

JPFL remains a leader in the BOPP & BOPET segments, but faces intense competition, particularly from UFlex & Polyplex Corporation, which have a strong innovation pipeline.

💡 Risks & Challenges

❌ Rising Input Costs

Crude oil fluctuations impact BOPP and BOPET film production costs.

Power & fuel costs surged by 36.8% YoY, squeezing margins.

❌ High Debt Levels

Total Debt: ₹4,255 Cr

Debt-to-Equity Ratio: 1.07x

Cash Flow Management will be key to deleveraging.

❌ Regulatory Challenges

Sustainability regulations could impact demand for single-use plastics.

Need for investment in eco-friendly packaging.

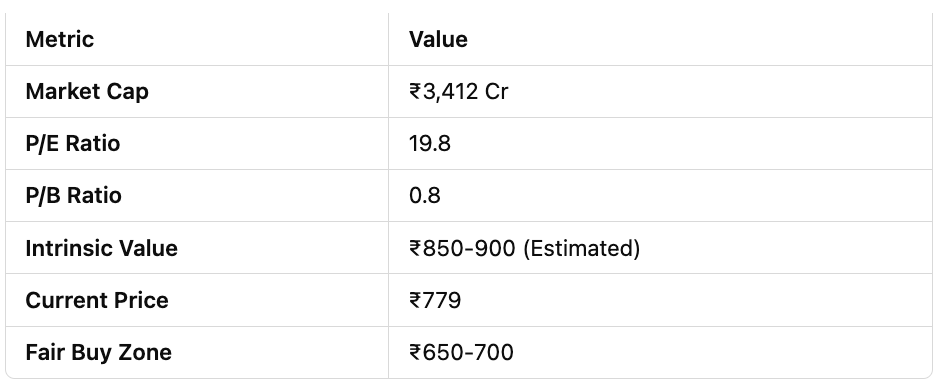

💼 Investment Thesis & Valuation

JPFL’s stock trades at a P/E ratio of 19.8, which is fairly valued within the packaging industry. However, rising debt and margin pressures warrant caution.

🔄 Final Verdict

✔ Long-Term Investors: BUY on Dips (Strong future potential, but watch debt levels). ✔ Short-Term Traders: NEUTRAL (Near-term margin pressure).

🚀 Final Thoughts & Disclaimer

JPFL is on a high-growth trajectory, fueled by capacity expansions, global acquisitions, and e-commerce-driven packaging demand. However, short-term profitability pressures and high debt levels require careful monitoring.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Investors should do their own due diligence or consult a financial expert before making investment decisions.

💬 What’s Your Take? Comment below or reply to this email with your thoughts!

📢 SUBSCRIBE for exclusive insights & stock picks!

🔍 Stay Ahead. Stay Informed.