Infosys Ltd Q3 FY2025 Results performance

Dear Subscribers,

Welcome to this premium edition of our newsletter where we dive deep into Infosys Ltd’s Q3 FY2025 performance and chart an exciting roadmap for its future. In an industry evolving at breakneck speed, Infosys has once again demonstrated its prowess—delivering robust results, pioneering digital innovation, and setting the stage for sustainable long‐term growth.

Q3 FY2025: A Snapshot of Stellar Execution

Infosys posted a resilient quarter marked by:

• Solid Revenue & Profit Performance:

– Revenue grew by 6.1% YoY in constant currency, even as seasonality and lower working days posed headwinds.

– Net profit surged by 11.4%, reflecting disciplined execution and strategic pricing initiatives that enhanced margins to 21.3% (up by 20 bps sequentially).

– Large deal wins reached a total contract value of $2.5 billion, with net new contributions up by 57% from the previous quarter.

• Robust Cash Flow & Operational Efficiency:

– Free cash flow hit an all-time high of $1.26 billion, underscoring a razor-sharp focus on cash conversion.

– Employee headcount grew by over 5,000, now exceeding 323,000 globally, further strengthening Infosys’ operational scale.

These results not only exceeded market expectations but also laid a solid foundation for future growth, as reported by major outlets such as Reuters

and NDTV Profit

.

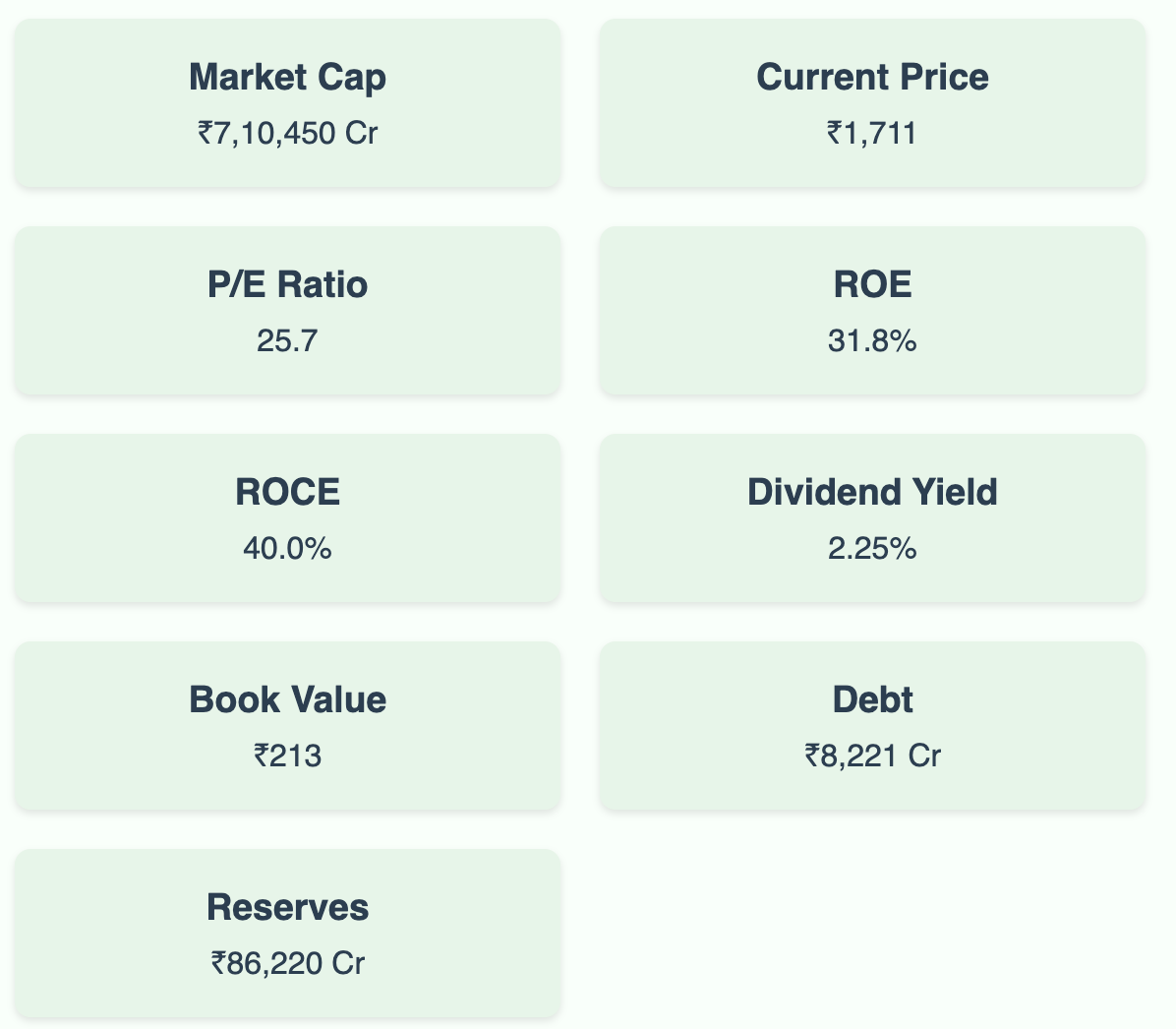

Key Financial Metrics at a Glance

For those who love the numbers, here’s a snapshot of Infosys’ current valuation and performance metrics:

These metrics underscore a financially sound entity with excellent profitability ratios and robust balance sheet strength.

The Future Roadmap: Innovation & Expansion

Infosys isn’t resting on its laurels. The company’s strategic roadmap is built on three key pillars:

Digital & AI Transformation:

– Infosys Topaz is at the forefront of its AI revolution. With four proprietary small language models (each with 2.5 billion parameters) and over 100 new generative AI agents in development, Infosys is empowering its clients across banking, cybersecurity, IT operations, and beyond.

– Enhanced digital platforms are expected to further boost operational efficiency and unlock new revenue streams.Geographical & Sectoral Expansion:

– Growth in the U.S. Financial Services segment continues to impress, and double-digit growth in European markets signals untapped potential.

– A focused push in Retail and Consumer Products is expected to capitalize on improving discretionary spending and evolving consumer sentiment.Talent & Operational Excellence:

– A commitment to hiring 15,000 freshers this fiscal and ramping up to 20,000 next year ensures a dynamic, agile workforce ready to support global expansion.

– Strategic capital expenditure, aimed at upgrading digital infrastructure and reskilling employees, reinforces Infosys’ competitive edge.

Long-Term Projections: Charting Returns Over Decades

Looking ahead, Infosys is poised to deliver attractive long-term returns. Based on our analysis and market sentiment, we project the following approximate growth trajectory, assuming an initial high-growth phase that moderates gradually over time:

Next 5 Years:

– Target CAGR: ~10–12%

– Projected Valuation: A potential price uplift to around ₹2,750

– Rationale: Continued expansion in high-growth verticals and successful digital transformation initiatives.Next 10 Years:

– Target CAGR: ~10%

– Projected Valuation: A price level near ₹4,430

– Rationale: Consolidation of market leadership, increased client reliance on AI-driven solutions, and robust free cash flow generation.Next 15 Years:

– Target CAGR: ~10%

– Projected Valuation: Approximately ₹7,150

– Rationale: Sustained operational efficiency, scale benefits, and a diversified revenue portfolio across geographies and sectors.Next 20 Years:

– Target CAGR: ~7–9% (as growth moderates)

– Projected Valuation: Roughly ₹11,520

– Rationale: A mature business model underpinned by strong fundamentals, steady dividend yield, and persistent innovation.

When combined with a dividend yield of 2.25%, the total return potential makes Infosys an attractive long-term play for both growth and income investors.

Investment Thesis & Valuation Perspective

Why Invest in Infosys?

Strong Financial Fundamentals: High ROE (31.8%), robust free cash flow conversion, and disciplined capital allocation underpin its premium valuation (P/E 25.7).

Strategic Vision: A clear focus on digital transformation and AI positions Infosys as a leader in a rapidly evolving industry.

Global Expansion: Positive trends in high-growth markets like the U.S. and Europe, coupled with strategic client wins, support sustained revenue growth.

Resilient Business Model: The company’s diversified portfolio and operational efficiency offer a buffer against macroeconomic uncertainties and competitive pressures.

With these factors, Infosys emerges as a compelling buy for investors with a long-term horizon, offering both capital appreciation and consistent income.

Risks & Considerations

No investment is without risk. Key factors to monitor include:

Currency Volatility: As a global player, adverse currency movements could impact margins.

Rising Costs: Wage hikes and increased third-party costs may exert short-term pressure on profitability.

Market Sentiment: Concerns over earnings quality, especially with heavy reliance on smaller deals, may cause near-term volatility.

Regulatory & Geopolitical Uncertainties: Shifts in visa regulations and global economic trends could influence business dynamics.

Final Thoughts

Infosys’ Q3 FY2025 performance is a testament to its robust execution, forward-thinking innovation, and strategic agility. As the company leverages digital transformation and expands its global footprint, its long-term growth prospects remain highly attractive. For investors seeking a balanced mix of growth and stability, Infosys offers a compelling investment case with significant upside potential over the next 5, 10, 15, and 20 years.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All projections and opinions are based on current market conditions and are subject to change. Please conduct your own research or consult a financial advisor before making any investment decisions.

Stay tuned for more in-depth analysis and insights in our next edition!