India's Largest Spirits Giant Is Being Ignored — Here's Why Smart Money Is Quietly Buying It

Equity Research Report: XXXXXXXXXXXXXXXXXX ()

Date: May 6, 2026

1. Investment Thesis & Summary

XXXXXXXXXXXXXXXXXX (), India’s largest alcoholic beverage company and a subsidiary of Diageo plc, presents a compelling investment opportunity driven by its dominant market position, aggressive premiumization strategy, and favorable long-term demographic trends in India. The company has successfully navigated a complex regulatory environment and significantly improved its profitability profile through strategic portfolio rationalization and operational efficiencies under Diageo’s stewardship.

Our “BUY” recommendation is underpinned by the following key factors:

Premiumization Tailwinds: India’s rapidly growing affluent consumer base and increasing disposable incomes are driving a structural shift towards premium and super-premium alcoholic beverages. USL, with its robust portfolio including global brands like Johnnie Walker and Smirnoff, alongside premiumized domestic brands such as Royal Challenge and McDowell’s No.1, is ideally positioned to capture this trend. The “Prestige & Above” (P&A) segment continues to outperform, contributing disproportionately to value growth and margin expansion.

Strong Parentage & Governance: Being a part of Diageo plc, a global leader, provides USL with unparalleled access to global best practices in brand building, innovation, supply chain management, and responsible marketing. This strategic backing ensures robust governance standards and a pipeline of successful international brands adapted for the Indian market.

Market Leadership & Distribution Prowess: USL maintains a leadership position in the Indian spirits market, backed by an extensive manufacturing and distribution network spanning across most Indian states. This scale provides a significant competitive advantage in terms of reach, cost efficiencies, and negotiation power.

Improving Financial Performance & Margin Expansion: Post a period of restructuring and integration with Diageo, USL has demonstrated consistent improvements in profitability. The strategic divestment of select ‘popular’ brands (Project Popular) has enhanced the overall portfolio margin profile. Operating leverage and a focus on cost rationalization are expected to drive further margin expansion. The latest TTM (Q4FY25-Q3FY26) data shows robust net profit growth and margin improvement.

Demographic Dividend: India’s young and growing population, increasing urbanization, and evolving social attitudes towards alcohol consumption provide a long-term structural demand driver for the spirits industry.

Our 12-month target price of INR 1,524.24, based on a 58.0x P/E multiple on projected TTM EPS of INR 26.28 (Q4FY26-Q3FY27), implies an upside of 15.82% from the current market price, warranting a “BUY” rating.

Key risks include adverse changes in state-level excise policies, rising input costs, and intensified competition. However, we believe USL’s strategic advantages and operational resilience adequately mitigate these concerns.

2. Business Model & Operations

XXXXXXXXXXXXXXXXXX (USL) is engaged in the manufacture, sale, and distribution of alcoholic beverages in India. Its business model is centered on building and managing a diversified portfolio of brands across various price points, with an increasing strategic emphasis on premium and luxury segments.

Product Portfolio: USL offers a wide array of Indian Made Foreign Liquor (IMFL) and imported foreign liquor (IFL) across categories such as Whisky, Brandy, Rum, Gin, and Vodka.

Prestige & Above (P&A) Segment: This segment is the strategic growth driver, comprising brands like Johnnie Walker, Black & White, Vat 69, Smirnoff, Tanqueray, Captain Morgan (imported brands), and Antiquity, Signature, Royal Challenge, McDowell’s No.1 Whisky, McDowell’s No.1 Brandy, and McDowell’s No.1 Rum (premiumized domestic brands). This segment contributes the majority of revenue and drives margin expansion.

Popular Segment: While historically a dominant segment, USL has strategically divested 32 brands in its ‘popular’ segment (under Project Popular, completed FY23), retaining only a few key popular brands (e.g., McDowell’s No.1 Celebration Rum, Blue Riband Gin) that demonstrate strong growth potential or strategic importance. The divestment allowed USL to focus on higher-margin P&A brands.

Manufacturing and Supply Chain: USL operates through a robust manufacturing and bottling network, including its own facilities and strategic third-party contractors across India. This extensive setup ensures efficient production and responsiveness to regional demand fluctuations. Raw materials primarily include Extra Neutral Alcohol (ENA), grains, and packaging materials.

Distribution Network: The company boasts an unparalleled distribution reach across India, leveraging relationships with state governments (who control alcohol distribution in many states), wholesalers, and retailers. The complex state-specific regulatory framework necessitates a deep understanding and strong local presence, which USL possesses.

Route to Market: Sales are executed through varied channels depending on state regulations, ranging from direct sales to state corporations, wholesale distributors, and retail outlets (on-premise and off-premise).

Diageo Synergy: As a subsidiary of Diageo, USL benefits from global brand development expertise, advanced marketing strategies, innovation capabilities, and responsible drinking initiatives. This integration has been crucial in transforming USL’s operations and brand portfolio.

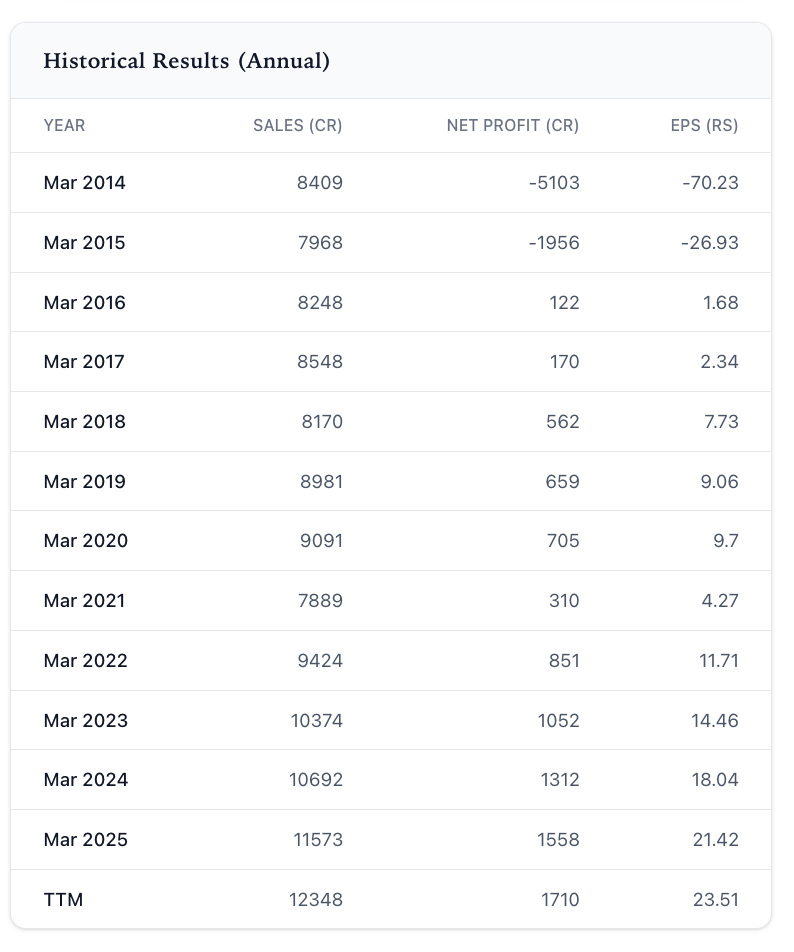

3. Historical Financial Review

USL’s financial trajectory over the past decade reflects a significant turnaround and strategic transformation under Diageo’s control.

Key Observations:

Turnaround from Losses: The early years (FY14-FY15) were marked by significant losses due to legacy issues, high debt, and operational inefficiencies prior to full Diageo control. A dramatic turnaround began in FY16, moving the company back to profitability.

Sales Growth & Resilience: Post a dip in FY21 due to the COVID-19 pandemic and associated lockdowns, USL has shown robust sales recovery and sustained growth. Sales increased from INR 7,889 Cr in FY21 to INR 11,573 Cr in FY25, and further to INR 12,348 Cr on a TTM basis (Q4FY25-Q3FY26). This demonstrates strong underlying demand and effective market strategies.

Accelerated Profitability: Net Profit has shown exceptional growth, particularly from FY22 onwards. From INR 310 Cr in FY21, Net Profit surged to INR 1,558 Cr in FY25, and reached INR 1,710 Cr on a TTM basis. This substantial increase is a testament to the success of the premiumization strategy, improved product mix, operational efficiencies, and the divestment of lower-margin popular brands.

Margin Expansion: The Net Profit Margin has expanded considerably. While not explicitly detailed in the table, the jump in Net Profit relative to sales growth indicates significant margin improvement. This is largely attributable to the shift towards higher-margin P&A brands and better cost management.

EPS Trajectory: Earnings Per Share (EPS) has mirrored the Net Profit growth, showcasing the enhanced value creation for shareholders. From a deeply negative EPS in earlier years, it has risen steadily to INR 21.42 in FY25 and INR 23.51 on a TTM basis.

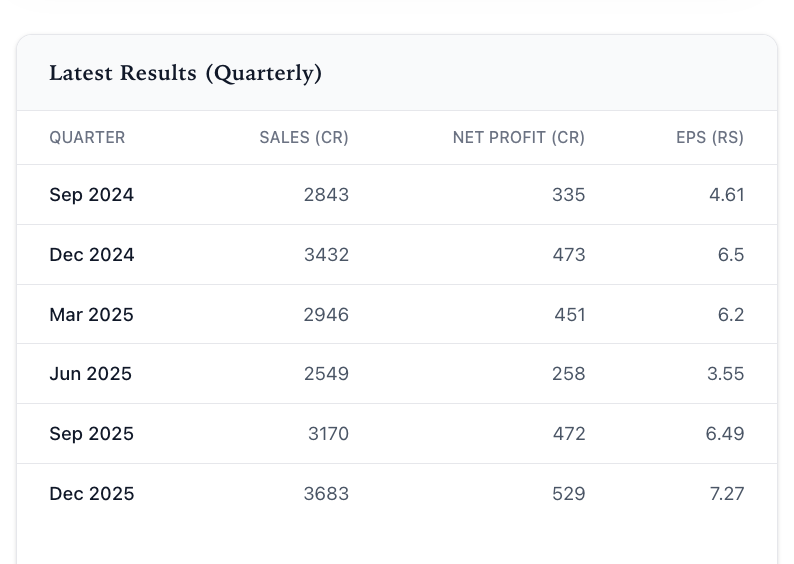

Recent Quarterly Performance (Last 4 Quarters):

The latest quarterly results (Dec 2025, Q3FY26) demonstrate continued strong momentum, with Sales of INR 3,683 Cr and Net Profit of INR 529 Cr, reflecting robust consumer demand and effective festive season execution. The cumulative TTM figures (Q4FY25 to Q3FY26) align perfectly with the TTM data provided in the annual P&L.

4. Growth Drivers & Catalysts

USL is well-positioned to capitalize on several structural and company-specific growth drivers:

Premiumization Trend in India: This is the most significant long-term driver. India’s rising per capita income, increasing urbanization, and expanding middle class are leading to a shift in consumer preferences towards higher-quality, premium alcoholic beverages. Consumers are increasingly willing to pay more for recognized brands, superior taste, and aspirational value. USL’s strategic focus on its ‘Prestige & Above’ portfolio directly benefits from this trend.

Favorable Demographics: India’s large young population, with a significant proportion entering the legal drinking age, ensures a steady inflow of new consumers. Changing lifestyles and social acceptance of moderate alcohol consumption further contribute to market expansion.

Innovation and Portfolio Expansion: USL continuously innovates with new product launches, packaging, and brand extensions to cater to evolving consumer tastes. Leveraging Diageo’s global portfolio, USL introduces and adapts international brands, filling market gaps and attracting new consumer segments. Recent examples include flavored spirits and ready-to-drink (RTD) cocktails.

Distribution Network Expansion & Efficiency: While already extensive, USL continues to optimize its route-to-market strategies, particularly in underpenetrated regions and through digital channels (where legally permissible for information and marketing). Enhanced supply chain efficiencies improve product availability and reduce costs.

Focus on Core High-Margin Brands: The strategic divestment of a significant portion of its ‘popular’ segment brands has allowed USL to dedicate resources, marketing spend, and management attention to its higher-margin ‘Prestige & Above’ portfolio. This focus is expected to continue driving improved profitability and return on capital.

Diageo’s Global Expertise: The strong partnership with Diageo provides a continuous transfer of global best practices in marketing, sales, product development, and operational excellence. This synergy enhances USL’s competitive edge and ensures alignment with global consumer trends and responsible drinking initiatives.

Evolving Regulatory Environment: While historically challenging, there is a gradual trend towards more stable and predictable alcohol policies in some states. Any rationalization of excise duties or distribution reforms could provide further tailwinds for organized players like USL.

5. Risk Assessment

Investing in USL, while promising, is subject to several key risks:

Regulatory & Taxation Risks (High): The spirits industry in India is highly regulated at the state level. Frequent changes in excise policies, taxation structures, distribution norms, and outright prohibition in some states (e.g., Bihar, Gujarat) pose significant risks to sales volume, pricing power, and profitability. Unpredictable policy changes can disrupt operations and impact financial performance.

Competition (Moderate): USL faces intense competition from both international players (e.g., Pernod Ricard, Bacardi) and strong domestic companies (e.g., Radico Khaitan, Allied Blenders & Distillers). While USL holds a dominant position, competitors actively launch new products and expand market share, particularly in the premium segments.

Input Cost Volatility (Moderate): Key raw materials like Extra Neutral Alcohol (ENA), glass bottles, and packaging materials are subject to price fluctuations. ENA prices, in particular, are influenced by molasses and sugar cane availability, which can be impacted by agricultural output and government policies. Sustained high input costs can compress margins.

Economic Slowdown & Discretionary Spending (Moderate): Alcoholic beverages are largely discretionary purchases. A significant slowdown in the Indian economy, leading to reduced consumer spending power, could negatively impact sales volumes and particularly affect the premium segments USL targets.

Social and Health Concerns (Moderate): Increasing awareness about health and wellness, coupled with potential anti-alcohol campaigns or stricter advertising norms, could dampen demand or restrict market access.

Supply Chain Disruptions (Low-Moderate): While USL has a robust supply chain, unforeseen events such as natural calamities, labor strikes, or logistical challenges could temporarily disrupt production and distribution.

Currency Fluctuations (Low): While primarily a domestic player, USL imports some raw materials and premium brands. Adverse currency movements (INR depreciation) could increase import costs, though this is partially hedged or passed on to consumers.

6. Valuation & Price Target

Our valuation for XXXXXXXXXXXXXXXXXX is based on a 12-month forward (Q4FY26-Q3FY27) earnings multiple approach, reflecting the company’s strong brand equity, market leadership, and consistent earnings growth potential driven by premiumization.

Current Market Data (as of May 6, 2026):

Current Market Price (CMP): INR 1,316.00

TTM EPS (Q4FY25-Q3FY26): INR 23.51

Implied TTM P/E: 1316.00 / 23.51 = 55.97x

Valuation Assumptions:

Revenue Growth: We project a sustainable annual revenue growth rate of 9.0% for the next 12-18 months, driven by the strong premiumization trend, expanding distribution, and robust demand.

Net Profit Margin: We anticipate continued margin expansion due to a favorable product mix (higher contribution from Prestige & Above brands), operating leverage, and cost efficiencies. We project the TTM Net Profit Margin to improve to 14.2% for the forward 12-month period (Q4FY26-Q3FY27).

Outstanding Shares: We assume a constant number of outstanding shares at approximately 72.73 Cr (derived from TTM NP of INR 1,710 Cr / TTM EPS of INR 23.51).

Target P/E Multiple: Given USL’s market leadership, strategic focus on premium segments, strong parentage (Diageo), and historical trading multiples for consumer discretionary/staples in India, we assign a target P/E multiple of 58.0x. This reflects a premium over broader market averages, justifiable by the company’s defensive characteristics, brand strength, and consistent growth prospects.

Forward 12-Month Earnings (Q4FY26-Q3FY27) Calculation:

Projected TTM Sales: Current TTM Sales (INR 12,348 Cr) * (1 + 0.09) = INR 13,459.32 Cr

Projected TTM Net Profit: Projected TTM Sales (INR 13,459.32 Cr) * Projected NPM (0.142) = INR 1,911.22 Cr

Projected TTM EPS: Projected TTM Net Profit (INR 1,911.22 Cr) / Outstanding Shares (72.73 Cr) = INR 26.28

Price Target Calculation:

Target Price = Projected TTM EPS * Target P/E Multiple

Target Price = 26.28 * 58.0 = INR 1,524.24

Implied Upside = ((1524.24 - 1316.00) / 1316.00) * 100 = 15.82%

Scenario Analysis:

To assess the sensitivity of our valuation, we consider Bull and Bear case scenarios:

Bull Case (Target Price: INR 1,687.02):

Assumes higher revenue growth of 10.5% driven by stronger premiumization and market share gains.

Net Profit Margin expands further to 14.5% due to enhanced operating leverage and product mix.

A higher target P/E multiple of 62.0x, reflecting exceptional execution and sustained premium valuations in the sector.

Projected TTM Sales = 12348 Cr * 1.105 = 13645.74 Cr

Projected TTM Net Profit = 13645.74 Cr * 0.145 = 1978.63 Cr

Projected TTM EPS = 1978.63 Cr / 72.73 Cr = 27.21 INR

Target Price = 27.21 * 62.0 = INR 1,687.02 (Upside: 28.19%)

Bear Case (Target Price: INR 1,253.50):

Assumes lower revenue growth of 7.0% due to economic slowdown or increased regulatory headwinds.

Net Profit Margin remains stable at the current TTM level of 13.8% (no further expansion).

A lower target P/E multiple of 50.0x, reflecting increased regulatory risks, higher competition, or overall market de-rating.

Projected TTM Sales = 12348 Cr * 1.07 = 13212.36 Cr

Projected TTM Net Profit = 13212.36 Cr * 0.138 = 1823.30 Cr

Projected TTM EPS = 1823.30 Cr / 72.73 Cr = 25.07 INR

Target Price = 25.07 * 50.0 = INR 1,253.50 (Downside: -4.75%)

Our base case upside of 15.82% is above the 15% threshold for a “BUY” recommendation, providing a favorable risk-reward profile.

7. Management Quality & Governance

XXXXXXXXXXXXXXXXXX benefits significantly from its strong association with Diageo plc, which instills a culture of global best practices, robust corporate governance, and ethical leadership.

Experienced Leadership: The management team, comprising seasoned professionals from the global alcoholic beverage industry, brings extensive experience in brand management, sales & marketing, finance, and supply chain operations. The leadership has successfully steered USL through significant restructuring and market shifts.

Diageo’s Influence: Diageo’s majority stake ensures that USL adheres to global standards of corporate governance, transparency, and accountability. This includes stringent internal controls, risk management frameworks, and responsible business practices. The strategic decisions, such as the premiumization drive and divestment of popular brands, reflect a clear, long-term vision aligned with global industry trends.

Focus on ESG: USL is committed to Environmental, Social, and Governance (ESG) principles, mirroring Diageo’s global “Society 2030” strategy. This includes initiatives for water stewardship, responsible sourcing, promoting responsible drinking, diversity & inclusion, and community engagement. This focus enhances long-term sustainability and brand reputation.

Strategic Vision: The management has demonstrated a clear strategic vision, particularly with the successful execution of ‘Project Popular’ – the divestment of non-core popular brands – which has significantly streamlined the portfolio and improved profitability. This proactive approach to portfolio management highlights effective capital allocation and strategic foresight.

Transparency and Disclosure: As a publicly listed company and part of a global conglomerate, USL maintains high standards of financial reporting and disclosure, providing investors with timely and comprehensive information.

Overall, the management quality and governance framework at USL are exemplary, providing confidence in the company’s ability to execute its strategies and deliver long-term shareholder value.

8. Competitive Positioning

XXXXXXXXXXXXXXXXXX enjoys a formidable competitive position in the Indian alcoholic beverages market, characterized by its market leadership, extensive brand portfolio, and strategic advantages derived from its parent company, Diageo.

Market Leadership: USL is the undisputed market leader in the IMFL segment by volume and value, commanding a significant share across various categories. This scale provides cost advantages, superior bargaining power with suppliers and distributors, and extensive market penetration.

Diversified & Premiumized Portfolio: USL boasts an unparalleled portfolio ranging from value-for-money popular brands (those retained post-divestment) to highly premium and super-premium imported and domestic brands. This diversified offering caters to a wide spectrum of consumer preferences and price points, while the strategic focus on the ‘Prestige & Above’ segment allows for higher margins and value growth. Brands like Johnnie Walker, Smirnoff, Black Dog, Royal Challenge, and Signature are household names and command strong consumer loyalty.

Strong Brand Equity: Decades of brand building, coupled with Diageo’s global marketing prowess, have resulted in exceptionally strong brand equity for USL’s key brands. This brand power allows for pricing flexibility and acts as a significant barrier to entry for new competitors.

Extensive Distribution and Reach: USL’s vast and deeply entrenched distribution network across nearly all states and union territories is a critical competitive advantage. Navigating India’s complex, state-controlled alcohol distribution landscape requires significant expertise and relationships, which USL possesses.

Diageo Synergy: Being a Diageo subsidiary provides a unique advantage that no other domestic player can match. This includes access to global innovation, cutting-edge marketing strategies, research & development, and a pipeline of successful international brands. Diageo’s global reputation and financial strength further bolster USL’s position.

Manufacturing Prowess: A robust network of owned and third-party manufacturing facilities across India ensures efficient production, economies of scale, and localized supply chain resilience.

Key Competitors:

Pernod Ricard India: A strong challenger, particularly in the premium segments with brands like Chivas Regal, Absolut Vodka, Ballantine’s, and Jameson.

Radico Khaitan: A leading Indian player with popular brands like 8 PM Whisky and Magic Moments Vodka, and a growing presence in premium segments.

Allied Blenders & Distillers (ABD): Known for Officer’s Choice Whisky, one of the largest-selling whisky brands globally by volume.

Bacardi India: Strong in rum and vodka categories with brands like Bacardi Rum and Grey Goose Vodka.

Globus Spirits: Regional player focused on various IMFL segments.

Despite robust competition, XXX’s unique blend of market leadership, premiumization strategy, strong brand equity, and the strategic backing of Diageo positions it favorably for sustained long-term growth and continued dominance in the Indian spirits market.