India's Largest IT Exporter Posts Record Q4 FY26 Revenue of ₹70,698 Cr — Profit Surges 12%, ₹110/Share Dividend Declared

📊 Executive Summary

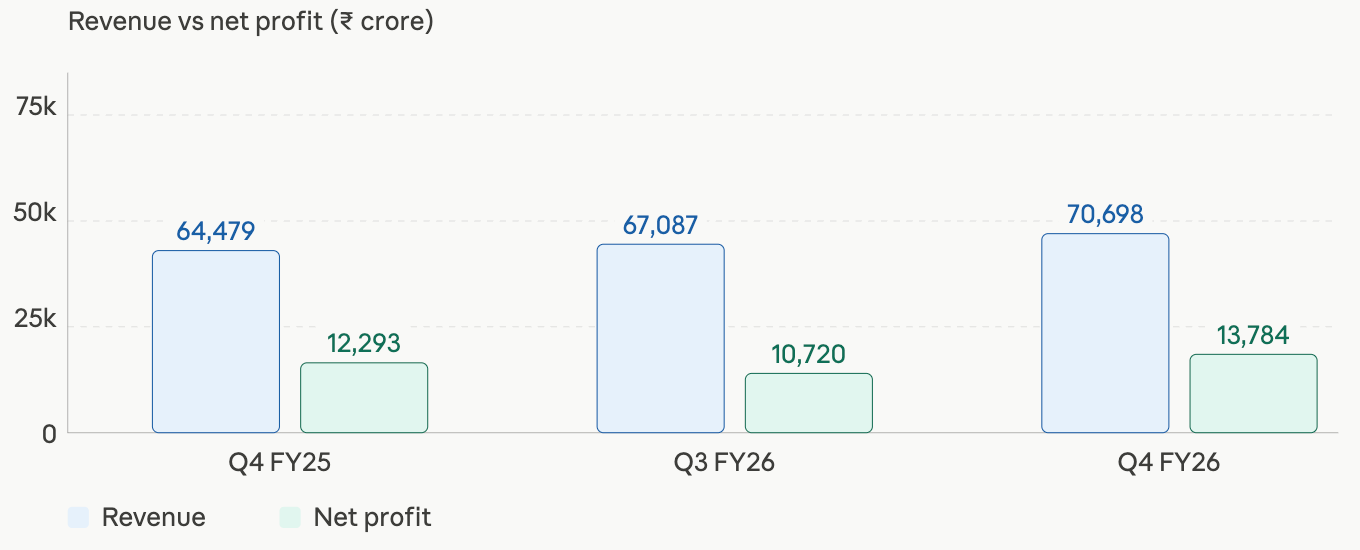

India’s largest IT services exporter closed FY26 on a high note, reporting its strongest-ever quarterly revenue of ₹70,698 crore (+9.64% YoY) and consolidated net profit of ₹13,784 crore (+12.12% YoY) for Q4 FY26. Full-year revenue crossed ₹2,67,021 crore with total dividends declared at ₹110 per share — FY26 dividend yield reflects the company’s consistent capital return philosophy. The quarter’s clean beat, absent of the exceptional charges that weighed on Q3, signals healthy underlying business momentum, even as macro headwinds from DXY strength and client spending caution persist.

📌 Detailed Quarterly Results Breakdown

Consolidated Total Revenue: ₹70,698 crore (↑9.64% YoY; ↑5.38% QoQ) — beat consensus; fifth consecutive sequential uptick

Operating EBITDA (pre-exceptional): Operating income ₹17,605 crore vs ₹15,373 crore in Q4 FY25 — margin expansion driven by lower exceptional charges in Q4 vs Q3’s ₹4,391 crore exceptional hit

Net Profit After Tax: ₹13,784 crore (↑12.12% YoY) — clean quarter; Q3 PAT was depressed by restructuring + labour code + legal provision totalling ₹4,391 crore

Diluted EPS: ₹37.92 (↑28.7% QoQ; vs ₹33.79 Q4 FY25 ↑12.2%) — FY26 full-year diluted EPS ₹136.01 vs ₹134.19 (+1.36% YoY); modest YoY EPS growth reflects exceptional-item drag in H2

📈 Comprehensive Growth Analysis

💰 Operational Cost Structure Analysis

FY25 employee costs: 57.1% of revenue → FY26: 58.0% (+0.9pp) — labour code impact ₹2,128 crore in exceptional itemsFinance costs: ₹1,227 crore (↑54% YoY) — reflects lease liabilities and CSC legal claim interest accrualOther expenses: ₹35,230 crore (↑15.6% YoY) — reflects Coastal Cloud/ListEngage integration costs

🔍 Long-term Financial Health Indicators

5-Year Revenue CAGR (estimated FY21–FY26): ~14% | Net Profit CAGR: ~10% — ahead of Indian IT sector average (~11% revenue CAGR); modest profit CAGR reflects margin normalisation post-Covid peak

ROCE: ~50%+ (estimated) vs industry average ~35–40% — capital-light model with high asset turnover remains a structural advantage

Debt-to-EBITDA: Near zero on gross debt; lease liabilities ₹11,283 crore represent the primary financial obligation; free cash flow from operations ₹52,094 crore (FY26) = strong ~74% FCF/Operating cash conversion

Promoter shareholding: Tata Sons group holds ~72.3% (stable; consistent for multiple quarters) — strong governance signal

🏗️ Strategic Capital Allocation & Future Growth Roadmap

M&A spend FY26: ₹7,362 crore — acquisition of ListEngage ($69M, Oct 2025) and Coastal Cloud ($707M, Jan 2026), both Salesforce ecosystem players; goodwill recognised ₹7,248 crore (₹514 crore + ₹6,161 crore provisionally)

Focus areas: AI-led enterprise transformation via Salesforce (Agentforce, Data Cloud, CRM), expanding Salesforce Summit Partner footprint in North America; new subsidiaries in Saudi Arabia and Morocco signal Gulf + Africa expansion

New subsidiary: HyperVault AI Data Center Limited (incorporated Oct 2025) — signals intent to build proprietary AI infrastructure capacity

Capex (FY26): ₹3,670 crore on PPE; ₹2,665 crore CWIP — moderate physical infrastructure investment consistent with asset-light positioning

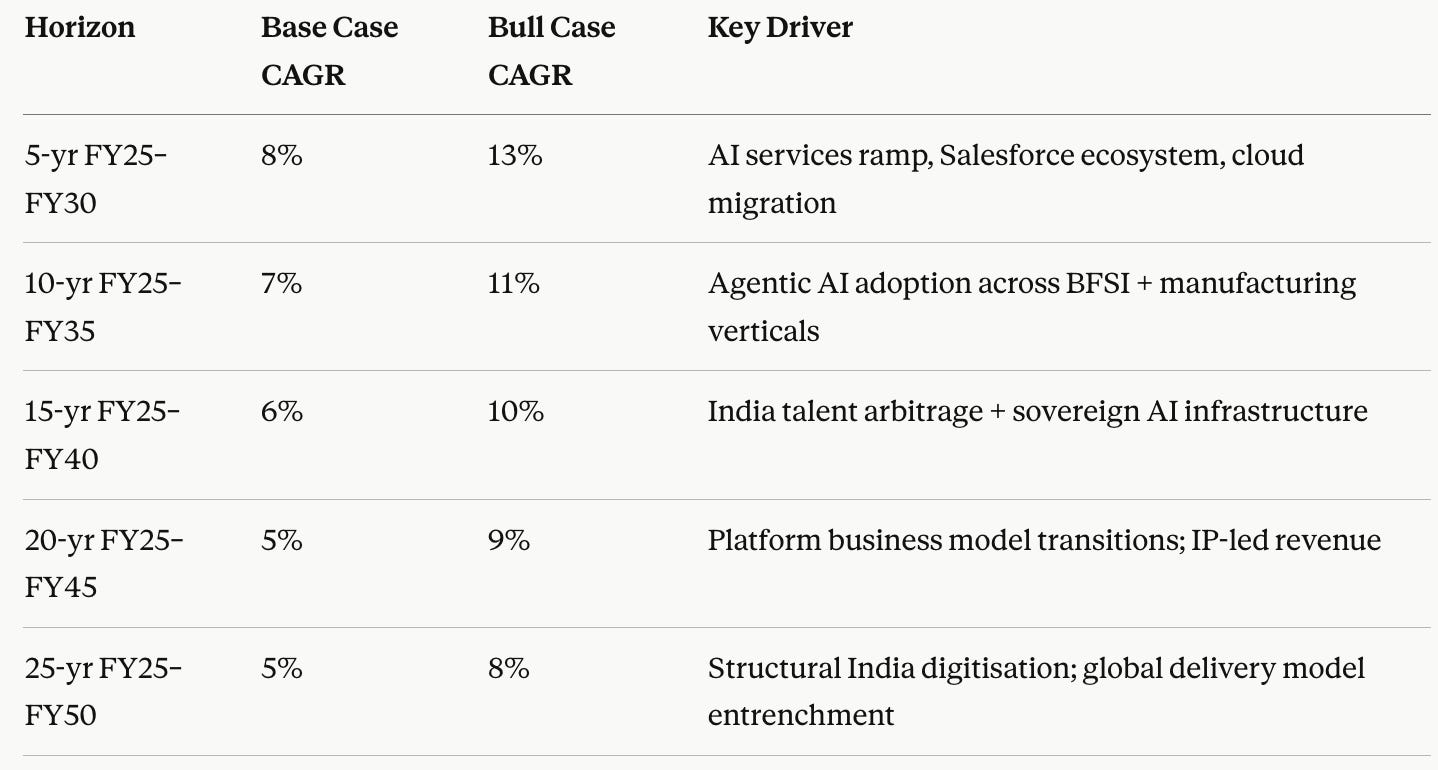

📊 Multi-Decade Growth Trajectory Projections

Base case assumes macro normalisation, no large-scale AI disruption to headcount models. Bull case assumes AI-augmented delivery expanding addressable market faster than headcount displacement.

💸 Current Valuation Analysis & Fair Value Assessment

P/E ratio: At ₹2,588 (Q4 FY26 close per context), trailing P/E ~19x vs 5-year historical average ~27x — trading at a meaningful discount to long-run average

EV/EBITDA: Estimated ~13–14x vs sector average ~18–20x — undervaluation relative to quality peers suggests either mean reversion opportunity or structural re-rating risk

Estimated fair value range: ₹3,100–₹3,600 based on 23–26x forward EPS of ₹136–₹145 — implies 20–39% potential upside from current levels; downside case ₹2,200 if macro deterioration accelerates FII outflows

Dividend yield at current price: ~4.2% on ₹110/share FY26 total dividend — historically attractive entry-level yield for a large-cap IT compounder

Management Commentary & Conference Call Highlights

K. Krithivasan (CEO): “Our deal wins in Q4 reflect customers’ increasing confidence in our ability to deliver AI-led transformations at enterprise scale — Coastal Cloud and ListEngage position us uniquely in the Salesforce ecosystem.”

On restructuring: “The ~1,388 crore restructuring charge reflects deliberate workforce rebalancing — associates whose deployment was not feasible given the shift toward AI-augmented delivery models.”

On Labour Codes: “The ₹2,128 crore statutory impact is a one-time, regulatory-driven item; we do not expect recurrence; employee compensation has been restructured effective April 1, 2026.”

On CSC legal matter: “We filed a petition to the US Supreme Court on March 19, 2026 — we believe we have a strong case; the ₹1,010 crore provision is conservative and prudent.”

Technical Analysis & Chart Patterns

At ₹2,588, the stock has retraced ~29% from its 52-week high of ₹3,630. Key support zone: ₹2,346 (52-week low). Resistance: ₹2,837 (0.382 Fib) and ₹2,988 (0.5 Fib). The Q4 earnings beat + ₹31 final dividend creates a near-term positive catalyst; watch for a gap-hold above ₹2,700 post-results for continuation toward ₹2,837. RSI likely oversold on the weekly timeframe given the extent of correction from highs.

Industry Context & Competitive Positioning

The IT sector faces a bifurcated demand environment: BFSI and Life Sciences spending resilient, while CMT clients deferred spend (CMT revenue -10.1% YoY). The Salesforce ecosystem acquisitions (Coastal Cloud, ListEngage) differentiate this company from pure-play legacy IT peers — Agentforce and Data Cloud are among the fastest-growing Salesforce product lines. Infosys (Q4 results Apr 23) and HCL Tech will set the sector bar; the early Q4 print establishes a high benchmark on both revenue growth and deal momentum (TCV $12B implied from segment performance).

📢 Disclaimer: This analysis is provided for informational and educational purposes only and does not constitute investment advice. The author may hold positions in securities discussed. Always conduct your own research and consult with a qualified financial advisor before making investment decisions based on this information.

If you found this analysis valuable, please consider:

Sharing this newsletter with colleagues interested in Indian equity markets

Subscribing to receive future in-depth analyses

Leaving a comment with your thoughts

#IndiaInvesting #ITServices #NSE #StockMarket #GrowthStocks #QuarterlyResults #FinancialAnalysis #LargeCapIT #TechStocks