India's Infrastructure Play - Hiding in Plain Sight

I) Investment Thesis

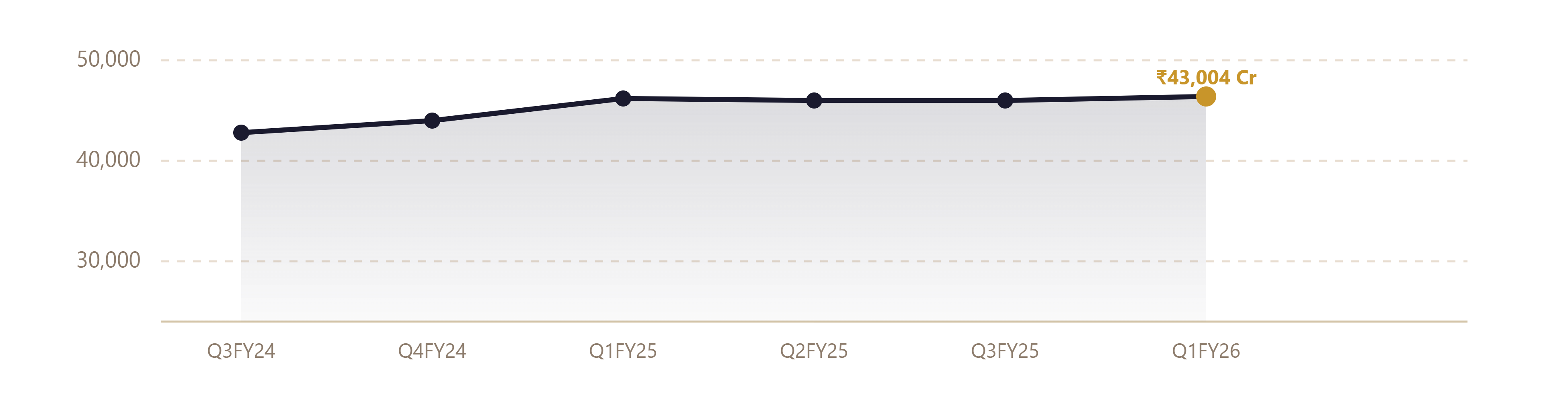

The core thesis is straightforward. India is spending aggressively on infrastructure — metros, power grids, smart factories, high-speed rail. This company sits right at the intersection of all of it. Their order backlog of ₹43,004 crore (that’s roughly 2.5x annual revenues) means they have years of work already locked in. You’re not betting on whether orders will come; they already have.

The demerger of the energy business into a separate listed entity (Siemens Energy India) completed in March 2025. This is actually a positive structural move — it sharpens focus on the core industrial and infrastructure portfolio and eliminates the complexity of running two very different business models under one roof. The remaining entity is cleaner, leaner, and more focused.

“₹43,004 crore sitting in the order book — that’s two-and-a-half years of work already sold. You’re not betting on demand. You’re betting on execution.”

The 75% promoter holding by Siemens AG, Germany is both a comfort and a constraint. It’s a comfort because you have one of the world’s great engineering companies as your anchor shareholder — technology, IP, and global contracts flow through that relationship. It’s a constraint because the float is thin and the stock tends to trade at structurally elevated multiples. That’s the trade-off.

Youtube Link:

II) Business Model & Operations

Four business lines power this machine. Let’s break them down in plain language.

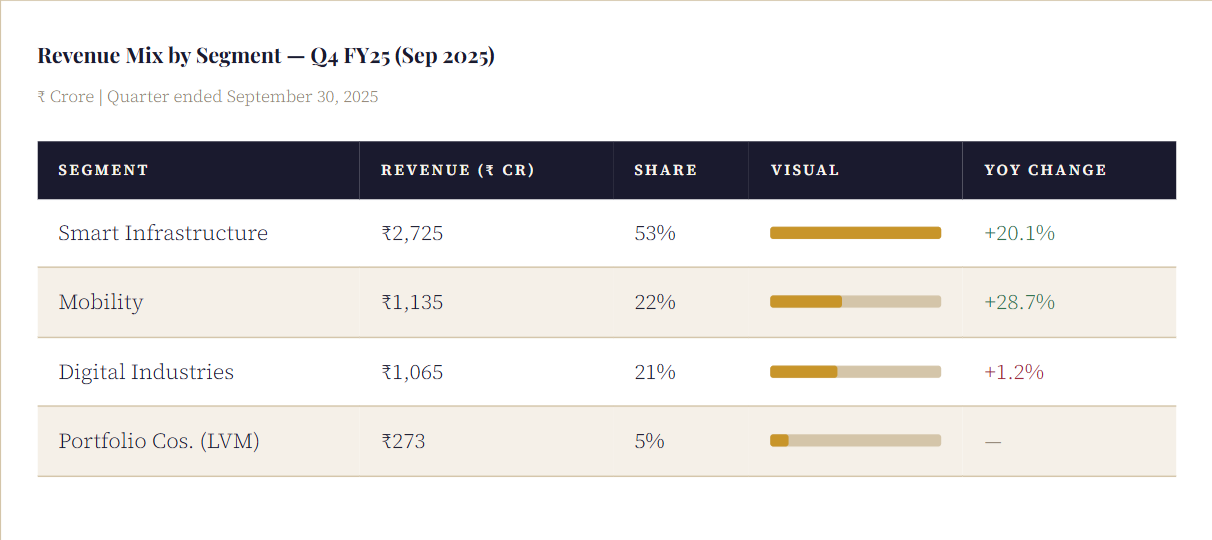

Smart Infrastructure is the biggest piece. Think electrical switchgear, building automation systems, power distribution for factories and data centres, smart grids. This is the most direct play on India’s power and urbanisation story — and it’s the engine of growth right now. Revenue here hit ₹2,725 crore in Q4 FY25 alone, up sharply from ₹2,270 crore a year earlier.

Mobility is the most exciting segment if you believe in India’s metro and railway ambitions. Rail automation, electrification systems, metro signalling — this is where the blockbuster orders live. A consortium involving this company recently secured a landmark high-speed rail automation contract. Mobility revenue nearly doubled QoQ in Q4 FY25 to ₹1,135 crore. The Siemens Rail Automation subsidiary (SRAPL) is also being amalgamated back into the parent — simplifying structure further.

Digital Industries handles factory automation — PLCs, drives, industrial software. This one has been quieter, with ₹1,065 crore in Q4 FY25, roughly flat. The global slowdown in manufacturing capex has muted this segment, but it remains a strategically important business for when India’s manufacturing cycle accelerates.

Portfolio Companies (Low Voltage Motors) is being sold to Innomotics India, with CCI approval received in February 2026. This business contributed roughly ₹273 crore in Q4 FY25 but is no longer core — it lost its technology backbone when Siemens AG sold Innomotics globally. Smart housekeeping, honestly.

One important structural note: the company changed its financial year from the old October–September cycle to the standard April–March. The current period is an 18-month transitional year running October 2024 to March 2026. This means straight year-on-year comparisons are tricky — you need to be careful when reading the numbers.

III) Historical Financial Review

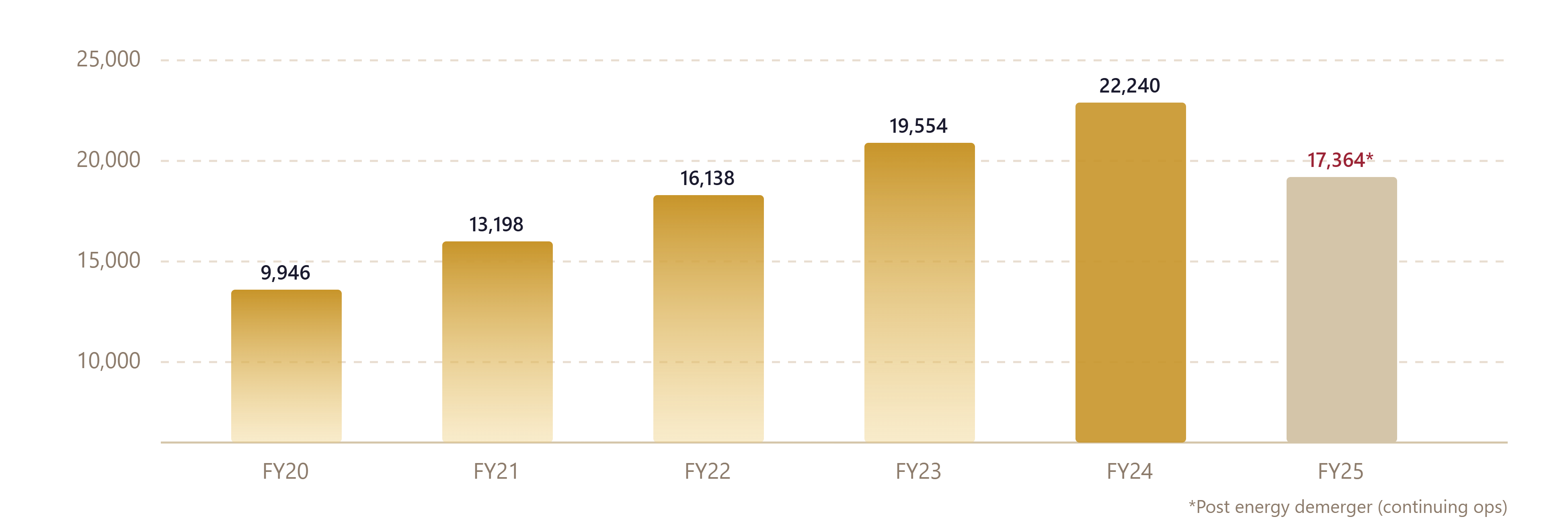

Revenue grew from ₹9,946 crore in FY20 to ₹22,240 crore in FY24 — a strong run driven by India’s capex boom. The FY25 number of ₹17,364 crore looks like a drop, but it isn’t — it reflects the energy business being carved out into Siemens Energy India. Like-for-like, the remaining business kept growing. The 3-year CAGR on the comparable base sits around 10.9%, which is solid but not explosive.

Operating margins have been improving steadily — from around 10–11% in FY20-21 to 14% in FY24. Post-demerger FY25 margins compressed back to around 12%, partly cyclical, partly a reflection of the mix shifting away from high-margin energy contracts. This is worth watching.

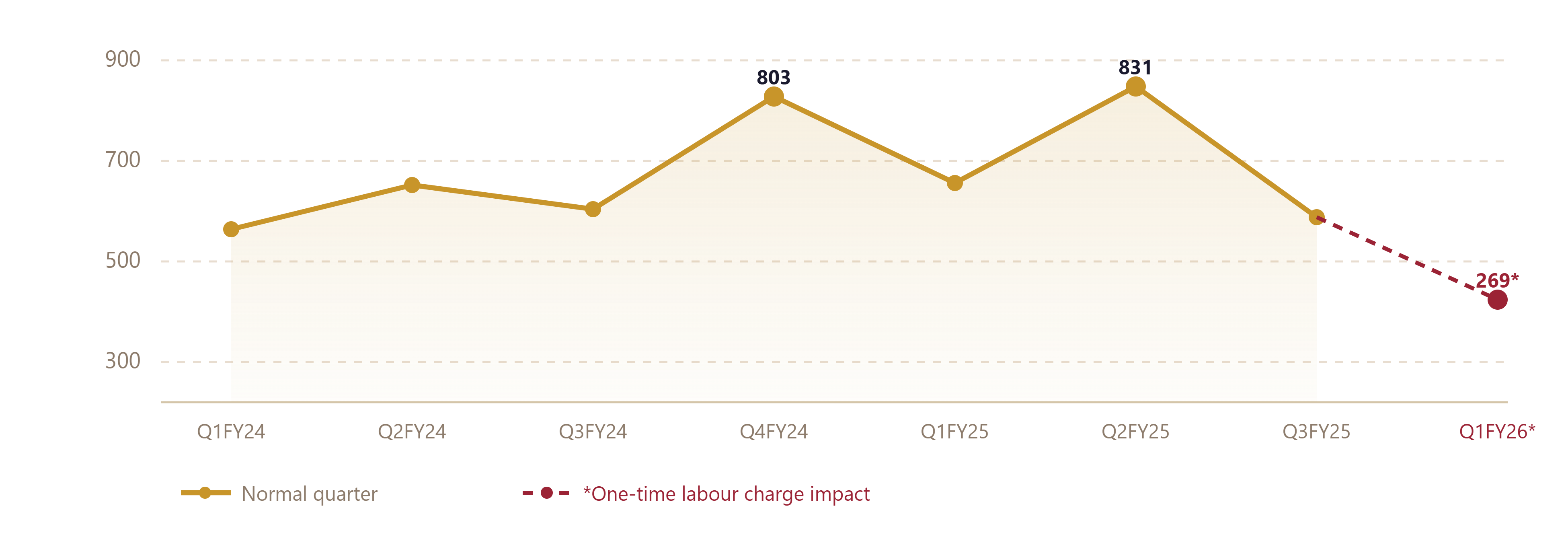

The most recent quarter — October to December 2025 — was a headline grabber for the wrong reasons. Net profit fell 55% year-on-year to ₹279 crore (consolidated). But here’s the critical context: ₹74.3 crore of that drop came from a one-time charge related to the new Labour Codes that kicked in on November 21, 2025. On top of that, there were forex losses from currency volatility. Strip those out, and the operational picture is actually fine — revenue grew 14% to ₹3,831 crore, and new orders rose 19% to ₹4,829 crore.

For 9 months April to December 2025, revenue stands at ₹20,228 crore — a big jump over ₹15,145 crore in the same period last year. The business is executing. The P&L just had a noisy quarter.

IV) Growth Potential & Risks

The macro backdrop for this company is genuinely supportive. India’s Union Budget allocated a record ₹11.2 lakh crore towards capital expenditure. Railways, metros, power transmission, smart cities — all of these require exactly what this company makes. The RBI has pencilled in 7.4% real GDP growth for FY26. Industrial output is expected to grow 6.2%. This isn’t a company fighting a headwind.

Beyond the macro, the Mobility segment is entering a multi-year upcycle. India’s metro network is expanding rapidly across Tier-2 cities. High-speed rail corridors are moving from planning to execution. And the SRAPL amalgamation will make the Mobility segment even more cohesive in its execution capability.

🟢 Bull Case

₹43,004 crore backlog provides multi-year revenue visibility

Government capex sustained at record levels in FY27 budget

Mobility orders accelerate as metro/HSR tenders awarded

Digital Industries recovery as Indian manufacturing investment picks up

Nearly debt-free balance sheet — self-funding growth

75% promoter holding = alignment, tech access, global contracts

🔴 Bear Case

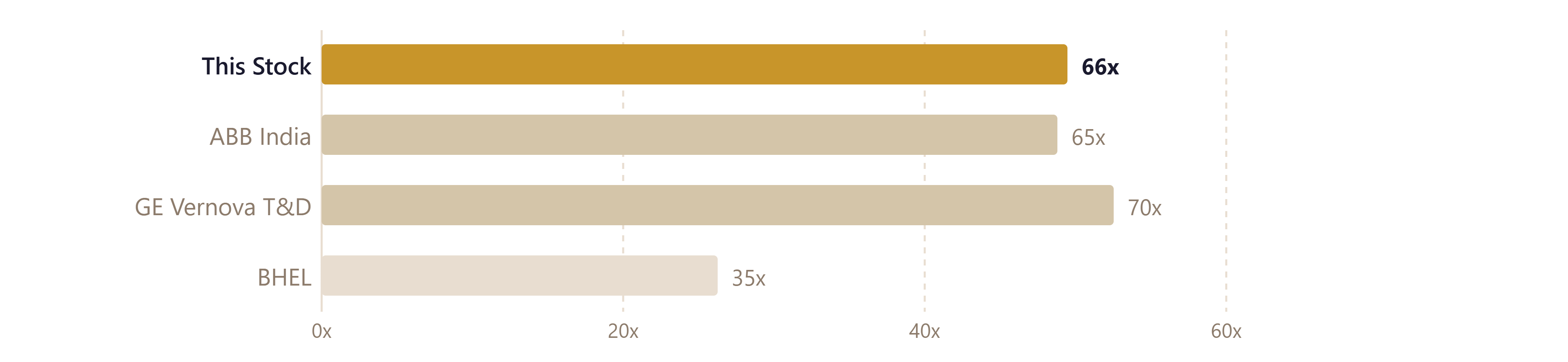

Valuation at 66x P/E leaves no room for disappointment

Government capex slowdown if fiscal deficit targets tighten

Chinese competition risk in infra contracts (recent concern raised by analysts)

Margin compression if project mix skews towards large, lower-margin orders

Transition to new financial year creates comparative confusion

Metro car capex deferred — signals some execution uncertainty

V) Valuation & Target Price

Let’s be straight about this: 66x earnings is expensive. It’s expensive even relative to India’s premium for quality industrial names. The sector trades at elevated multiples because everyone knows the capex story is real — the question is always whether the multiple has run ahead of the earnings.

The 52-week range — ₹2,450 to ₹3,963 — tells you the market has already tried to price in both the optimism and the doubt. At ₹3,215, we’re sitting roughly in the middle of that range. Analyst consensus targets cluster around ₹3,300–₹3,400. A handful of more bullish analysts push to ₹3,700–₹3,950.

My target of ₹3,700 assumes that: (a) the Labour Code hit is truly one-time, (b) the Mobility segment keeps winning large orders, and (c) operating margins recover back towards 13–14% as the business mix normalises. That’s a ~15% upside from current levels — respectable, but not compelling enough to be a screaming buy at today’s price.

For a 5–10 year holding horizon, the story is stronger. If earnings grow at 12–15% annually (which is reasonable given the backlog and India’s capex pipeline), you could be looking at ₹7,000–₹9,000 per share a decade out, assuming multiples compress modestly from current levels. This is a compounder, not a momentum trade.

VI) What to Watch Next

The transition to the new April–March financial year completes in March 2026. From FY27 onwards, results will be on a standard calendar that makes comparisons clean again. The first full April–March result will be worth scrutinising closely for normalised margins.

Watch the Digital Industries segment carefully. It’s been flat for several quarters. Any uptick there — driven by India’s semiconductor push, PLI-backed manufacturing expansion, or the Simatic/Sinamics product cycle — could be a meaningful earnings catalyst that the market isn’t currently pricing in.

The LVM (Low Voltage Motors) sale to Innomotics India, pending regulatory clearance, will simplify the portfolio further. Small near-term positive, but strategically it signals management’s commitment to keeping the business clean and focused.

Finally, keep an eye on the Chinese competition narrative. If the government eases bidding restrictions for Chinese companies in infrastructure contracts, ABB, Siemens, and L&T all face margin pressure in power equipment tenders. That’s a risk worth monitoring — not panicking about, but monitoring.

The Bottom Line

This is a genuinely excellent business with a stellar order book, strong promoter backing, a debt-free balance sheet, and direct exposure to India’s most exciting long-term theme: infrastructure and industrialisation. The Q1 FY26 profit dip is noise, not signal.

The problem is the valuation. At 66x trailing earnings, everything has to go right. There’s limited margin for error. For long-term holders — hold, and add opportunistically on dips below ₹2,800. For new investors — wait. A better entry will come.

This is a 10-year story. The 10-year story is good. The next 12-month story is: expensive, but backed by ₹43,000 crore of locked-in work.